ACH payment processing made easy.

Helcim merchants are able to accept ACH (automated clearing house) payments without the need for any extra signups or complicated paperwork. Online ACH payments are built directly into your free Helcim account.

For Canadian merchants, see EFT/PAD payments0.5 + 25

$5 per returned or rejected transfer

Ways small businesses can accept ACH.

-

Get invoices paid by ACH transfers

Easily create and send professional invoices online, and give your customers the ability to pay those invoices via ACH. No need for complicated setup, customers can simply enter their bank account information and pay.

-

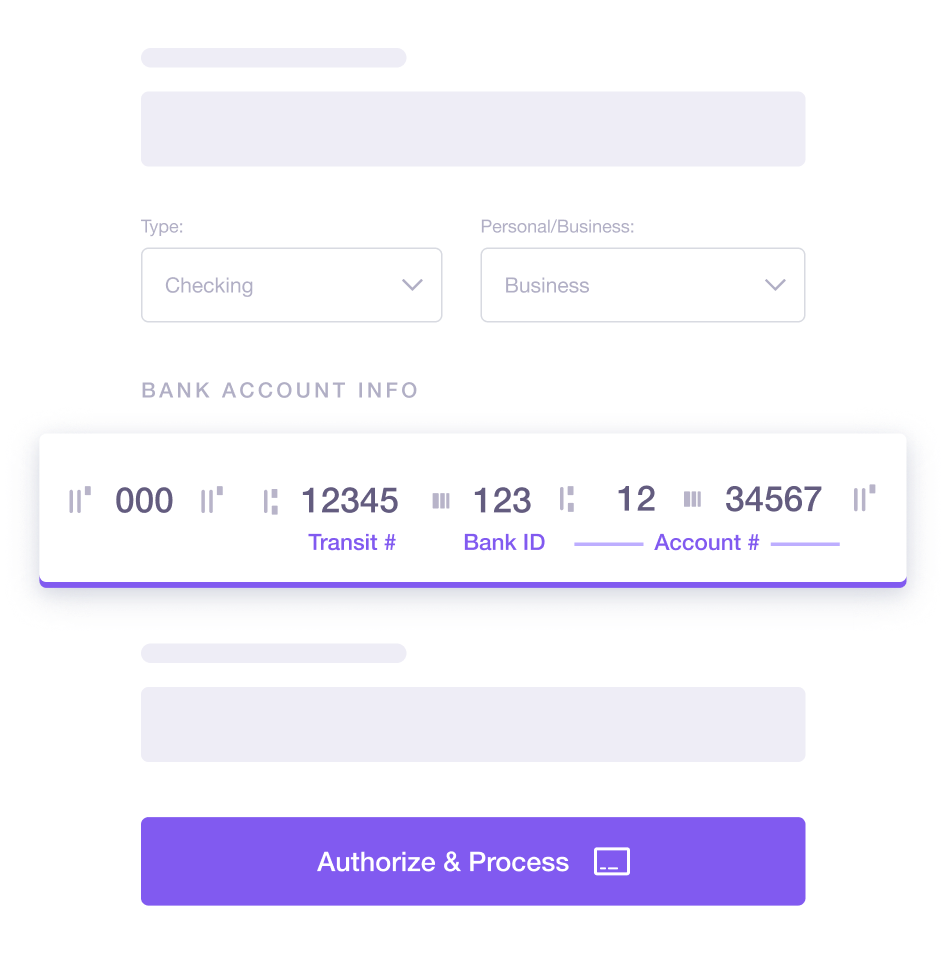

Process ACH payments with the Virtual Terminal

Accept ACH payments on your computer by simply entering your customer's bank information. Bank account details are automatically encrypted and stored as part of your customer card vault.

-

Automate recurring payments with ACH transactions

Helcim gives you all the tools you need to automate your client billing and set up customized recurring payment plans via ACH. Payments are collected automatically on each set date, with customers notified in advance.

-

Request ACH payments by email & SMS

No more buried unpaid invoices. Follow up on client ACH payments with email or SMS requests. Reach your client where they are the most - on their phone and gently remind them to send a quick payment.