Nice work! you set up your tax account with your bank details and got your refund deposited weeks faster than waiting for a check. It was so convenient that now you’re wondering: Could I set up something similar to process electronic payments for my business? Maybe it’s even better than taking credit card payments.

When it comes to getting paid, you’ve got options. ACH payments and credit card transactions each come with their own pros and cons, so it’s worth comparing them closely to see what fits your business best.

Below you’ll find a quick side-by-side comparison between ACH versus credit card payments. If you want more details on how they stack up, just keep reading.

| Key aspect | ACH payments | Credit card payments |

|---|---|---|

| Processing flow | Bank-to-bank transfers through the ACH network. | Routed via card networks plus issuing and acquiring banks. |

| Revenue impact | Best for predictable, recurring payments. | Can lift average order value due to rewards and available credit. |

| Processing fees | ~0.5%–1% per transaction. | ~2.5%–3% + fixed per-transaction fee. |

| Processing time | Slower: funds in 3–5 business days. | Faster: funds in 1–3 business days. |

| Customer experience | Ideal for automatic, recurring billing. | Great for one-time and impulse purchases. |

| International processing | U.S. only. | Designed for global transactions. |

| Compliance requirements | Governed by NACHA; requires signed authorization. | Must comply with PCI DSS security standards. |

| Security considerations | Higher risk if bank details are exposed; harder to verify account ownership. | Robust fraud tools available (AVS, CVV, 3-D Secure, risk scoring). |

How are ACH and credit card payments processed differently?

When you accept an ACH (automated clearing house) payment, you first need your customer to sign a NACHA authorization form. This form gives you the go-ahead to directly transfer funds from their bank account into yours, using the Automated Clearing House (ACH) network. It's a secure, bank-to-bank method that moves funds electronically without involving debt.

Credit card payments take a totally different route. When your customer pays with their credit cards, their transaction details immediately travel through card networks like Visa or Mastercard, as well as issuing and acquiring banks. The customer’s bank quickly checks if there’s enough available credit or if the transaction exceeds their spending limit. If everything checks out, the transaction is approved, and the funds move into your merchant account. (Learn more about how credit card processing works here)

ACH vs. credit card: which is easier for customers to spend more?

Credit card payments make it convenient for customers to buy more because they can borrow funds instantly from their banks. Plus, credit cards come with appealing incentives like reward points or cash-back offers. For businesses looking to increase their average transaction value, like retail or wholesale stores, accepting credit cards can encourage larger purchases.

On the other hand, ACH payment method offers convenience for customers who prefer predictable, recurring payments. ACH works best for businesses that rely on steady monthly revenue streams, such as subscriptions, payment plans, or installment-based services. SaaS companies, gyms, or membership-based businesses often choose ACH payments because customers appreciate the ease of automatic billing without needing to manually authorize each payment.

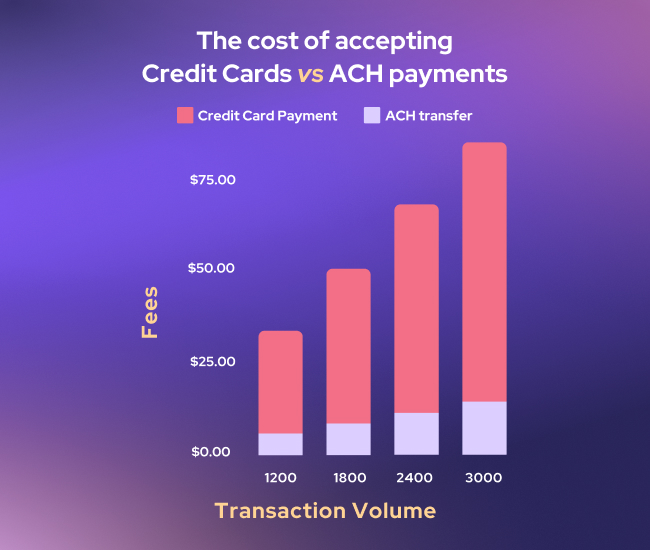

Is it cheaper to accept payments by credit card or ACH transfer?

Credit card processing fees typically range from 2.5% to 3% of the transaction amount (learn more about lowest credit card processing fees). In contrast, ACH transfer has lower processing fees, usually around 0.5% to 1% per transaction. Because of these lower rates, ACH transfers are popular for recurring billing and large-value transactions. The more you process, the quicker the savings from using ACH start to add up.

But processing fees aren’t just the only fees. There are also extra costs tied to credit card chargebacks and ACH returns. If a customer files a credit card chargeback, whether it’s valid or not, you’re hit with a fee that can range from $15 to over $35. Similarly, if your customer’s bank rejects an ACH payment you tried to pull, you’ll often pay a return fee between $10 and $15.

While many payment processors keep these fees no matter what, Helcim takes a different approach. If you successfully dispute a credit card chargeback or prove an ACH transaction was valid, Helcim refunds those chargeback and return fees, helping you keep more of your hard-earned money.

How long does it take to receive payment via ACH vs. credit card?

Credit card payments are typically processed within 1 to 3 business days. In contrast, ACH payments can take 3 to 5 business days to reach your account. Because credit cards move faster, they’re the most common choice for both in-person and online purchases.

ACH payments take longer because transactions aren't processed right away. Instead, they’re grouped into batches and sent through the ACH network several times each business day. The network then sorts and verifies these transactions overnight to ensure everything is legitimate. These extra steps usually add 1 to 2 days to the process.

Because credit card processing is faster than ACH payments, you can use it to collect payments and have funds to pay suppliers, cover payroll, or reinvest in your operations sooner.

How do ACH and credit card payments affect the customer experience?

When customers pay with ACH, they must provide their bank account details, routing and account numbers, and authorize transactions using a NACHA-compliant form. While it’s simple once set up, this initial step can feel cumbersome to some customers. However, ACH payments become highly convenient when customers prefer automatic payments rather than manually entering payment details every time.

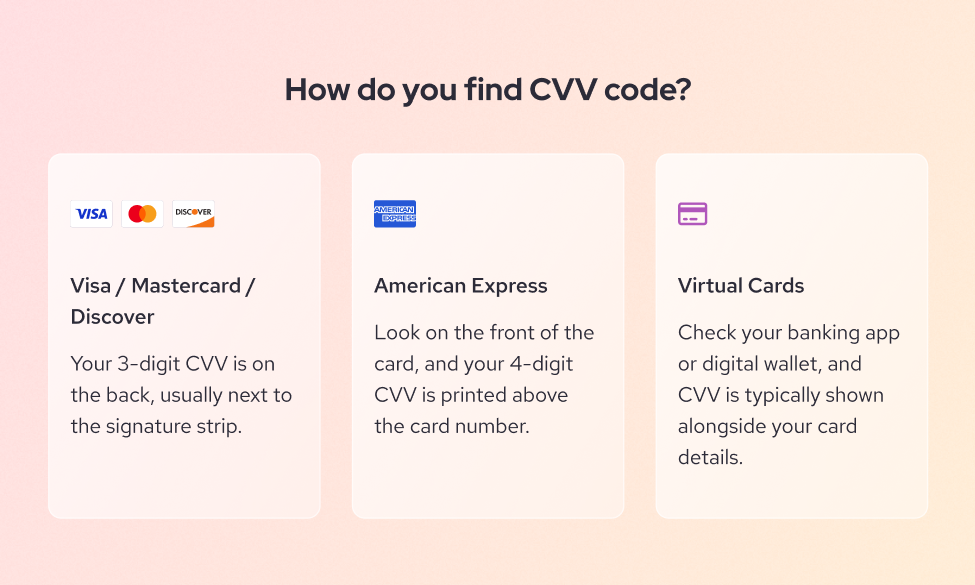

Credit card payments are quick. For in-person transactions, they simply tap or insert their cards and pay. For online transactions, they just need to enter their credit card number, expiry date, and CVV which can be easily found on the card itself. In contrast, ACH payments require customers to provide bank account, branch number and routing numbers, which can be confusing and tedious to find.

In short, ACH payments work best when your customers regularly pay large or recurring invoices, where speed matters less than lower costs. Credit cards provide a seamless, fast experience that’s perfect for retail, ecommerce, and impulse buys, where convenience drives the customer’s purchasing decisions.

ACH vs. credit card: which is better for international transactions?

When it comes to international payments, credit cards are the clear winner over ACH transfers. ACH is designed only for domestic payments within the U.S. Credit cards, on the other hand, run on global networks like Visa and Mastercard, making it easy to accept payments from customers anywhere in the world (learn more about international credit card processing).

The credit card networks handle currency exchange behind the scenes, so you can charge in your own currency while your customer pays in theirs. Of course, you may pay higher processing fees and your customers may pay an extra currency conversion charge.

How do compliance requirements differ for ACH vs. credit card payments?

ACH compliance rules are set by NACHA, the organization that manages the ACH network. Before you can pull funds from a customer’s bank account, they need to sign a NACHA-compliant authorization form to give you permission. You also need to store and organize all these authorization forms to prove your legitimacy if an ACH return ever happens.

Credit card payment processing follows PCI DSS (Payment Card Industry Data Security Standard) rules. PCI compliance is all about protecting sensitive card data. The payment processors you use must comply with PCI, but you’re still required to complete annual self-assessments or questionnaires to show you’re following PCI requirements too.

What are the security risks when processing credit card and ACH transactions?

When accepting ACH payments, your biggest security risk is ACH phishing and ACH kiting:

- Fraudsters often use phishing techniques to steal a victim’s bank account and routing numbers. They then use those details to make unauthorized purchases from your business. Once the real account holder sees the unauthorized transaction, they’ll contact their bank to reverse the payment.

- Another ACH risk is ACH kiting, where criminals exploit the delay in ACH processing. They shuffle money between accounts to artificially inflate their balances. Then, using this falsely inflated account, they purchase goods or services from you. Once the bank identifies the scheme and corrects the balances, your received payment is reversed because there isn't sufficient funds in the first place.

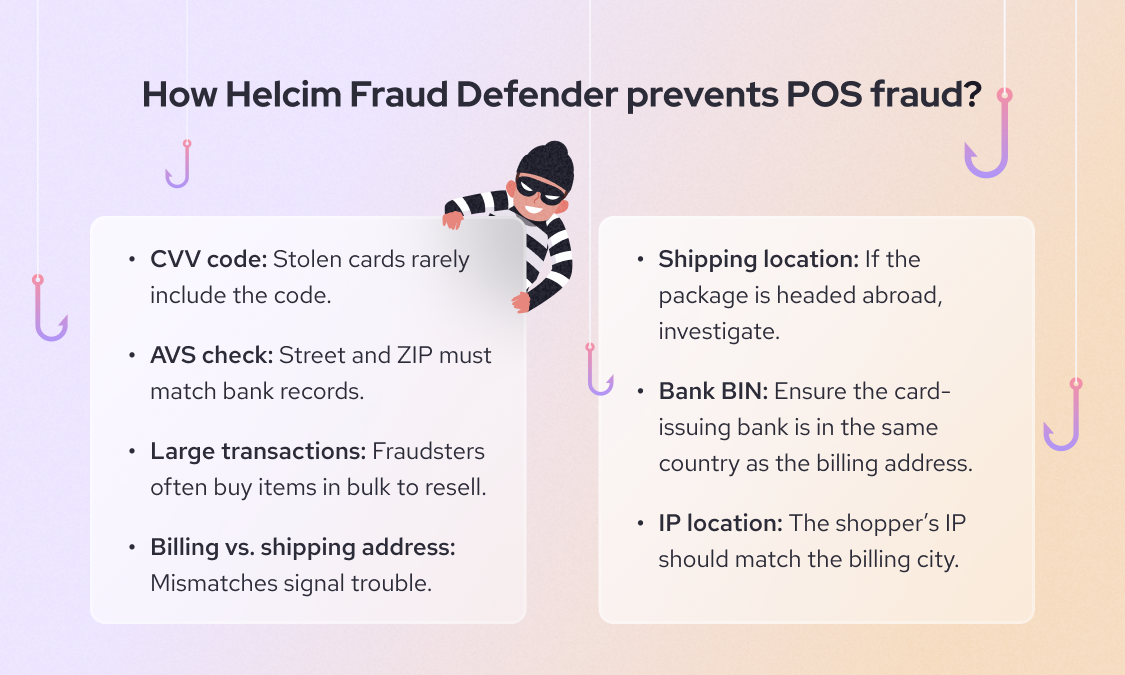

With credit card payments, your security risk comes from stolen credit card information. Fraudsters often use credit card skimmers or phishing emails to steal credit card information. They then use these stolen cards to buy from you. When the actual cardholder sees an unauthorized charge, they contact their bank and initiate a credit card chargeback. Learn how to avoid processing stolen credit card information.

All the security risks above leave you with the loss of your products and services when the payments are reversed. Processors like Helcim provide tools to help your business prevent payment fraud risks.

How to accept credit card and ACH payments at low fees

If you’re looking to accept ACH and credit card payments at low fees, Helcim is an ideal option:

- Credit card fees: Helcim offers a transparent interchange-plus pricing that lets you save 25% on processing fees compared to other credit card processors. Visit Helcim pricing page for more detail.

- ACH transfer fees: Helcim offers 0.5% + 25¢ per transaction, capped at $6 for transactions below $25,000.

Not only that, you can have access to all payment tools with no monthly fees, contract, hidden fees or set up fees.

- Helcim Virtual Terminal: Process EFT and ACH payments online without any hardware, from your laptop, tablet or mobile.

- Helcim Invoicing: Send online invoices, handle late payments and automate follow-ups.

- Helcim Recurring Payments: Automate billing, customize subscription plans, and grow revenue effortlessly.

- Helcim Payment Pages: Securely add payment functionality to your website, with no programming required.

FAQ

What are the potential chargeback scenarios for ACH and credit card transactions?

Credit card chargebacks occur when customers dispute charges due to unauthorized transactions, dissatisfaction with products, fraud, or billing errors. For ACH payments, ACH returns happen if a customer disputes or didn’t authorize a transaction, has insufficient funds, or provides incorrect banking details.

Which payment method, ACH or credit card, offers better fraud protection?

ACH payments generally offer less fraud protection for merchants. That’s because customers provide their banking details directly, and it’s hard to know if they’re truly the account owners or if they got that information through phishing. In contrast, credit card payments come with more advanced fraud tools. Payment processors like Helcim can flag risky transactions by analyzing factors such as shipping address, IP location, and purchase history, giving you stronger protection against fraudulent activity.

Are there any hidden fees associated with ACH and credit card processing?

Yes, credit cards often include additional fees for chargebacks, PCI compliance, monthly statements, or international currency conversion charges. ACH may include fees for ACH returns, reversals, or failed transactions.

How do ACH and credit card payments impact a business's cash flow?

Credit card payments are processed from 1-3 business days, helping you quickly access your funds. ACH payments typically take 3-5 business days, which is slower and can impact your business’s cash flow. However, ACH’s lower transaction fees can improve profitability over the long term.

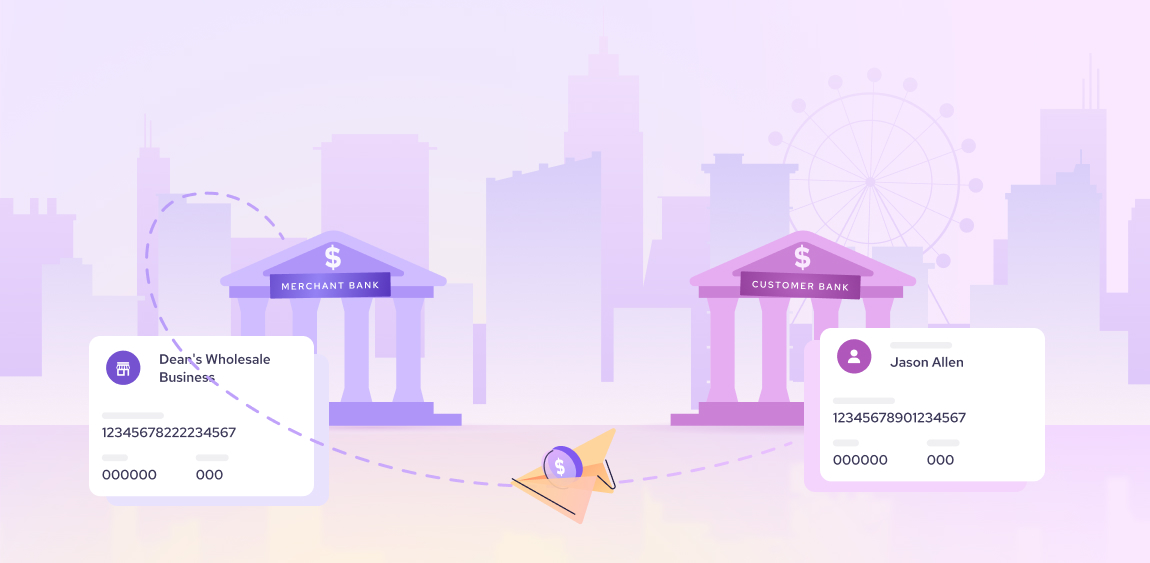

What is the role of banks in ACH and credit card transactions?

In ACH transactions, banks serve as ODFI (originating depository financial institution) and RDFI (receiving depository financial institution), securely transferring funds between customer and merchant accounts via the ACH network. For credit card transactions, banks act as issuers (providing credit to cardholders) and acquirers (processing payments for merchants). Issuing banks verify cardholder details and authorize transactions, while acquiring banks facilitate payment settlement into merchant accounts.