-

Content

Disconnected payment systems create manual work, reconciliation delays, and reporting errors. Online payment integration connects your business software directly to a payment gateway or payment processor, allowing transactions to sync automatically with accounting, invoicing, CRM, and inventory systems.

Instead of manually entering totals, payments flow securely between systems in real time — reducing administrative work and improving financial accuracy. According to the Federal Reserve Payments Study, electronic payments continue to grow year over year, reflecting sustained business and consumer demand for digital payment options.

This guide answers the most important questions businesses ask about online payment integration.

What is online payment integration?

Online payment integration is the process of connecting your website, POS system, CRM, or accounting software directly to a payment gateway or payment processor.

Rather than manually recording payments, your system securely transmits payment information and receives a confirmation response. Once approved, the transaction can automatically:

- Mark invoices as paid

- Update accounting records

- Adjust inventory levels

- Store customer payment data (tokenized)

- Trigger receipts and notifications

This automation reduces double entry and improves operational efficiency.

How does online payment integration work?

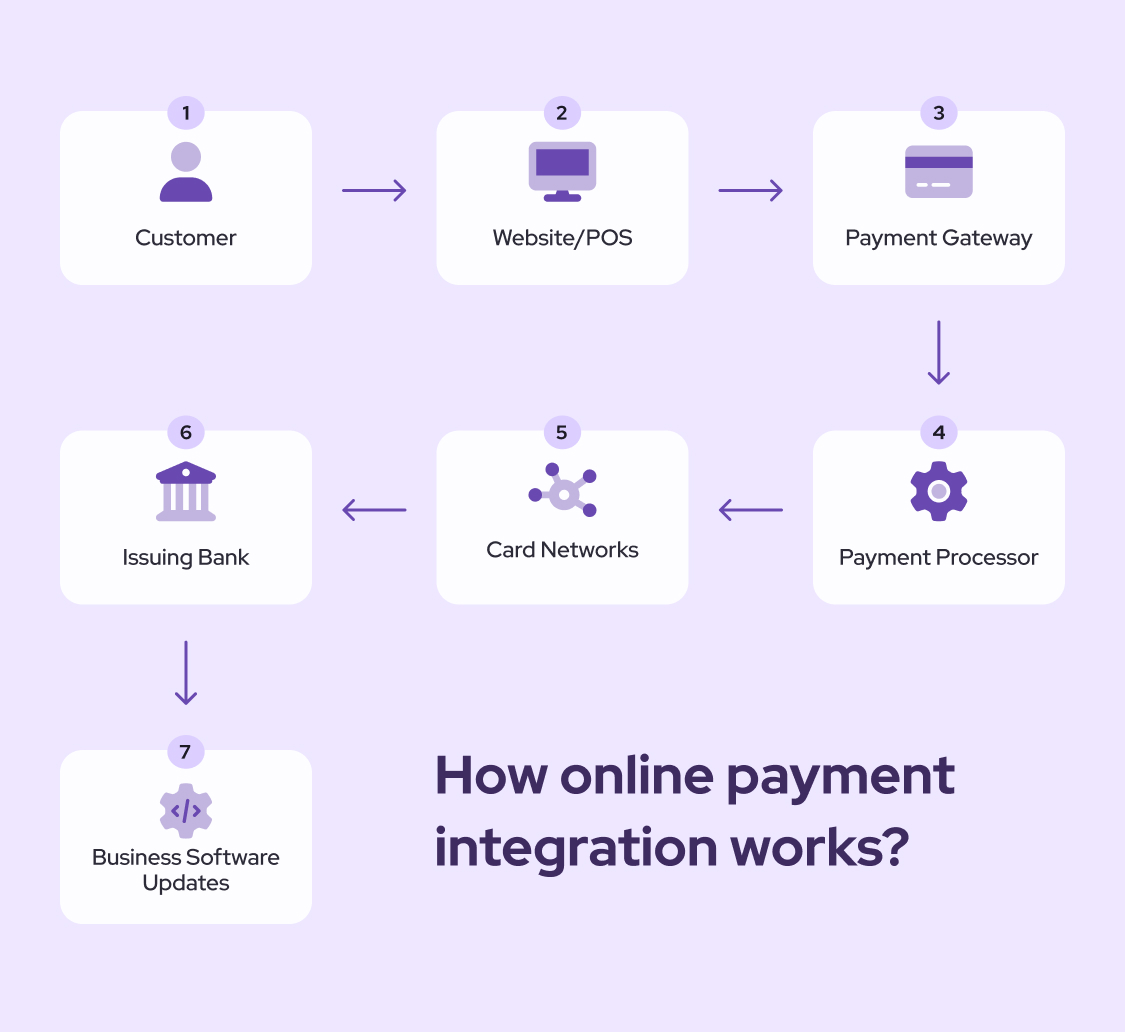

Online payment integration works by securely transmitting payment data between your software and your payment processor using APIs, SDKs, or secure connectors.

The typical process includes:

- A customer initiates a payment.

- Your system encrypts and sends payment data to the processor.

- The processor routes the transaction through card networks for authorization.

- The issuing bank approves or declines the transaction.

- A confirmation response is returned to your system.

- Your software updates records automatically.

Most integrations rely on encryption and tokenization to protect sensitive payment data. Tokenization reduces the risk of storing raw card data and aligns with the security standards outlined by the PCI Security Standards Council (PCI SSC).

What are the different types of online payment integration?

There are three primary types of online payment integration, each suited to different business needs. Those three types are API payment integrations, SDK-based payment integrations, and browser-based payment integrations.

What is API payment integration?

API payment integration connects your software directly to a payment processor using secure API calls.

- Best for: Custom checkout experiences and scalable platforms

- Benefit: Full control over payment flows, branding, and automation

- Consideration: Requires developer resources

API integrations are ideal for SaaS platforms, marketplaces, and growing businesses that want flexible payment workflows.

What is SDK-based payment integration?

SDK integration uses pre-built software libraries to embed payment functionality into mobile apps or proprietary platforms.

- Best for: Mobile apps and SaaS platforms

- Benefit: Faster development with secure, pre-coded components

- Consideration: Less customization than a full API build

SDKs can reduce development time and often include secure handling of card data in a way that supports compliance with the PCI DSS standards.

What is browser-based payment integration?

Browser-based integration uses a connector or extension to transmit payment data from web-based software to payment hardware or gateways.

Browser-based integration is best for small businesses without developer resources because it doesn't requires coding to set up. However, the downside of browser-based payment integration is the low customization flexibility.

This approach is often a good fit for businesses that want payments connected to their workflow but don’t have an engineering team.

Which industries benefit most from online payment integration?

Online payment integration is valuable for nearly any business that accepts digital payments, but some industries see especially strong benefits because they deal with high transaction volume, invoicing workflows, or recurring billing.

Common industries that benefit include:

- Ecommerce and retail: Online retailersoften integrate payments to support faster checkout, reduce cart abandonment, and sync transactions automatically into inventory and fulfillment systems. Explore payment processing for retailers more.

- SaaS and subscription businesses: Subscription-based businesses rely on integrated payments for automated recurring billing, failed payment recovery workflows, and customer lifecycle tracking.

- Professional services and consultants: Service-based businesses benefit from integrations that automatically update invoices, track receivables, and reduce the time spent chasing payments. Explore payment processing for service-based businesses more.

- Healthcare and wellness clinic:s Clinics often need integrated payments to support recurring payments, appointment-based billing, and secure storage of customer payment methods. Explore payment processing for healthcare businesses more.

- Home services and contractors: Contractors and field service businesses can benefit from mobile payment acceptance and automated invoice syncing, reducing delays between job completion and payment. Explore payment processing for contractors and home service businesses more.

- Nonprofits and membership organizations: Nonprofits often rely on integrated payments for donations, recurring contributions, and donor reporting. Explore payment processing for non-profit businesses more.

How much does online payment integration cost?

The cost of online payment integration typically includes: payment processing fees, monthly platform or gateway fees, and optional costs like chargeback fees, add-on features, and development work. Most businesses pay around 2.5% to 3.5% per card transaction, while monthly fees (if applicable) can range from $0 to $50+ per month, depending on the provider and tools included.

| Cost type | Typical range | What it covers |

|---|---|---|

| Card processing fees |

|

|

| Monthly gateway/platform fees |

|

|

| Chargeback fees |

|

|

| Add-on feature fees |

|

|

| Development costs (API/SDK) |

|

|

Payment processing fees for online payment integration

Everytime your customer pays by credit or debit card through the online payment integration, you are charged payment processing fees. Most providers charge a percentage of the transaction amount plus a flat per-transaction fee.

For most businesses, card processing fees typically range from 2.5% to 3.5%, plus an additional $0.10 to $0.30 per transaction, depending on the provider, card type, and how the payment is accepted.

These fees include interchange costs set by card networks, as well as processor markup. Some processors charge higher rates because they bundle additional services such as fraud tools, payout speed, chargeback management, and software features into the pricing.

How Helcim helps: Helcim offers transparent interchange-plus pricing and volume-based rate reductions, which can help businesses lower their effective processing costs as they grow. Explore Helcim payment processing fees here.

Subscription fees or gateway costs for online payment integration

Some payment providers charge monthly subscription or gateway fees in addition to transaction fees. These charges typically cover access to payment tools, reporting dashboards, or gateway services.

Common monthly costs include:

- Gateway or platform access fees: typically $0 to $50+ per month

- Premium reporting or analytics: typically $10 to $100+ per month

- API access or advanced tools: sometimes included, sometimes charged separately

Processors that advertise lower transaction rates may offset that pricing with higher monthly fees, which can increase total cost depending on your transaction volume.

How Helcim helps: Helcim provides not only a free merchant account with no monthly fees, but also a low and transparent payment processing fees. With Helcim, your business can avoid paying for basic access and reporting. Sign up for a free Helcim merchant account here.

Add-on fees for online payment integration

Beyond standard processing fees, some providers charge additional fees for specific payment features. These add-ons may be optional, but many become necessary as businesses scale.

Common add-on fees include:

- Recurring billing tools: typically $10 to $50+ per month

- Multi-currency support: often 1% to 3% extra per transaction

- Advanced fraud tools: typically $5 to $100+ per month

- International transaction fees: often 0.5% to 2% extra per transaction

Some processors charge these fees because they rely on third-party services or increased risk management costs, especially for cross-border payments or high-risk transactions.

How Helcim helps: Helcim supports key payment tools without forcing businesses into expensive software bundles, helping reduce unnecessary add-on costs.

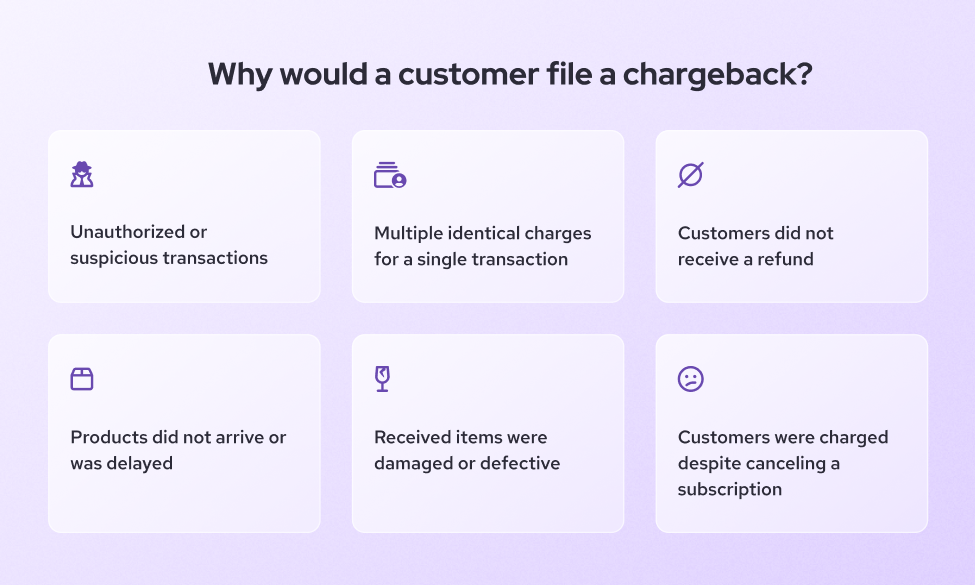

Chargeback fees for online payment integration

A chargeback occurs when a customer disputes a transaction through their card issuer. If this happens, payment processors typically charge a fixed dispute fee, regardless of whether you win or lose the case.

Chargeback fees often range from $15 to $30 per dispute, depending on the processor.

While the chargeback fee is the direct cost, the true cost is often higher. Many businesses lose the product or service, spend time responding to the dispute, and may also face increased processing risk if chargeback rates rise.

How Helcim helps: Helcim provides tools and reporting that help businesses track disputes and manage transaction records more efficiently, reducing the time and cost of responding to chargebacks.

Developer costs for online payment integration

Developer costs apply mainly to businesses that build custom API or SDK payment integrations. Costs vary depending on complexity, testing requirements, and internal resources.

Typical development cost ranges include:

- Simple integration setup: $1,000 to $5,000

- Custom checkout and workflows: $5,000 to $25,000+

- Enterprise-level integration projects: $25,000 to $100,000+

In addition to initial setup, businesses should plan for ongoing maintenance costs, especially when APIs change or new payment features are added.

For businesses that want to avoid development work, native integrations or browser-based tools can significantly reduce time and cost.

How Helcim helps: Helcim offers multiple integration options, including developer APIs and browser-based tools like the Helcim Payment Extension, allowing businesses to choose the approach that fits their technical resources and budget.

What are the requirements for online payment integration?

To implement online payment integration successfully, businesses typically need a few key components, including a merchant account, developer resources, compatible software, reliable internet connection and a browser. Depending on the type of integration you choose, you may also need developer support for setup and testing.

1. Merchant account

Yes. Most online payment integrations require a merchant account to accept credit and debit card payments.

A merchant account temporarily holds funds before they’re settled into your business bank account.

If you don’t already have a merchant account, Helcim offers a free merchant account that you can apply for online in just a few minutes, making it easy to get started with integrated payments.

2. Developer resources

It depends on the integration type:

- API and SDK integrations usually require development support

- Native or browser-based integrations may not

Businesses with custom ecommerce sites, SaaS platforms, or multi-step checkout flows typically benefit from having technical support available.

3. Compatible software

Yes. Your ecommerce platform, POS system, CRM, or accounting software must support integration through:

- APIs

- SDKs

- Native integrations

- Secure connectors

If your software is outdated or proprietary, you may face additional integration limitations.

4. Reliable internet connection

Yes. Payment authorization depends on secure real-time communication between your system, the payment processor, and card networks. If your business operates in locations with unreliable connectivity, you may want a backup connection or offline-capable payment solution.

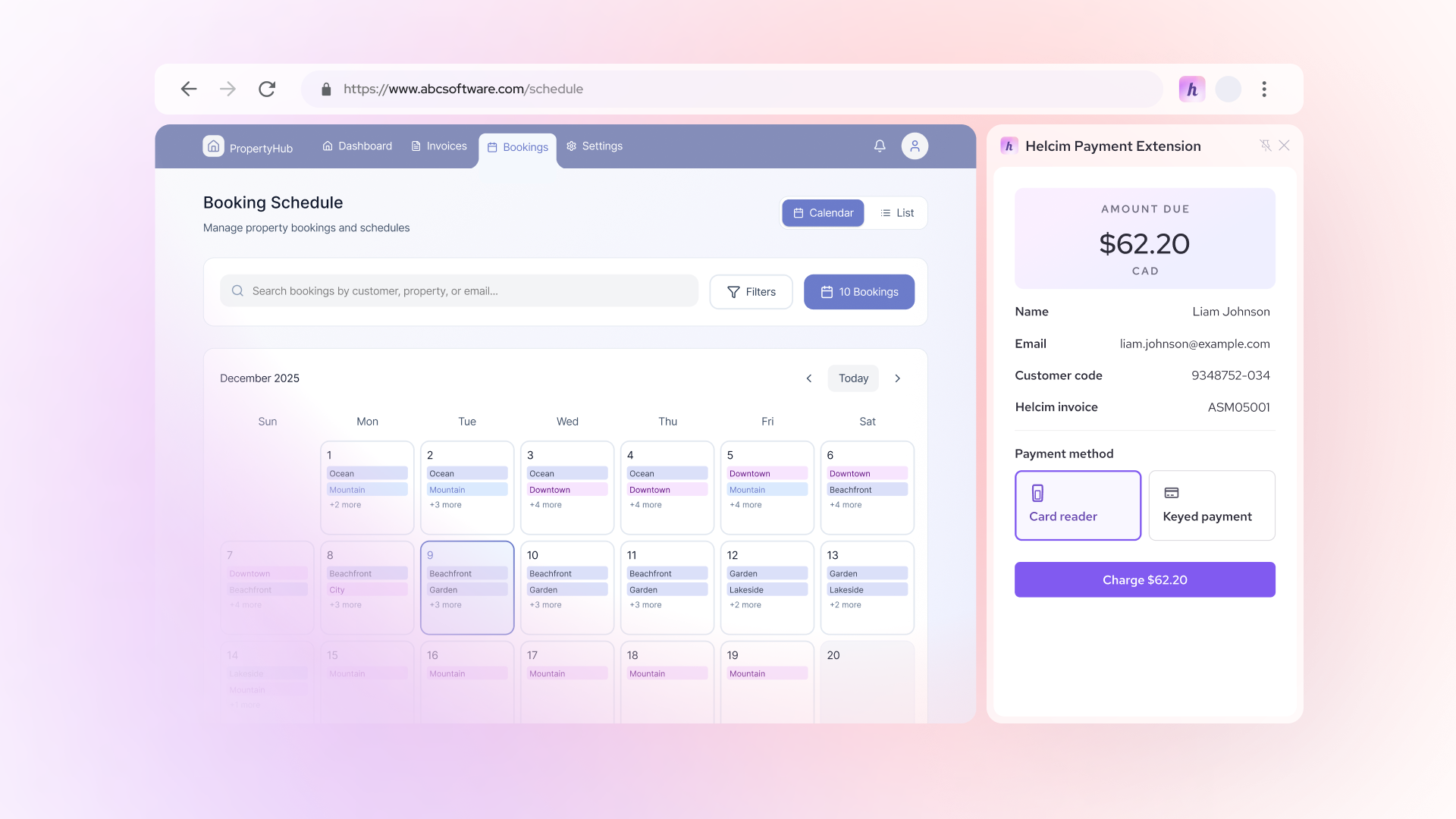

5. Browser-based integrations

For businesses using software with closed payment systems (where traditional integrations aren’t available), browser-based integrations can be a fast and flexible alternative. These solutions work directly through your browser, making it easy to start accepting payments without complex development work.

One example is the Helcim Payment Extension, which enables seamless payment acceptance across a wide range of platforms.

Key benefits include:

- Smart browser automation: Detects payment fields and helps automate payment reconciliation.

- Easy to set up: Get started in minutes with no coding required.

- Wide integration options: Works with 20+ software platforms that use closed payment systems.

Find the Right Integration for Your Business: Not sure which integration is right for you? Visit the Helcim Integration Library to explore all available connection options.

Our Integration Library helps you quickly find the best way to connect Helcim payments to your existing ecommerce platform, POS system, CRM, accounting software, or business tools. Whether you need a native integration, API/SDK solution, secure connector, or browser-based option like the Helcim Payment Extension, you’ll find detailed information to guide your setup.

Is online payment integration secure?

Yes, online payment integration is secure when implemented correctly and supported by a PCI-compliant provider. Most payment processors follow PCI DSS compliance standards and use encryption and tokenization to protect sensitive payment data during transmission and storage. Many providers also offer built-in fraud prevention tools such as AVS, CVV checks, and 3D Secure authentication.

What is PCI compliance?

The Payment Card Industry Data Security Standard (PCI DSS) is a set of security requirements designed to protect cardholder data.

Any business that accepts card payments is responsible for meeting PCI compliance requirements, even if they use a third-party payment provider. PCI DSS is managed by the PCI Security Standards Council.

How does tokenization protect payment data?

Tokenization replaces sensitive card numbers with randomly generated tokens. These tokens can be stored and reused for future payments without exposing the actual card number.

This reduces risk in the event of a data breach and is considered a major security best practice. PCI SSC provides specific guidance in its Tokenization Product Security Guidelines.

Is payment data encrypted?

Yes. Encryption protects payment information while it is transmitted between systems. Encryption ensures that even if data is intercepted, it cannot be read or reused without proper decryption keys.

What fraud prevention tools are available?

Payment processors often provide fraud tools that help reduce unauthorized transactions, including:

- Address Verification Service (AVS)

- CVV checks

- Velocity monitoring

- Fraud scoring and monitoring systems

- 3D Secure authentication

3D Secure adds an extra authentication step during online checkout and is governed by the global EMVCo 3-D Secure standard.

| Criteria | API | SDK | Browser-Based |

|---|---|---|---|

| Setup Time |

|

|

|

| Customization Level |

|

|

|

| Developer required |

|

|

|

| Ideal For |

|

|

|

Why is online payment integration important for businesses?

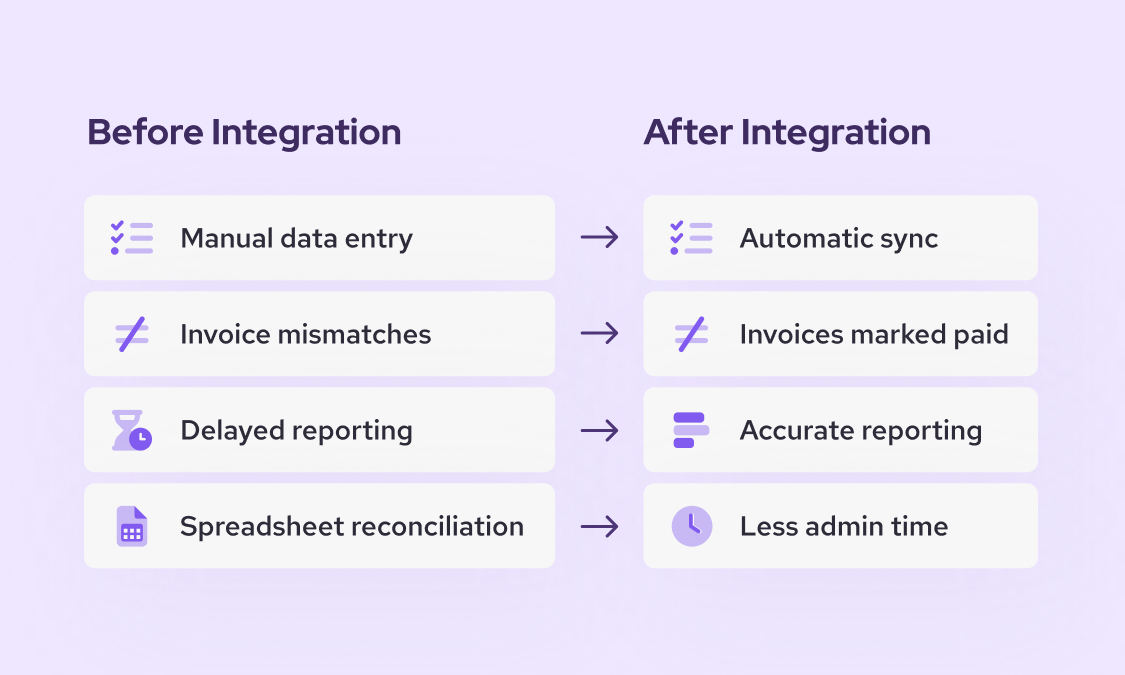

Online payment integration improves more than just checkout speed. It also impacts operations, reporting, and customer satisfaction.

How does it reduce manual errors?

Integrated systems reduce or eliminate duplicate entry, helping prevent:

- Incorrect invoice totals

- Missed payments

- Accounting mismatches

- Customer billing errors

This can save time while improving the reliability of your records.

How does it improve accounting and reporting?

When payments automatically sync with accounting software, reconciliation becomes significantly easier. Finance automation studies consistently show that manual reconciliation and data entry consume a meaningful portion of back-office time, increasing both labor costs and the risk of human error.

Instead of manually matching deposits to invoices, businesses can track:

- Sales trends

- Payment status

- Refunds

- Chargebacks

- Outstanding receivables

This leads to faster month-end close processes and more accurate financial reporting.

Does it improve customer experience?

Yes! Checkout experience directly impacts revenue. According to research from the Baymard Institute, the average documented online shopping cart abandonment rate is approximately 70%, with checkout friction and limited payment options among the leading causes.

Customers benefit from:

- Faster checkout experiences

- Digital wallet support

- Stored payment methods (tokenized)

- Recurring billing options

- Modern payment choices

According to the Federal Reserve Payments Study, electronic payments continue to increase over time, reflecting strong customer demand for digital payment options.

Conclusion: Is online payment integration right for your business?

Online payment integration reduces manual work, improves financial accuracy, strengthens security, and supports modern customer expectations. For businesses looking to streamline operations and scale efficiently, integrating payments directly into core systems is no longer optional — it’s foundational.

If you want to integrate online payment processing into your software with no code or dev resources required, then Helcim Payment Extension is an ideal option. It helps integrate with your business management software quickly through your browser. Besides, Helcim does not charge monthly fees, setup fees, or hidden fees.

FAQ: online payment integration

How long does online payment integration take to set up?

Simple integrations can take a few days. More advanced API integrations may take several weeks depending on testing, compliance, and complexity.

Is online payment integration secure for small businesses?

Yes, as long as you use a PCI-compliant payment provider and follow security best practices like encryption and tokenization. PCI compliance standards are maintained by the PCI Security Standards Council.

Do I need a developer to set up online payment integration?

Not always. Browser-based and native integrations often require no coding. However, custom checkout experiences and advanced automation typically require development support.

Do I need a merchant account for online payment integration?

Yes, in most cases a merchant account is required to process card payments.

What payment methods can I accept with online payment integration?

Depending on your provider, you may be able to accept:

- Credit and debit cards

- ACH bank transfers

- Digital wallets

- International payments

ACH payments in the U.S. operate under rules maintained by Nacha (ACH Network rules).

What challenges should you consider before implementing online payment integration?

Online payment integration may involve technical setup time, compatibility limitations with legacy software, and reliance on provider uptime and internet connectivity. Businesses may also need to train staff and adjust internal workflows. Choosing a reliable payment provider and testing the integration thoroughly can help reduce these risks and ensure a smoother implementation.

What’s the difference between a payment gateway and a payment processor?

A payment gateway securely transmits payment data from your website or POS system to the processor. A payment processor communicates with card networks and issuing banks to authorize and settle transactions. Many modern providers combine both services into a single platform to simplify setup and support.