As a business owner, you have to deal with a lot of things that are far from simple: inventory management, taxes, and accounting, just to name a few. So when it comes to what you pay in credit card processing, a simple calculation that doesn't change can be an attractive option for your business. But is flat rate the best pricing model for your business? Here's what you need to know about how flat rate pricing works.

What is flat rate credit card processing?

Before we dive into the flat rate pricing model, it’s important to know that it’s just one of several pricing strategies out there for handling merchant discount fees. The three main models you’ll encounter are Flat rate, Tiered pricing, and Interchange plus.

Flat rate pricing

Also called flat fee processing, flat rate pricing is straightforward. Your payment processor charges you a fixed rate on every credit card transaction—regardless of the card type or its specific interchange rate. For example, whether it’s a basic Visa Debit or a premium Amex OptBlue, the rate stays the same. However, the rate might vary depending on how the type of transaction that is processed:

- Card-Present (chip and PIN/swiped) transactions usually come with a lower flat rate.

- Card-Not-Present (manual entry/online) transactions are charged a higher flat rate due to increased fraud risks.

So while you’re getting one consistent rate across all cards, there’s still some difference depending on how the payment is made.

Beyond flat rate pricing

Interchange plus pricing

Interchange Plus pricing model gives small businesses more transparency. Unlike flat rate pricing, which charges a fixed fee for every transaction, with interchange plus pricing, you get the actual network rate (which varies by card type) plus a small, fixed markup from the processor. Think of it as getting the true “wholesale” cost of processing the payment plus a small margin. It’s often cheaper for businesses with high transaction volumes or a mix of card types because you benefit from the lower interchange fees where they apply.

Tiered pricing

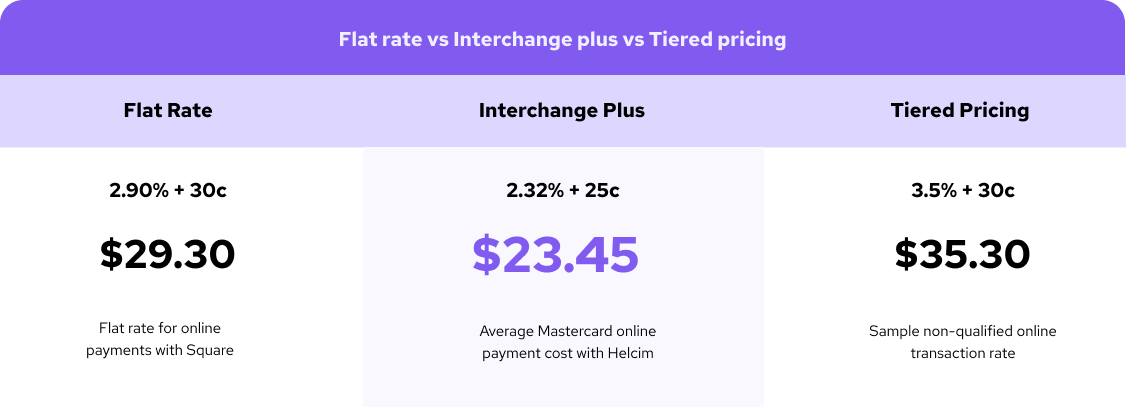

This model bundles transactions into categories like “qualified,” “mid-qualified,” and “non-qualified,” with different rates for each. This model can be hard to navigate because it’s less transparent, and the highest tiers can be pricey. Here's an example of a $1,000 card-not-present transaction using a Mastercard to better illustrate the difference between the three pricing structures:

In short, flat rate pricing offers predictability, but it doesn’t give you the flexibility or savings that interchange plus might, especially as your business grows. So yes, it’s simple, but that simplicity comes at a cost—literally.

Is flat rate pricing model processing a good deal?

The biggest selling point of flat rate pricing is predictability. If you’re a small business with low monthly processing volume or lots of small, low-cost transactions (think: a coffee shop selling $3 cappuccinos), a fixed price can seem like a dream. You know what you’re paying each time, there are no surprises, and it’s easy to factor into your budget. Flat rate pricing eliminates uncertainties and makes it easier for businesses to budget.

But here’s where the plot thickens. Flat rate pricing is like having a subscription for “one-size-fits-all” shoes. It’s simple, but once your feet (aka your business) grow, those shoes start pinching—hard. The flat rate pricing structure is designed to offer predictability and simplicity, but it may not always be the most cost-effective option as your business grows.

For instance, if you’re paying a flat rate of 2.9% on every transaction, but the actual interchange rate (the fee that the credit card companies like Visa and Mastercard charge) for some of your transactions is only 1.5%, you’re effectively paying a lot more than you need to. You’re covering the processor’s cushion—extra money they pocket to hedge against the variability of interchange fees.

Just like our example above, when you process a $1,000 transaction at a 2.9% flat rate. That’s $29 in fees. But if the true interchange fee is just 1.5%, you’re paying too much per transaction. Multiply that across hundreds of sales, and suddenly, your “simple” flat rate is costing you hundreds or even thousands more each month.

What are typical flat rate fees and how to calculate flat rate pricing?

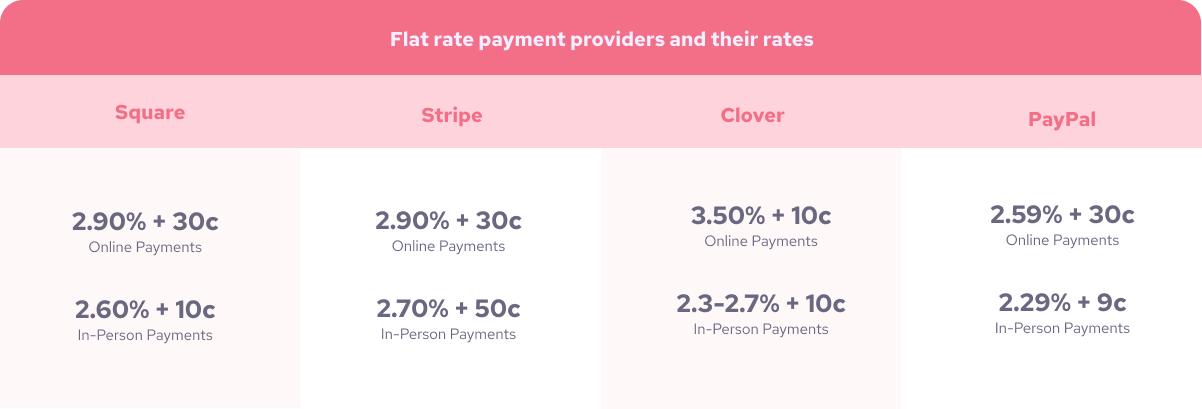

To give you an idea of what other flat rate payment providers typically charge, here’s what you can expect in terms of their fees:

[ ]

]

While flat rates are simple and easy to understand, keep in mind that actual interchange rates are often much lower—meaning you could be overpaying. Curious how much you could save by switching to Helcim? Check out our rate comparison tool and discover your potential savings!

What’s the alternative? Enter interchange plus pricing

If flat rate pricing is the "easy button," interchange plus pricing is more like paying à la carte. It’s still straightforward, but it’s also more transparent and potentially cheaper in the long run.

With interchange plus pricing model, the processor charges you the actual interchange rate (set by the card networks) plus a small, fixed margin for themselves. This means you’re paying what each transaction truly costs—no extra padding for the processor. The margin the processor adds stays consistent (or in the case of Helcim, this margin decreases when you process more), but the interchange rates fluctuate depending on factors like the card type (a standard Visa vs. a fancy rewards card) and how the payment is processed (swipe vs. online).

For example, with Helcim, you pay 0.25% above the actual interchange fee for card-present transactions. So, if the interchange fee is 1.5%, your total processing fee is 1.75%, which is way better than a flat rate of 2.9%.

Interchange plus vs. flat rate: When does it make sense?

Flat rate processing can make sense for businesses that:

- Have low monthly transaction volumes (under $10,000).

- Mainly process small, low-ticket transactions in person (under $15 per sale).

- Need a no-fuss, predictable rate that’s easy to calculate and doesn’t fluctuate. For example, a small coffee shop with $3 sales might love the simplicity of flat rate pricing. But if you’re running a larger operation, or if your business grows beyond a certain point, interchange plus pricing will almost always save you more in the long run.

Interchange plus on the other hand, can be a better option for most businesses, especially those that:

- Process high monthly volumes: The more you process, the more you stand to save with interchange plus, since you’re not stuck overpaying on each transaction.

- Have higher-value transactions: If your sales tend to be larger (think: e-commerce, luxury retail, B2B), paying a flat 2.9% on a $1,000 sale vs. 1.75% can add up quickly.

- Have a mix of card types: Flat rate lumps all cards together. Interchange plus adjusts for each card type, so you save on transactions with lower interchange fees.

The bottom line: Are you overpaying with flat rate pricing?

Flat rate credit card processing is like the fast food of payment options—quick, easy, and predictable, but not necessarily the healthiest (or most cost-effective) choice in the long run. If you’re a small, low-volume business, it might work fine for now. But as your business scales, the convenience of flat rate pricing often gets outweighed by the savings potential of interchange plus pricing.

Want to see how much you could save with a more transparent, cost-efficient pricing?

Switch to Helcim for a more affordable payment processing. Sign up for free here or submit your statement now and we’ll provide a custom savings estimate—because at the end of the day, saving money on processing fees means more profits for your business.