Most small businesses face the same challenges when it comes to credit card transaction fees - it's yet another overhead expense which chews away at profits due to the multitude of fees that the modern-day merchant pays.

While some credit card processing pricing models offer more savings than others (see Helcim Interchange Plus pricing), it can still be frustrating to accept certain types of payment methods with a higher interchange rate or processing fee, or resort to age-old tactics like minimum purchase requirements or cash only transactions.

With the total amount of credit card transactions rising above $50 billion USD from consumers annually, merchants passing on their processing fees to customers (through mediums such as credit card surcharges) has been one of the most important financial decisions made by businesses worldwide, but not without gaining controversy from government agencies, card brands, and consumers alike.

Key points and FAQs

What is a credit card surcharge?

- A credit card surcharge is a fee that a merchant can choose to impose when the customer or client chooses to pay via credit card.

Merchant options to offset payment processing fees:

-

A merchant has three main methods of passing on their credit card processing fees for their customers to pay: <BR>

- Apply a credit card surcharge

- Charge convenience fees, or

- Impose a service fee.

-

Alternative and less popular methods to offset higher processing fees include:

- Only accepting debit cards,

- Accepting ACH bank payments as the primary transaction type,

- Offering cash discounts, or

- Implementing a minimum purchase requirement.

How can I surcharge on credit card transactions legally?

The legal landscape for surcharging is complicated: there are certain rules in accordance with country laws, state laws, card network requirements, and card brands (such as Mastercard or Visa cards) when deciding to apply credit card surcharges.

In the United States, the surcharging rules are:

- The surcharge amount that the merchant adds must be disclosed on every receipt as a separate line item. In the state of New York, businesses are required to display the total price of products or services, including any credit card surcharges, before customers complete their checkout. Owners have the option to either show a single total price that includes the credit card surcharge or to display distinct prices for payments made with a credit card versus cash.

- The merchant must disclose the extra fees through in-store signage or list surcharges online

- You must notify the financial institution or credit card brands of your decision on imposing surcharges (or let your payment processor handle the communications),

- A credit card surcharge is capped at 3% for Visa cards and 4% for Mastercard,

- Surcharging is not allowed in Massachusetts, Connecticut, or Puerto Rico, and Colorado merchants cannot apply a credit card surcharge above 2%,

- Credit card surcharges cannot be applied to debit card transactions and prepaid cards.

- If a merchant chooses to impose credit card surcharges, they cannot choose to charge convenience fees or a service charge in conjunction.

In Canada, the surcharging rules are similar with a few caveats:

- The surcharge amount must be disclosed on every receipt as a separate line item.

- The merchant must disclose the extra fees through in-store signage or list surcharges online.

- You must notify the financial institution or credit card brands of your decision to implement surcharges (or let your payment processor handle the communications),

- A credit card surcharge is capped at 2.4% for all card brands.

- Credit card surcharges may not be applied to debit cards, only credit card purchases.

- If a merchant chooses to impose credit card surcharges, they cannot choose to charge convenience fees or a service charge in conjunction.

Our recommendation on credit card processing fees:

To ensure complete credit card surcharging compliance, use a tool like Helcim Fee Saver to seamlessly pass on your credit card fees to your customer, and take advantage of Helcim's competitive rates.

Different types of fees

As a business owner, you have three main methods of passing on fees associated with accepting payments : Surcharging, service fees, and convenience fees.

There is some controversy surrounding the choice to charge an additional fee. Many are wondering what options are available to them to pass on processing costs, especially those using an online payment solution, without offering arbitrary methods such as a cash discount or a minimum purchase amount.

Ultimately, it comes down to the **decision of the merchant **whether to impose surcharges or another additional fee on credit card transactions. Remember to weigh the potential financial benefits against the impact on customer relationships. Transparency and open communication can go a long way in ensuring a positive experience for both you and your valued customers.

What is surcharging, and are credit card surcharges legal?

Applying a surcharge on credit card transactions that your customers pay is one way to offset your payment processing fees. When deciding to implement surcharges, one consideration is that merchants are required to give the choice to either accept the surcharge fee, or opt for an alternative payment method, such as ACH bank payments, wire transfers, or cash.

When a consumer chooses credit card payments, payment processors charge a fee for each transaction. Such costs can add up, especially if you process a high volume of credit cards.

There are two types of credit card surcharges to consider: A brand level surcharge and product level surcharge. A brand level surcharge applies to all cards of a particular brand, such as Visa or Mastercard, and even debit and prepaid cards. On the other hand, product level surcharges vary depending on certain card types within a brand, like the TD® Aeroplan® Visa Infinite Card.

Credit card surcharge laws for the United States:

In the United States, credit card surcharges are legally allowed across most states, except for Massachusetts, Connecticut, and Puerto Rico. In addition, merchants located in Colorado may not surcharge more than 2.0% of the total purchase price as per state laws.

The cap for credit card surcharges vary based on brand - 3% for Visa and 4% for Mastercard. Most United States merchants opt to cap these at 3%.

Credit card surcharge laws for Canada:

Following changes to federal laws in October 2022, credit card surcharging has also made its way into Canada (except Quebec), offering merchants an additional avenue to address credit card transaction costs.

Canadian merchants have an absolute maximum surcharge cap of 2.4% of the total cost of the transaction.

Credit card surcharge laws for all of North America:

A business who decides to surcharge credit cards must display a notice of this fee on their storefronts or website. They must also prompt the customer at the time of sale to accept the itemized cost on top of the total so that people will know prior to purchasing that they will pay a surcharge. Finally, the surcharge must be listed as a separate item on the transaction receipt.

Merchants throughout North America can not apply surcharge fees to debit card transactions, as credit card surcharge laws only permit an additional fee to be applied to credit card payments specifically.

Most, if not all merchants are eligible to implement credit card surcharges, but will need approval from their payment processors or acquirer and the card network / card brand.

Some card network brands prohibit some municipalities, government agencies, educational institutions, and courts from applying surcharges to credit cards, which will need to be checked with the issuer or card brand.

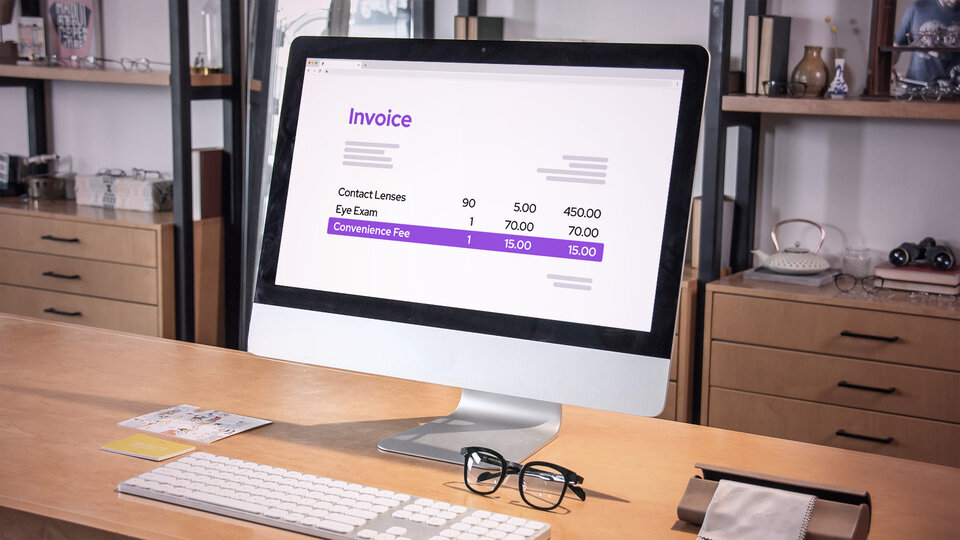

As an alternative, how can I charge convenience fees?

Convenience fees often come into play for card-not-present transactions, such as online payments or invoices, and are added to the total cost paid by the customer. Merchants may choose to impose convenience fees to offset the cost incurred from certain transaction methods such as online payments or invoicing.

This approach not only helps a business to recoup expenses but, like surcharging, sometimes convenience fees can act as an incentive to opt for more cost-effective payment methods like ACH transactions.

Convenience fees vs. surcharges:

While credit card surcharges only apply specifically to credit card fees, there's another way to pass on fees called a convenience fee. These are charged by a business to cover the cost associated with offering convenience in certain payment methods. Credit card surcharging is different in that it can only be applied to credit cards, and won’t require an alternative option of payment.

With convenience fees, a merchant still needs to disclose the fee prior to the transaction, but a written notice is not technically required, nor a receipt. Merchants may still want to communicate this out of transparency.

Both surcharges and convenience fees have their place in the business landscape and are legal in most regions, including Canada and the U.S. Again, most merchants are eligible to implement a convenience fee, but will need approval from their payment processors or acquirer and the card network. They will not be able to implement both a surcharge and a convenience fee.

If your business allows customers to pay with expensive transaction types and doesn't solely rely on credit cards, incorporating convenience fees can be a great solution. By strategically implementing convenience fees, businesses can strike a balance between offering a wide range of payment options and managing their cash effectively.

What about a service fee?

Finally, have something called a service fee. It's an additional charge to pay in addition to the purchase, different from credit surcharging, and falls under the broader category of convenience fees.

What industries are service fees applicable to?

These aren't common at your everyday retail business, but in various industries like registries, banking, and travel, these charges help cover the extra services that come with what you're buying. Whether it's customer-specific services or the behind-the-scenes administrative work, some businesses need a little extra to keep things running smoothly. Not all are eligible to impose service fees, so they will need to check their local legislation as well as notify their acquirers before expecting consumers to pay them.

Service fees are not the same as tipping. Tips go directly to the employees who serve you, but service charges are where businesses get a boost to handle their expenses and provide you with top-notch service.

Navigate credit card surcharges, convenience fees, and service fees with Helcim Fee Saver

Unsure about surcharging? Wish there was an easier way to pass on fees? Enter Helcim Fee Saver, the effortless tool that simplifies surcharging and convenience fees and empowers your choices. Imagine seamlessly adding a surcharge option to your In-person payments via the Helcim Smart Terminal or Convenience Fees to invoices and online payments without the headache of manually calculating processing fees or jumping through hoops. It's just one toggle to savings!

Explore Helcim Fee Saver to learn more!