What is a surcharge fee?

First, let’s define a surcharge fee: A surcharge fee is a fee charged by a business owner to cover the cost of a transaction when a customer pays via credit card.

When a merchant chooses to accept credit cards and process credit card transactions, there are merchant discount fees associated which has traditionally come out of the merchant’s pocket. With surcharges, also sometimes referred to as free or zero-fee credit card processing, the customer is prompted at the time of payment and given a choice to accept the surcharge fee for using a credit card or opt to use another form of payment.

There are two types of surcharges: Brand level vs. product level surcharges.

- Brand level surcharge - surcharge applied to all cards of a certain brand.

- Product level surcharge - surcharge applied to certain card types within a brand. Product level surcharges are not easily understood by customers and are not always practical.

Note: Merchants can only use one type of surcharge (not both), and anti-competitive clauses may be in effect for various card brands, which prohibit selective surcharging by brand or product and call for uniform charging across levels.

Read: Convenience fees vs. Sucharge

Is it legal to charge a credit card fee?

Surcharging in Canada

Canadian merchants plead their case to ease the burden of interchange rates (set by the card brands) that has cost merchants millions. Despite multiple deals with credit card companies since 2020 that were meant to lower credit card fees (forecasted to save businesses over a quarter million per year), the increase in credit card transactions has meant increased fees, especially for smaller businesses.

Thus, the idea of surcharges has been at the forefront of concern for Canadian business owners, with major brands like Mastercard adjusting their merchant rules, which could be a way to offset the cost of the credit card processing fees by offloading this cost to cardholders as an extra expense at checkout.

Surcharging in the United States- Not yet accepted everywhere

In the United States, card brands allow surcharges if you follow each card brand’s specific guidelines as outlined in their merchant agreement if your business does not operate in one of the states that ban credit card surcharges.

States are adjusting their laws quickly, and the topic of surcharging has been heavily discussed. Colorado passed a new surcharge law in July of 2021, leaving only Massachusetts, Maine, and Connecticut as the only states with surcharge bans. There are specific laws, which go into more detail, within the several states regarding surcharging.

Connecticut

In Connecticut, general states that surcharging based on the payment method is prohibited. “No seller may impose a surcharge on a buyer who elects to use any payment method, including, but not limited to, cash, check, credit card or electronic means, in any sales transaction.”

Massachusetts

Section 28A of the Massachusetts state law states that no seller in any sales transaction may impose a surcharge on a cardholder who elects to use a credit card in lieu of payment by cash, check, or similar means.

New York

In New York, starting February 2024 businesses are required to display the total price of products or services, including any credit card surcharges, before customers complete their checkout. Owners have the option to either show a single total price that includes the credit card surcharge or to display distinct prices for payments made with a credit card versus cash. Additionally, the new regulation mandates that any surcharge applied to customers who use credit cards must match the exact fee charged by the credit card companies.

Colorado

In Colorado, merchants can apply up to a 2% surcharge or charge the actual credit processing cost, with most capping the surcharge at 2% due to varying costs.

Surcharges in Canada: What you need to know

While this controversial model has already been accepted by our U.S. neighbor for the most part, surcharges are new to Canada this October (2022). Consumer protection laws in Quebec mean that Quebec businesses are still ineligible to participate in surcharging but for other provinces, Both Visa and Mastercard have released detailed guidelines for how merchants should go about passing a surcharge on in their usage rules for merchants.

When it comes to whether or not to pass on credit card processing fees to your customers and who pays for credit card processing fees, it's always best to consider best practices in order to maintain customer loyalty, goodwill, and transparency. However, in this article, we’ll give you the Cole’s notes on what to do to save you a thorough read of all their terms and conditions.

Playing by the rules: How do surcharge fees work?

There are a few stipulations surcharges must follow. Below we will take a deep dive into the rules of the game.

Different states and provinces have different laws so be sure to read up on your states legislation as well as the card brand rules to get a full understanding before implementing surcharges. Surcharges are currently illegal as of October 2022 in Massachusetts, Connecticut, Maine, and Quebec.

No cherry picking: equal surcharging across card brands

Depending on your state or provincial laws, card network regulations, and payment processors, anti-competitive laws may state that you can’t discriminate against card brands or types. If you apply a surcharge, you must do so equally. For example, you may not be able to charge the processing cost for AMEX credit cards but not Visa.

Generally, the easiest way for a merchant to get started in implementing surcharging is to have a uniform brand level surcharge and credit card surcharging for all credit card transactions.

It is also important to note that to implement a surcharge on Mastercard transactions, you must inform both Mastercard and your acquirer (the bank or entity processing credit card payments) 30 days before starting. This involves completing an online disclosure form and also communicating separately with your acquirer. For adding a surcharge to Visa transactions, notification is not required.

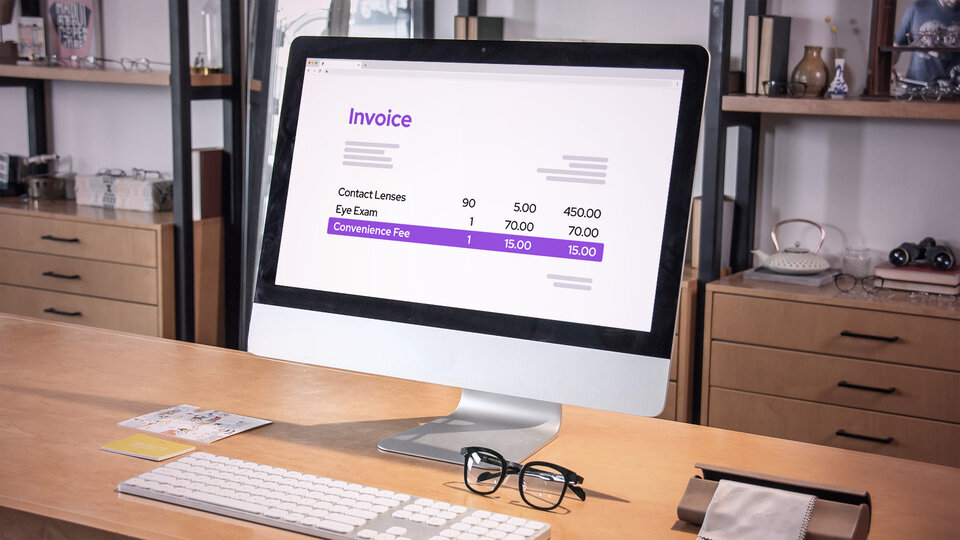

Merchants must disclose surcharge fees

To impose surcharge fees for credit card transactions, merchants must also clearly disclose this to cardholders at the storefront and during the POS (point of sale) purchase (for both in-person or e-commerce transactions.) This means that the POS system the merchant uses must display the surcharge fee as a separate item on the terminal or card reader and include the option to change payment methods or accept the credit card surcharge. Merchants must also specify at the storefront or on their online credit card brand page that their fee is not greater than their cost.

There are regulations around how you inform cardholders — surcharge fees should be calculated and presented at checkout as a separate cost in addition to the total. Merchants are mandated to provide a prompt to switch to an alternative payment method to mitigate this cost or to inform customers who choose to accept it and continue to pay with their credit card. The surcharge fee must also be shown on the customer’s receipt as an itemized cost.

Additionally states like New York, as mentioned above, would require additional disclosure measures in order to implement surcharging so it is always a good idea to check whether your local legislations have updated their surcharging laws.

It's also important to note that different card brands have specific caps on how much you can charge — Mastercard and Visa websites state the maximum surcharge is 2.4% in Canada and 3% in the U.S. even when the merchant discount rate is higher — although some other card brands may differ.

FAQ's

1. How much can a merchant charge for surcharge fees?

There is usually a capped amount a merchant may issue to their customer for each card brand. Merchants can find this information by heading to the card brand's website and clicking through to rules and guidelines. Mastercard and Visa surcharge policies state 2.4% in Canada and 3% in the U.S.

It can vary by card brand, so contact your payments company if you’re curious about other card brands your business accepts.

2. What is the difference between convenience and surcharge fees?

This is a fee charged for offering a payment method that is an alternative to standard payment options. For example, if a company typically accepts payments in-person but also offers the convenience of paying online or over the phone, they might charge a convenience fee for these alternative payment methods.

On the other hand, surcharging is an additional fee that a merchant adds specifically for the use of a credit card (and in some cases, debit cards) to cover the cost of credit card processing fees.

A merchant cannot impose both surcharging and convenience fee on a single transaction.

3. Can you surcharge debit cards?

Merchants cannot impose surcharge to debit cards and prepaid cards in the US even if they operate in the credit card rails. For Canadian Interac Debit however, starting January 26, 2024, surcharges are permitted when multiple debit networks are present at the POS, not exceeding others’ rates. Surcharges are capped at $0.25, must appear on transaction records, and be enforced by the merchant's acquirer.

4. What type of cards and transactions can I surcharge?

The rule of thumb is that businesses can add a surcharge to any credit card transaction, whether in-person, keyed-in (over the phone) or online.

Canadian merchants can apply surcharges to credit card transactions in one of two ways: Brand level or product level surcharges.

A brand level surcharge is applied to all cards of a particular brand, whereas product surcharges are applied to specific card types within a brand. Note: Merchants can only implement one type —not both. Anti-competitive laws may impact how merchants can utilize these types of surcharging methods.

5. Where can I find more details on the card-brand rules regarding surcharging?

You can read more about Mastercard’s surcharge rules and Visa Surcharge FAQs here.