-

Content

Last Updated on May 14, 2025 by Robert Luong

A credit means money goes into your account. A debit means money goes out. Simple, right? But once you start setting up ACH payments for your business, those old definitions suddenly feel complicated. You’ll hear terms like ACH credit and ACH debit, and wonder—what’s the real difference? Let’s explore these two terms in this article.

What is an ACH credit transaction?

An ACH credit transaction happens when the funds are "pushed" (deposited) into your bank account. Overall, whenever you receive payments through the ACH network, that transaction is called ACH credit transaction.

Example: As a seller (recipient point of view), you are receiving ACH transfers from your buyers (senders). As an employee, you are receiving paycheck through ACH. As a citizen, you receive a tax refund via an ACH credit.

What is an ACH debit transaction?

An ACH debit transaction happens when funds are "pulled" (withdrawn) from your bank account. When a customer authorizes a direct payment, a depository financial institution (bank or credit union) receives a request from the biller's bank, and the funds are transferred through the ACH system.

Example: When you fill out that bank authorization form with the cell phone company, you allow them to charge your account via ACH. Every month when your bill is due, funds are automatically withdrawn from your account to pay the bill. This transaction is called an ACH debit transaction.

What are the differences between ACH credit and ACH debit transactions?

There are five key differences between ACH credit and ACH debit transactions:

- Who initiates the transaction

- Direction of fund flow

- Purpose of the transaction

- How the transaction is initiated

- Who benefits most

| Key difference | ACH credit | ACH debit |

|---|---|---|

| Who initiates the transaction | Sender (e.g., customer, buyer, employer) | Recipient (e.g., merchant, seller) |

| Direction of fund flow | Funds are pushed into the recipient's account, increasing their balance. | Funds are pulled from the sender's account, decreasing their balance. |

| Purpose of the transaction | Used to pay bills, send payroll, make purchases, issue refunds, or reimbursements. | Used to automatically collect recurring or scheduled payments from customers. |

| How it is initiated | Sender authorizes and initiates transfer to recipient’s bank account. | Sender authorizes recipient to initiate transfer from sender’s account. |

| Who benefits most? | Both sender and recipient benefit. The sender saves time and avoids late payments, while the recipient receives funds on time and at a low cost. | |

What are different types of ACH debit and ACH credit payments?

When a business or customer sends or receives an ACH payment, the type of transaction is labeled using something called an SEC (Standard Entry Class) code.

Common types of ACH credit transactions

- CCD (Corporate Credit or Debit Entry): Used when a business pushes funds to another business—for example, paying a supplier or vendor.

- CTX (Corporate Trade Exchange): Similar to CCD but used for corporate or government payments.

- CIE (Customer Initiated Entry): Occurs when a customer initiates a payment to a business, like paying a utility bill through their bank’s online system.

- PPD (Prearranged Payment and Deposit): Used to push funds into a recipient’s account, such as payroll direct deposit, government benefits, or pension payments.

- IAT (International ACH Transaction): Used to receive cross-border payments.

- WEB (Internet-Initiated Entry): Occurs when a consumer authorizes a business to receive a one-time or recurring payment online.

- MTE (Machine Transfer Entry): Used to push money into a recipient’s account via ATM. For example, when someone deposits cash at an ATM.

- POS (Point of Sale Entry): Used when a business refunds a customer at an in-person POS terminal.

- SHR (Shared Network Transaction): Used when a shared ATM network credits a customer’s account. For example, a deposit made through a partnered financial institution’s ATM.

Common types of ACH debit transactions

- PPD (Prearranged Payment and Deposit): Used when a business pulls funds from a consumer’s account for recurring payments like monthly utility bills, or gym memberships.

- WEB (Internet-Initiated Entry): Used when a customer authorizes an online business to pull payments from their account for eCommerce, or any other online payments.

- TEL (Telephone-Initiated Entry): Occurs when a customer provides an authorization over the phone, allowing a business to take funds from their account.

- ARC (Accounts Receivable Entry): Used when a business converts a check received by mail into an ACH debit payment.

- BOC (Back Office Conversion): Converts a paper check handed in person into a debit ACH payment during back-office processing.

- POP (Point of Purchase Entry): Converts a check written in-store at the point of sale system into an ACH debit, allowing the merchant to collect ACH payment electronically.

- RCK (Re-presented Check Entry): Used by a business to retry collecting a bounced check by re-submitting it electronically as an ACH debit.

- TRC/TRX (Truncated Check Entries): Used by businesses to scan and store paper checks electronically, allowing them to collect payments without keeping the physical check.

- POS (Point of Sale Entry): Used when a business pulls funds from a customer’s account at a credit card machine using a debit card linked to their bank account.

- MTE (Machine Transfer Entry): Debits a customer’s account when they withdraw money from an ATM or transfer funds using an ATM interface.

- SHR (Shared Network Transaction): Debits a customer’s account through a transaction routed across a shared ATM or POS network.

What are the typical use cases for ACH credits and ACH debit in businesses

If you're a merchant who wants to accept ACH payments, you'll likely need to process ACH debit transactions. This allows you to initiate the transfer and pull funds directly from your customer's bank account into yours with their prior authorization. ACH debits are ideal for:

- SaaS businesses and gyms: Automatically collecting recurring payments for subscriptions or memberships.

- Installment-based businesses: Pulling scheduled payments for subscription plans or financing agreements.

- Professional services: Collecting large invoices or recurring retainers with lower processing fees than credit cards.

On the other hand, if you're a customer or business that wants to pay bills on time, you’ll use ACH credit transactions. In this case, you initiate the payment and push funds from your account to the seller's bank account. This is common when:

- You're paying vendors or suppliers directly through online banking.

- You’re sending payroll or issuing refunds.

- You want to keep control over when funds leave your account.

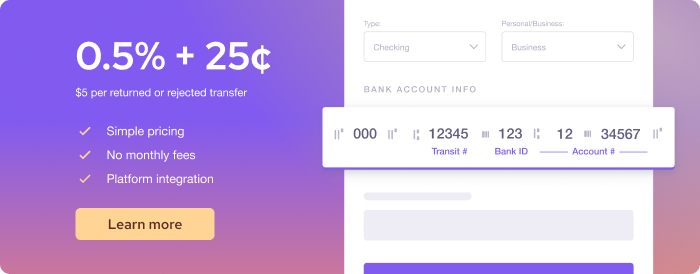

Process ACH transaction at low costs with Helcim

Helcim makes it easy and affordable to accept ACH credit transfers. Helcim ACH processing fee is just 0.5% + 25¢, capped at $6 per transaction under $25,000. That means big savings—especially for high-ticket or recurring payments.

You also get access to powerful, no-monthly-fee tools that let you accept ACH payments online:

- Invoicing: Send professional invoices and automate payment reminders.

- Virtual terminal: Accept payments right from your computer for one-time or overdue invoices.

- Recurring payment software: Set up automatic billing for subscriptions and payment plans.

- Payment pages: Create a branded checkout page and embed a “Pay Now” button on your website.

No monthly fees. No hidden costs. No long-term contracts. Just simple, low-cost ACH processing to help you get paid faster.

FAQs

Why was money debited from my account through ACH?

An ACH debit means someone you authorized—like a company or service provider—pulled money from your bank account. This often happens for things like bills, subscriptions, or loan payments. If you didn’t authorize the charge, it could be an error or potential fraud. Check with your bank or the company to confirm the source.

How can I stop an ACH debit transaction?

To stop an ACH debit, contact your bank and request a stop payment order. You should also notify the company that’s pulling the funds and cancel any authorizations. Banks usually require advance notice and may charge a small fee. If the transaction was unauthorized, report it immediately to your bank.

Can ACH debits or credits be reversed?

Yes, both ACH debits and credits can be reversed under certain conditions. For example, if there was an error, duplicate transaction, or fraud, a reversal may be requested. However, reversals must meet strict rules and time limits. Contact your bank or the payment sender as soon as possible if you spot an issue.

Why did I receive an ACH credit in my bank account?

An ACH credit means someone pushed money into your account electronically. It could be a paycheck, tax refund, reimbursement, or payment from a business. These are usually scheduled payments from senders you know. Check your transaction details or contact your bank to confirm the source.

How can I find out where an ACH credit came from?

Your bank statement should show the sender’s name or a transaction code tied to the ACH credit. You can also contact your bank for more details if the description is unclear. In most cases, the sender is a company, government agency, or employer. If the payment seems suspicious, report it to your bank immediately.

How does a direct deposit work through the ACH system?

Direct deposit is a type of ACH credit where your employer, government agency, or other payer pushes funds into your account. The process starts with the originating depository financial institution (ODFI)—usually the payer’s bank—sending the transaction through the ACH system. Your bank or receiving depository financial institution (RDFI) then accepts the funds and credits your account.