If you’ve heard about ACH payments or direct deposits but aren’t sure how they can benefit your business, you’re not alone. ACH has been around for decades, yet many businesses are still unclear on the advantages it offers. This cheat sheet will guide you through everything you need to know about ACH payments—from what they are to how you can start accepting them in your business.

The quick rundown: What Is ACH and why should you care?

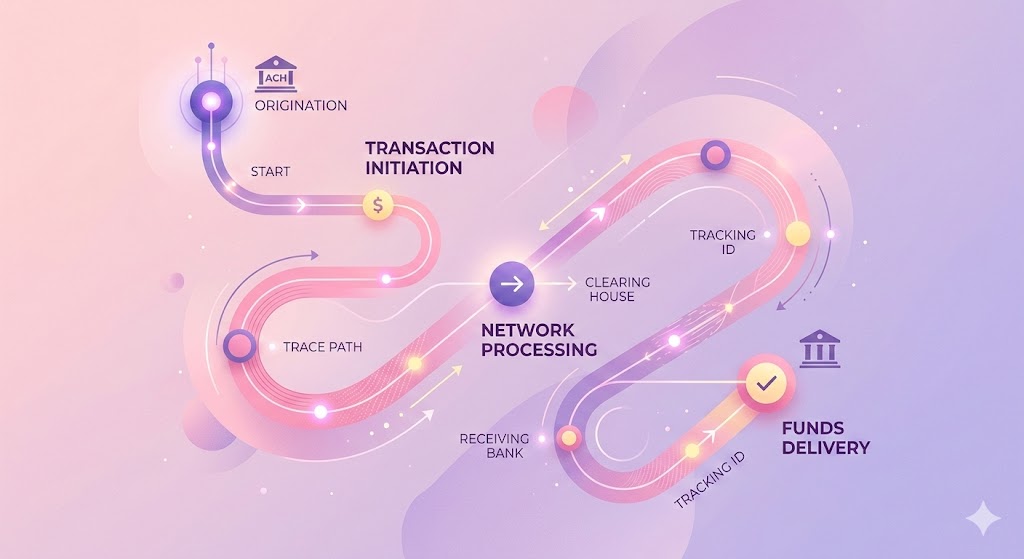

ACH payments are a secure and reliable way for businesses to get paid directly through bank transfers. It’s a payment method where funds move between bank accounts electronically through the Automated Clearing House network. Unlike credit card payments, ACH is typically more cost-effective and doesn’t come with high processing fees. Compared to check payments and e-transfers, ACH is faster, automated, and more streamlined, making it ideal for recurring payment processing and improving cash flow predictability.

- ACH: Stands for Automated Clearing House. In Canada, it’s known as Electronic Fund Transfer (EFT).

- Purpose: Created in the 1970s to reduce the need for paper checks by processing electronic payments between bank accounts.

- 2023 stats: The ACH network processed nearly 31.5 billion payments, totaling an astounding $80.1 trillion, highlighting its crucial role in the U.S. and Canadian banking systems.

ACH payments bring several benefits to the table:

- Cost savings: ACH transactions are typically much cheaper than credit card transactions or wire transfers, which means more savings for your business.

- Better cash flow: By scheduling payments through ACH, you can make your cash flow more predictable. This helps with automating things like payroll, vendor payments, and customer billing.

- Increased security: All payments are encrypted and monitored for ACH fraud, making them a safer option compared to paper checks for both businesses and customers.

- Convenience: ACH allows for automatic recurring payments, which reduces the manual work for you and lets you focus on growing your business.

- Greater transaction capacity: ACH payments allow for higher-value transfers compared to e-transfers, making them ideal for businesses handling large transactions, reducing the need to split payments and simplifying financial management.

The big question: Are ACH payments really cheaper? (Spoiler: yes, they are!)

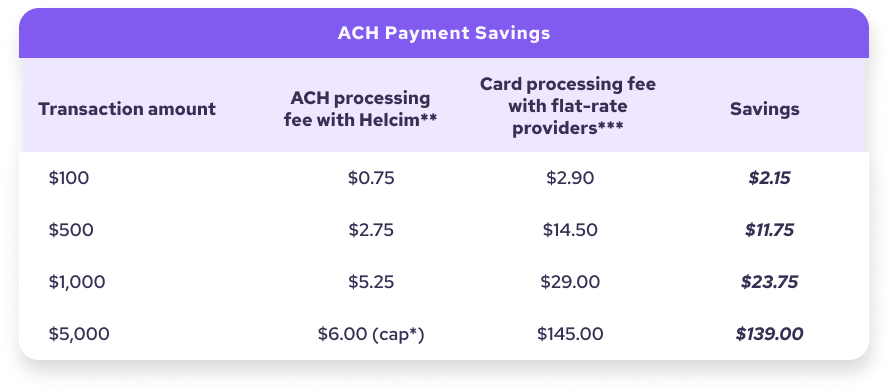

ACH payment fees are usually lower than credit card processing fees. Most providers charge between 0.5% and 1.5% per transaction, but some, like Helcim, offer a cap on fees to help you save even more.

*up to transactions worth $25,000 **based on Helcim’s ACH rates at 0.5% + 25c capped at $6 ***based on average market flat-rate providers 2.9%

Great, you're sold! So what’s next?

Finding the perfect payments provider: What to look for

First things first—choosing the right provider is key. You’ll probably want to consider:

- Fees: Look for a provider with competitive rates. For instance, Helcim charges just 0.5% + 25 cents per transaction and caps the fee at $6 for transactions up to $25,000.

- Processing times: Standard ACH payments usually settle within 1-4 business days, but some providers offer same-day processing for an extra fee.

- Customer support: Reliable support is a must in case you run into any issues like chargebacks or fraud.

Setting up your ACH merchant account

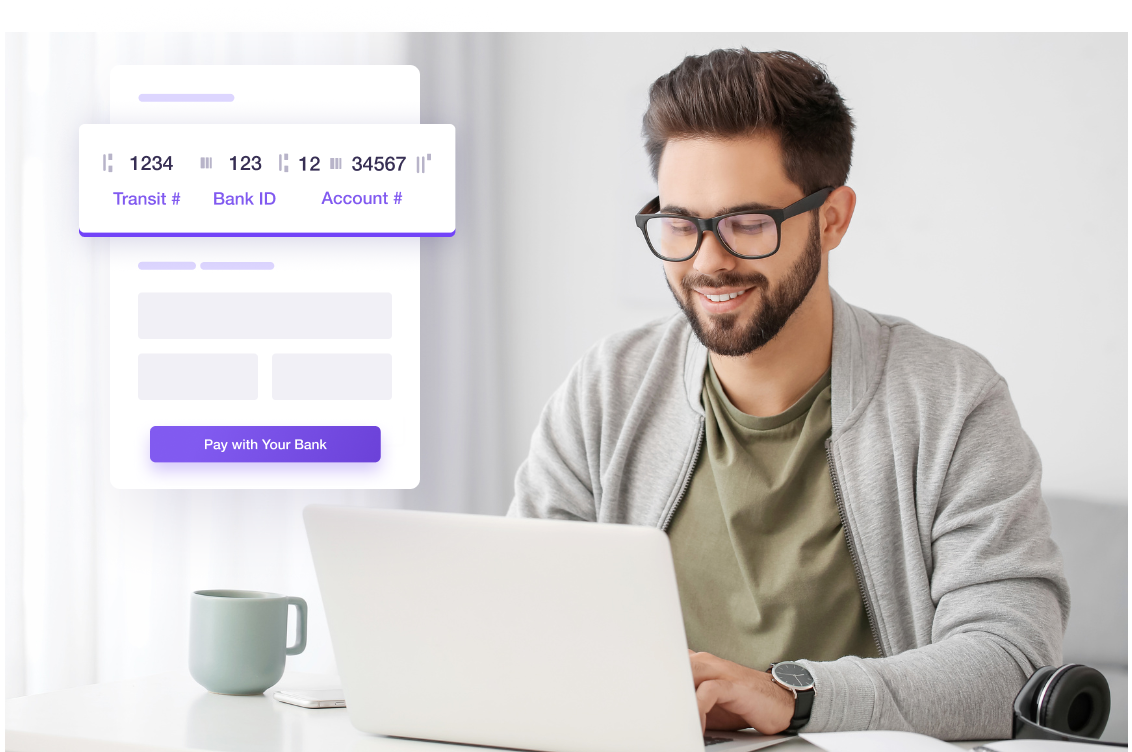

Once you've picked an ACH payments provider, you'll need to set up a merchant account. This account will allow you to start and receive ACH transactions from your customers. Be sure to go over the terms and conditions, pricing, and funding times to avoid any surprises later. It's also best

Collect the essentials: What you need from your customers

After setting up your merchant account, you’ll now need to gather some information from your customers which you can include in your customer intake process such as:

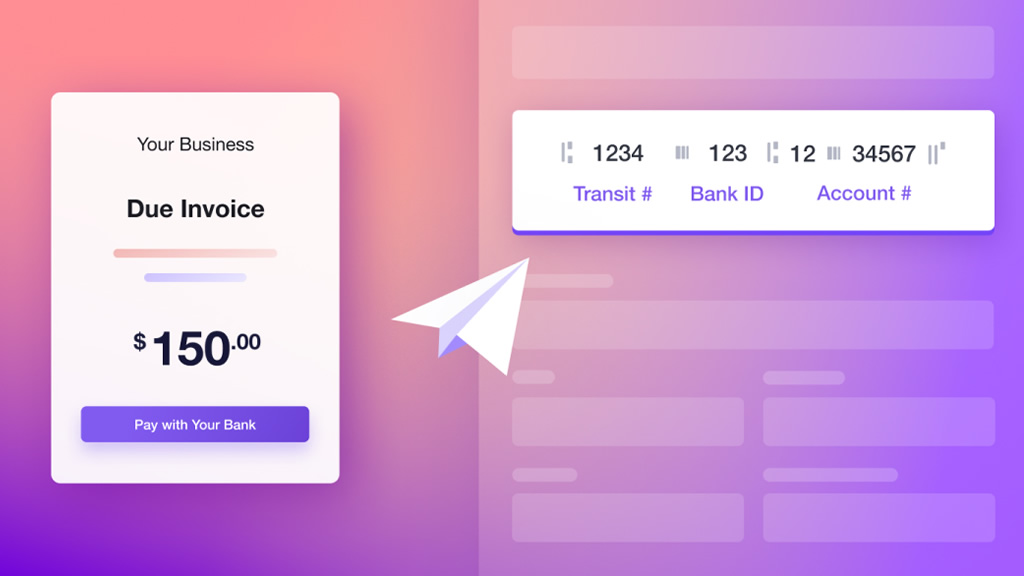

- Bank account details: Get their account and routing numbers.

- Authorization: Make sure your customers authorize the transactions you’ll run. This can be done through a Pre-authorized Debit (PAD) agreement, which they can sign physically, electronically, or even recorded verbally. While you can make your own authorization form, we made it easier for you with a ready-to-print template along with other materials in our guide below.

Kick back, get paid, save on costs

Once you’ve got the authorization, you can submit the ACH payment request using your provider’s platform and save on processing fees versus card payments. Providers like Helcim offer ACH payments in various tools, including invoicing, virtual terminals, recurring payments, and payment links.

Wrapping it up

ACH payments may have seemed mysterious before, but now you’re equipped with everything you need to take full advantage of this cost-effective, secure, and convenient payment method.

Ready to start accepting ACH payments for your business? Sign up with Helcim today—no monthly fees, no contracts, just affordable ACH payments and more at your fingertips.

Frequently asked questions (FAQ)

Q: Which banks support ACH transfers?

A: Most banks in the U.S. and Canada support ACH transfers, as it's a standard method for electronic payments. However, it’s always a good idea to double-check with your customer’s bank to ensure everything’s in place.

Q: What’s the maximum amount you can accept through ACH?

A: The maximum amount you can accept through ACH depends on your payment provider and bank’s policies. Some may have limits, while others offer higher caps for business accounts. NACHA recently raised the same-day ACH transaction limit from $100,000 to $1 million, offering more flexibility for larger payments. It’s best to check with your payment provider for specific limits.

Q: What happens if an ACH payment goes to the wrong account?

A: If this happens, you can process a reversal through your payment provider or bank. It’s important to act quickly since reversals typically need to be initiated within 24 hours or a specific timeframe to avoid fees.

Q: Can you send ACH payments to a Canadian bank?

A: ACH payments are mainly used in the U.S., but Canada uses a similar system called EFT (Electronic Funds Transfer). While you can’t send ACH payments directly to Canadian banks, some providers offer cross-border payment solutions.

Q: Can an ACH payment be declined?

A: Yes, ACH payments can be declined for reasons like insufficient funds, incorrect account information, or a closed account. Your payment provider will notify you if a payment is declined.

Q: Can a bank reverse an ACH payment?

A: Yes, ACH payments can be reversed if there’s an error or if the transaction is unauthorized. However, reversals need to be requested within a certain period to avoid costs and chargebacks.

Q: Can ACH payments be traced?

A: Yes, ACH payments are traceable. Your payment provider can track the status of a transaction using a trace number, so you can confirm whether the payment went through successfully or if there were any issues.