You know that feeling when you check your bank statement, and something just… isn't right? Like a charge for a gym membership you never signed up for, or a donation to a charity you've never heard of? It's not a credit card charge you can easily dispute. Instead, it's an ACH payment, quietly pulled directly from your bank account. A knot forms in your stomach as you realize someone has found a way to dip into your bank account, without your permission, using the same system many businesses use to pay bills or employees. Scary, right? This isn't some far-fetched movie plot; it's a real-life headache many businesses and individuals face.

The good news is, you're not powerless. Fraudulent ACH transactions might sound intimidating, but there are clear steps you can take to protect your money. In this article, we'll pull back the curtain on how ACH payments work, expose the common ways fraudsters try to trick you, and most importantly, give you 10 practical tips to safeguard your business and your bank account from these sneaky scams.

What is the benefit to ACH payments?

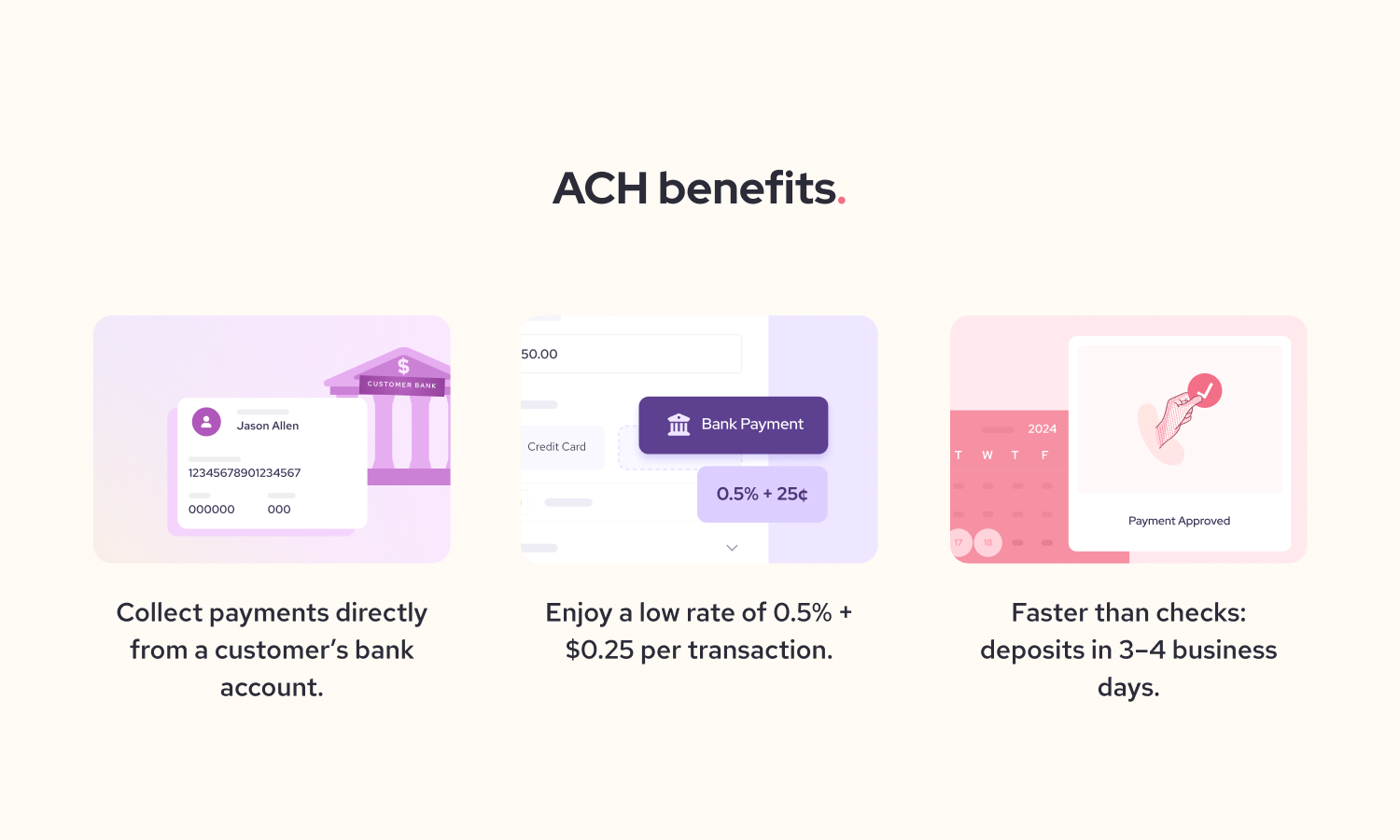

ACH payments offer a simple and cost-effective way to move money directly between bank accounts. Think of them as the backbone for many common financial tasks, like getting paid every two weeks or setting up automatic bill payments. This method is often much cheaper for businesses than processing credit card payments, which usually come with higher processing fees.

Many businesses choose ACH because it helps them save money on transaction costs. For example, a credit card transaction might cost a business 2% or more of the sale amount, plus a small fee. An ACH payment, on the other hand, often has a flat fee that's much lower, sometimes just a few cents or a fixed small amount per transaction. When you're dealing with hundreds or thousands of transactions, those savings really add up. That's why the ACH Network securely handled 31.5 billion payments in the US in 2023, showing just how widely businesses and consumers rely on it for its efficiency and lower costs."

What is the risk of paying with ACH?

While ACH payments offer great benefits, the main risk comes from their direct connection to your bank account: unauthorized access can lead to significant financial loss. Unlike credit cards, which offer strong consumer protections and chargeback options, getting your money back from an unauthorized ACH debit can be a much harder and slower process.

Think about it this way: when someone gets your credit card number, they might spend up to your credit limit, and banks are usually quick to reverse fraudulent charges. But if a fraudster gets your bank account and routing number, they could potentially drain your checking or savings account. Recovering those funds often involves your bank investigating, which can take days or even weeks. During that time, your business might face cash flow problems because the money is gone. This is why vigilance is key when dealing with anything connected to your bank account details.

How does ACH fraud work?

ACH fraud typically involves a scammer getting your bank account information and then using it to make unauthorized payments or withdrawals. It usually follows a few key steps:

- Getting your information: Fraudsters first need your bank account and routing numbers.

- Creating fake transactions: They then use this information to set up unauthorized debits or credits.

- Processing the payment: The unauthorized payment goes through the ACH network.

- Money vanishes: Your bank account is debited, and the money is gone.

1. Getting your information

The first step for any fraudster is getting their hands on your sensitive banking details. They might do this in a few ways. Sometimes, they trick you into giving it to them through phishing emails that look like they're from a legitimate company or your bank. These emails often ask you to "verify" your account details by clicking a link that takes you to a fake website. Other times, they might steal paper checks, as your account and routing numbers are printed right there. They could also hack into business systems where this information is stored.

2. Creating fake transactions

Once they have your bank account and routing numbers, fraudsters will create fake payment requests. They might set up a recurring debit payment for a service you never subscribed to, or they could initiate a one-time withdrawal pretending to be a vendor you regularly pay. The goal is to make it seem like a legitimate transaction so it flies under the radar.

3. Processing the payment

These fake transactions are then submitted to the ACH network, just like real payments. The ACH network is a powerful system that processes billions of transactions. Because the fraudster has your actual bank account and routing number, the system processes it like any other payment. It doesn't instantly check if the person initiating the payment is truly authorized – that relies on other security measures and later reconciliation.

4. Money vanishes

Finally, your bank account is debited for the unauthorized amount. This means the money is removed from your account and sent to the fraudster's account. Often, victims only discover the ach payment fraud when they review their bank statements, sometimes days or even weeks after the money has already been taken. This delay makes it harder to recover the funds quickly, leading to potential financial strain for your business.

Who is at risk for ACH fraud?

Anyone who uses ACH payments, whether as an individual or a business, is at risk for ACH fraud. However, small businesses are often particularly vulnerable because they might not have the same robust security systems or dedicated fraud prevention teams as larger corporations.

Here's a closer look at who is typically in the crosshairs for these types of scams:

- Individuals: If you pay bills automatically, receive direct deposits, or send money through apps, your personal banking details could be targeted.

- Small businesses: Without strong internal controls, small businesses are attractive targets for fraudsters.

- Companies with weak security: Any organization that doesn't prioritize cybersecurity measures is at higher risk.

- Businesses that frequently use ACH: The more you use ACH for payroll or vendor payments, the more opportunities there are for unauthorized transactions.

1. Individuals

If you've ever set up an automatic payment for your utility bill, received your paycheck via direct deposit, or used a payment app like PayPal or Venmo that links to your bank account, you're using ACH. This means your personal bank account and routing numbers are out there. Fraudsters can try to intercept this information or trick you into revealing it, then use it to pull money from your account. While financial institutions offer some protection, recovering funds from a personal ACH fraud can still be a frustrating and time-consuming process.

2. Small businesses

Small businesses are often seen as easier targets for fraudulent transactions compared to larger companies. Why? They might not have complex fraud detection software, dedicated IT security staff, or the strict payment verification processes that big corporations do. This means a single employee can sometimes be tricked into making a fraudulent payment, or a security lapse could expose sensitive banking data. For instance, if a small business owner uses the same computer for both personal and business banking, and that computer gets infected with malware, both sets of accounts could be at risk.

3. Companies with weak security

Any business, regardless of size, that doesn't make cybersecurity a top priority is putting itself at risk. This includes not having strong passwords, not using two-factor authentication (where you need a code from your phone in addition to a password), or not regularly updating software. Outdated systems can have security holes that fraudsters can exploit to get their hands on your banking information or infiltrate your network. It's like leaving your business's back door unlocked – it just makes it easier for criminals to walk right in.

4. Businesses that frequently use ACH

The more often your business uses ACH for things like payroll, vendor payments, or collecting customer invoices, the more exposure your banking details have. Every transaction, every new vendor setup, and every employee receiving a direct deposit creates a potential point of vulnerability. This doesn't mean you should stop using ACH – it's too beneficial! – but it does mean that businesses with high ACH transaction volumes need to be extra vigilant and have robust internal controls in place to prevent fraud.

What are common examples of ACH frauds?

Now that we know who is at risk, let's review a few common ways ACH fraud can happen so you are better equipped to spot fraudulent activity before it occurs.

- Unauthorized debits: This is when a fraudster simply pulls money from your account without your permission.

- Phishing scams: These scams try to trick you into giving away your bank information or other sensitive details.

- Business Email Compromise (BEC): This scam tricks your employees into sending payments to the wrong bank account.

- Vendor Impersonation: Fraudsters pretend to be a supplier and trick you into updating payment details.

- Account takeover: Criminals gain full access to your online banking.

1. Unauthorized debits

This is perhaps the most straightforward type. A fraudster simply uses your bank account and routing number to pull money directly from your account without your permission.

How it shows up at a small business: Imagine a small marketing agency. A fraudster might get their bank details from a carelessly discarded invoice or even a data breach. The fraudster then sets up a recurring "subscription fee" for a fake software service, pulling hundreds of dollars from the agency's operating account every month. The agency might not notice until they do their monthly reconciliation, by which time several payments could have already gone through.

2. Phishing scams

These scams try to trick you into giving away your bank information or other sensitive details. They usually come in the form of fake emails or texts that look legitimate.

How it shows up at a small business: You might get an email that looks exactly like it's from your utility company, saying your latest bill couldn't be processed and asking you to "update your payment information" by clicking a link. If you click and enter your bank details on their fake website, the fraudsters now have what they need to initiate unauthorized ACH debits.

3. Business Email Compromise (BEC) fraud

This is a sophisticated scam where fraudsters pretend to be someone you know and trust, often a vendor or even your CEO, to trick you into making an unauthorized payment.

How it shows up at a small business: A fraudster hacks into a supplier's email account (or creates a very convincing fake one). They then send an email to your small business's accounts payable department, pretending to be that supplier, announcing "new bank details" for future payments. If your bookkeeper updates the bank details and sends the next invoice payment via ACH to the fraudster's account, that money is as good as gone. This scam relies on urgency and trust, making it particularly dangerous for businesses.

4. Check fraud

Even in our digital age, physical checks can be a weak link. Your account and routing numbers are printed right there.

How it shows up at a small business: If a fraudster steals one of your business checks from the mail or even dumpster dives, they have all the information needed to create fraudulent ACH payments. They don't even need to forge the check; they can use the numbers to set up an electronic withdrawal that looks legitimate to the ACH system.

Top 10 ACH fraud prevention tips

Protecting your business from ACH fraud might seem like a daunting task, but it doesn't have to be. By putting a few smart practices in place, you can significantly reduce your risk and keep your money safe. Think of these as your business's shield against sneaky fraudsters.

Here are our top 10 tips to help you prevent ACH fraud:

- Monitor your bank accounts daily.

- Implement strong internal controls.

- Use positive pay or ACH blocks.

- Educate your employees.

- Secure your computer systems.

- Protect your banking credentials.

- Verify all payment changes.

- Limit who has access to banking info.

- Reconcile bank statements regularly.

- Consider ACH velocity limits.

1. Monitor your bank accounts daily

Checking your bank accounts every single day is one of the easiest and most effective ways to spot fraud early. Fraudsters often start with small, unauthorized transactions to test the waters. If you catch these quickly, you can shut them down before they escalate to larger withdrawals. For example, if you see a $5 or $10 debit you don't recognize, reporting it immediately allows your bank to investigate and stop further attempts, potentially saving you thousands. Businesses that don't check their accounts often might only discover fraud weeks later, by which point the money is often much harder to recover.

2. Implement strong internal controls

Internal controls are like your business's rulebook for handling money. They ensure that no single person can authorize and execute a payment without another person reviewing it. For instance, you could require two signatures for any ACH payment over a certain amount, or have one employee prepare payments and another approve them. This two-person rule significantly reduces the chance of an employee being tricked by a scam or even committing fraud themselves, as there's always a second pair of eyes on every transaction. Without these controls, a single phishing email could lead to a massive unauthorized payment if only one person has the power to act on it.

3. Use positive pay or ACH blocks

Many banks offer services specifically designed to prevent unauthorized ACH transactions. ACH positive pay lets you tell your bank exactly which companies you authorize to debit your account, and for what amounts. If an unauthorized debit tries to come through, the bank flags it.

An ACH block is even simpler: you can block all ACH debits from your account, or block them from specific companies you don't want debited. For small businesses that rarely receive ACH debits, an outright block can be a simple, powerful defense. Using these services means your bank acts as an extra layer of defense, stopping suspicious activity before it hits your account.

4. Educate your employees

Your employees are often the first line of defense, but they can also be the weakest link if they're not aware of common scams. Regular training on how to spot phishing emails, recognizing suspicious invoices, and understanding the risks of ACH fraud is crucial. For example, if your team knows to always double-check an email address before clicking a link or sending sensitive information, they're much less likely to fall for a Business Email Compromise (BEC) scam. Educated employees are like human firewalls, helping to protect your business from the inside out. To make this training consistent and measurable, many businesses partner with security awareness training vendors that offer AI-powered phishing simulations and interactive modules tailored to real-world threats like BEC and payment fraud.

5. Secure your computer systems

Fraudsters often try to get into your systems to steal banking information. Keeping your computers and networks secure is vital. This means using strong antivirus software, keeping all your software updated (especially your operating system and web browser), and using firewalls. Regular updates fix security weaknesses that hackers might try to exploit. Think of it like regularly locking your doors and windows; it makes it much harder for thieves to break in and access your sensitive data, including bank account details.

6. Protect your banking credentials

Your online banking username and password are the keys to your business's vault. Never share them, and always use strong, unique passwords that are hard to guess. Even better, enable multi-factor authentication (MFA), also known as two-factor authentication (2FA). This requires a second piece of information, like a code sent to your phone, in addition to your password. This means even if a fraudster somehow gets your password, they can't log in without that second code, making it significantly harder for them to gain unauthorized access to your accounts.

7. Verify all payment changes

If you receive an email or call asking you to change a vendor's bank account details for future payments, always verify it independently. Don't just reply to the email or use the phone number provided in the request. Instead, call the vendor using a trusted phone number you already have on file (like from a previous invoice or their official website). Fraudsters are very good at mimicking legitimate requests, so a quick, independent call can save you from sending a payment to a scammer instead of your actual supplier. This simple step can prevent costly vendor impersonation fraud.

8. Limit who has access to banking info

Not everyone in your business needs to have access to your full bank account and routing numbers. The fewer people who have access, the smaller the risk of that information being compromised. Only grant access to employees who absolutely need it for their job responsibilities, and ensure those employees understand the importance of keeping that information confidential. Just as you wouldn't give every employee a key to your safe, you shouldn't give everyone access to your banking information.

9. Reconcile bank statements regularly

Don't just glance at your bank statement; carefully compare every transaction on your statement with your own records. This reconciliation process helps you spot any unauthorized debits or credits that might have slipped through. Many businesses reconcile monthly, but for better fraud detection, consider doing it weekly, especially if you have a high volume of transactions. The faster you spot a discrepancy, the faster you can report it to your bank and increase your chances of recovering lost funds.

10. Consider ACH velocity limits

Some banks allow you to set "velocity limits" on your ACH transactions. This means you can put a cap on the total dollar amount or the number of ACH debits that can occur from your account within a certain timeframe (e.g., no more than $10,000 in ACH debits per day, or no more than 5 ACH debits per week). If a fraudster tries to exceed these limits, the transaction will be blocked. This provides an automated safety net, catching large or numerous unauthorized transactions that might otherwise go unnoticed until it's too late.

Conclusion

We've covered a lot, from understanding how sneaky ACH fraud works to putting practical defenses in place. The bottom line is this: ACH payments are incredibly useful and cost-effective for businesses, but like any financial tool, they come with risks. By staying vigilant, educating your team, and implementing smart security practices, you can significantly reduce your vulnerability. It's about being proactive, not reactive, to protect your hard-earned money.

FAQs

What does ACH stand for?

ACH stands for Automated Clearing House. It's an electronic network that processes high volumes of credit and debit transactions in batches. Essentially, it's the secure system used for many direct deposits (like paychecks), automatic bill payments, and business-to-business money transfers across North America.

How do I stop an unauthorized ACH withdrawal?

Act immediately.

- Contact your bank right away: Call your bank's fraud department as soon as you spot the suspicious ACH debit.

- Submit a formal dispute: Your bank will require a written dispute form. For business accounts, the timeframe to report unauthorized debits is often very short (sometimes 24-48 hours), making quick action critical.

- Consider a stop payment order: If it's a recurring unauthorized debit, you can often issue a stop payment order to your bank for future payments from that specific source.

Can you trace an ACH transaction?

Yes, absolutely. Every ACH transaction has a unique 15-digit trace number. Think of it like a tracking number for a package. You or your bank can use this number to follow the payment's journey through the ACH network, which helps if a payment is delayed, missing, or needs investigation. You can usually find this number in your online banking transaction details.

Can you reverse an ACH transfer?

Reversing an ACH transfer is possible, but it's much harder and more restricted than a credit card reversal.

- For an unauthorized ACH debit (money pulled from your account), you can dispute it with your bank for potential reversal.

- For an ACH credit (money sent by you), reversals are only allowed under very specific circumstances, like a duplicate payment, incorrect amount, wrong account, or wrong date. Your bank can request a reversal, usually within a few banking days, but it's not guaranteed, especially if the funds have already been accessed by the recipient. Always double-check payment details before sending an ACH credit.