Credit card processing fees can feel like a hidden tax on your business. Every time a customer swipes, taps, or enters their card online, a portion of that sale goes to credit card industry companies.

For small businesses, these fees can add up fast. But why are credit card processing fees so expensive today? What’s driving these costs up? And is there anything businesses can do about it? Let’s break it down.

Who gets the money from credit card fees?

Every time a customer pays with a credit card, the business doesn’t get the full amount. A portion of the sale goes to banks, credit card networks, and payment processors.

- Card-issuing bank (your customer banks): They collect interchange fees because they take the risk of lending out money and help transfer money through the credit card network. The interchange fees vary by card type, transaction method, and industry.

- The credit card networks: The networks like Visa, Mastercard, Amex, and Discover collect assessment fees (card brand fees) to help cover network operations and fraud protection.

- Your credit card processor: They help process credit card transactions, so they add a small markup on top of each transaction.

Why are credit card processing fees so high?

If you feel like credit card processing fees keep getting more expensive, you’re not imagining things. Businesses across industries have seen their costs rise, cutting into profits and making it harder to keep prices competitive.

But why are these fees going up? It’s not just one factor—it’s a mix of:

- Rising interchange fees

- More premium and rewards credit cards are used by the customers

- Increase in online and card-not-present transactions

- Lack of transparency from some payment processors

Let’s break down the biggest reasons why businesses are paying more today.

1. Rising interchange fees

Interchange fees make up the largest portion of credit card processing costs. When card networks raise interchange fees, processors have no choice but to pass those costs on to businesses.

The chart below shows how interchange fees have changed over time, based on Helcim data from May 2021 to March 2025. These are average numbers factors in the official changes in interchange fees by card brands, different types of cards (consumer, corporate, and premium), and industries.

For online transactions:

- American Express (AEXP) saw a 1% increase in average credit card interchange fees.

- Visa (VISA) fees went up by 3%.

- Mastercard (M/C) was the only major network to lower its interchange fees, decreasing by 7% over the same period.

For in-person transactions:

- American Express (AEXP) saw a 3% decrease in credit card interchange fees.

- Mastercard (M/C)’s fees increased 7%.

- Visa (VISA) fees decreased by 3%.

2. More premium and rewards credit cards are used by the customers

Consumers love rewards—cashback, travel points, and exclusive perks, but someone needs to pay for these rewards.

Every time a customer pays with a premium rewards card, the interchange fee is higher. That’s because the banks and credit card networks funding these rewards need to make up for the perks they offer. They then pass it on to businesses in the form of higher interchange fees.

Why do rewards credit cards cost more to accept?

- Bigger perks mean higher fees

- Customers who use premium credit cards increase the average processing cost for businesses.

- Customers' banks promote these cards heavily because they generate more revenue through fees and interest.

According to Helcim data, consumer credit card usage (low-fee credit card type) has dropped by 18% from May 2021 to February 2025. In its place, businesses are seeing more transactions from corporate, premium, and other high-cost credit cards—which come with significantly higher processing fees.

When analyzing interchange fee trends by card type, consumer credit cards have 50% less fees than premium and corporate cards. This means that as more customers switch to higher-cost credit cards, merchants are forced to pay more in processing fees—even if their total sales stay the same.

3. Increase in online and card-not-present transactions

More customers are shopping online, paying invoices remotely, and using digital wallets. While this shift offers convenience, it also drives up credit card processing fees. According to Helcim data, in March 2025, the online interchange fees are 45% higher than the in-person ones.

Why do online and card-not-present transactions cost more?

- Higher fraud risk: Without a physical card being inserted, it’s harder for the bank to verify that the transactions are made by card owners. Because of higher risks, banks and card networks charge higher interchange fees for these transactions.

- Stronger security requirements: Online transactions require additional fraud protection measures like tokenization, 3D Secure, and PCI compliance, adding extra costs for processors—and ultimately for businesses. For businesses handling remote payments or sensitive customer data, using a secure vpn can also help reduce exposure to cyber threats that contribute to higher fraud risk and processing costs.

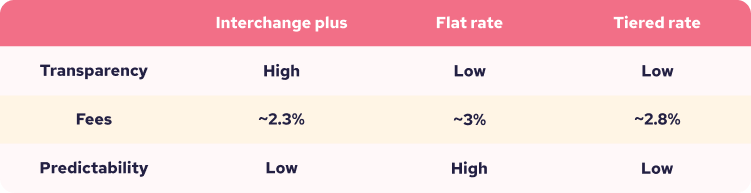

4. Lack of transparency from some payment processors

Not all payment processors are upfront about their fees. Many businesses sign up for processing services without realizing they’re paying much higher credit card fees than the true costs.

How do credit card processors charge high costs without transparency?

- Tiered pricing structures: Some processors group transactions into different rate tiers (qualified, mid-qualified, non-qualified). The qualified tier has the lowest credit card fees, but the merchants could never know what transaction is qualified, and what is not.

- Flat-rate processing fees: Many big processors like Square, Stripe, Clover, and Moneris charge a flat rate (e.g., 2.75% to 3.5% per transaction). While it looks simple, the actual credit card fees for many transactions are often much lower. This means processors profit more on every sale while merchants unknowingly overpay.

Instead of charging a flat-rate markup, Helcim uses interchange-plus (cost-plus) pricing, which passes the true cost of each transaction to merchants, with a transparent, fixed markup. On average, Helcim merchants save 25% compared to traditional pricing models.

Helcim credit card fees compared to other processors in Canadia

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.39% (avg) + $0.25 | 1.76% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% + $0.30 to 3.3% + $0.15 | 2.5% |

| Stripe (flat-rate) | 2.90% + $0.30 + 0.5% for manually entered cards + 0.8% for international cards + 2% if currency conversion is required | 2.7% + $0.05 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Helcim credit card fees compared to other processors in the U.S.:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.49% (avg) + $0.25 | 1.93% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% to 3.30% + $0.30 | 2.60% + $0.15 |

| Stripe (flat-rate) | From 2.90% + $0.30 + 0.5% for manually entered cards + 1.5% for international cards + 1% if currency conversion is required | 2.70% + $0.50 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Why do high-risk industries pay higher credit card processing fees?

Businesses in high-risk industries face higher credit card fees because they are more likely to have fraud, chargebacks, and financial instability.

Examples of high-risk industries:

- Adult Content and Services

- Unregistered charities

- Firearms, weapons, explosives and dangerous materials

- Gambling

- Tobacco

- Multi-level marketing

Many mainstream payment processors refuse to work with high-risk businesses due to the financial and legal risks. Those that do accept them charge significantly higher fees to offset potential losses. This often includes higher per-transaction fees, rolling reserves, and stricter contract terms. For age-restricted businesses (e.g., tobacco), strong age verification software can help reduce compliance risk and chargeback or dispute exposure, and comparing providers can clarify what’s typically available.

How can businesses negotiate lower credit card rates?

Many businesses don’t realize that credit card processing fees aren’t fixed. If you process a high volume of transactions each month, you can contact the payment processor to negotiate lower rates and save a significant amount over time.

However, most payment processors require a contract with minimum volume commitments to maintain those lower rates. If your processing volume drops below the agreed threshold, you could face higher fees or lose your discounted rate.

With Helcim, there’s no need to negotiate. Helcim automatically lowers your credit card processing fees as your transaction volume increases—saving you both time and money, without the hassle of contracts or negotiations.

What are the best credit card alternatives to reduce processing fees?

Businesses don’t have to rely solely on credit card payments. By offering alternative payment methods, you can reduce fees and keep more of your revenue. Here are the best alternative payment methods:

- ACH/EFT payments (Bank transfers): ACH payments (US) or EFT payments (Canada) can be 90% cheaper than credit card transactions. For example, Helcim charges 0.5% + 25¢ per transaction. The fees are capped at $6 for transactions below $25,000. The ACH/EFT payments are affordable for recurring billing or high-ticket purchases.

- Debit card payments: Debit card interchange fees are typically lower than credit card fees. For example, in the U.S., Visa Debit Card has the interchange rate from 0.05% to 1.7%. For Canada, Helcim charges 9¢ per debit transaction through Interact network.

- Cash: For in-person transactions, you can encourage cash payments by offering a discount. Collecting cash eliminates credit card fees entirely.

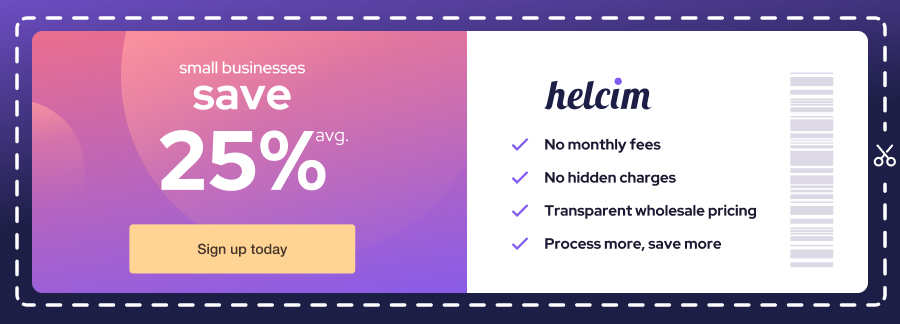

Save 25% on credit card fees with Helcim

Many businesses overpay without realizing it. Unlike traditional payment processors, Helcim offers interchange-plus pricing which offers the most transparent and lowest rates for credit cards.

- You only pay the true interchange cost plus a transparent markup.

- As your business grows and processes more payments, your rates automatically get lower.

- No monthly fees and long-term contracts

- Businesses save 25% on credit card fees compared to traditional processors.

Stuck with another provider? We’ll waive up to $500 in processing fees to help cover your contract cancellation costs and equipment fees when you switch to Helcim.

FAQ

How much do credit card companies make off each transaction?

Credit card brands (Visa, Mastercard, Amex, Discover) earn money through assessment fees. For example, Visa charges 0.24% + 2¢ per in-person transaction and 0.22% + 2¢ per online transaction.

How much do banks make on credit card transaction fees?

The customer’s bank (card issuer) collects interchange fees from merchants on every credit card transaction. These fees can be as high as 2.50%, depending on factors like the card brand (Visa, Mastercard, Amex), the industry, the card type (premium vs. standard), and whether the transaction is online or in person. Banks also earn revenue from annual fees, cash advances, and penalties for late or missed payments from cardholders.

Do credit card processing companies make money?

Yes, credit card processing companies make money by charging a markup on top of interchange fees set by card networks. For example, Helcim charges a 0.40% + 8¢ markup per transaction, while Square keeps 0.86% of processing fees as profit. Some processors also earn revenue from monthly fees, PCI compliance fees, and other service charges. Helcim merchants don’t pay monthly or hidden fees, making it a more transparent option.