A chargeback hits your business like a gut punch. One day you’ve made a sale, then tomorrow, the payment is reversed, and the money is pulled out of your account—sometimes without warning.

But here’s the thing: you don’t have to just accept it and move on. You can dispute the chargeback and fight back. And if you do it right, you can win.

What is a chargeback fraud?

Chargeback fraud happens when a customer disputes legitimate credit card transactions to get their money back, even though they received the product or service.

Chargebacks were designed to protect customers from fraud. Over time, some customers realize just how easy it is to get their money back through a chargeback—no matter the reason. That’s when things cross the line into what’s called chargeback fraud.

This type of abuse can quietly eat into your profits. A customer files a legitimate chargeback once and sees it work. Next time, they skip contacting you altogether and go straight to the bank—even if there’s nothing wrong with the transaction.

How does a merchant dispute credit card chargeback?

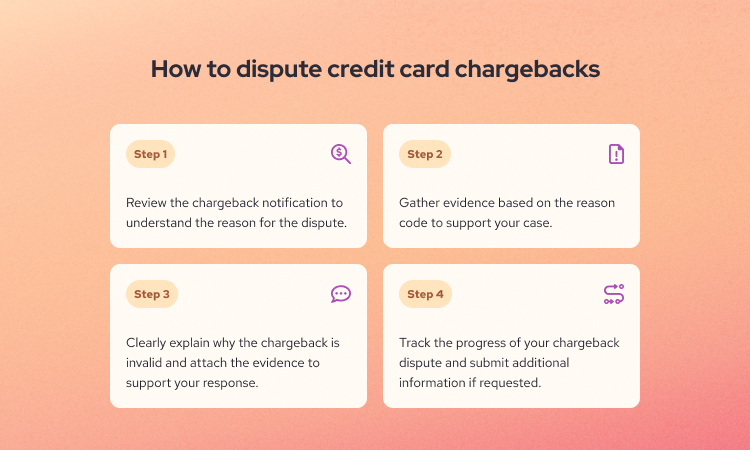

Getting hit with a chargeback can feel unfair. As the merchant, you have the right to dispute the chargeback and make your case. Here’s what the chargeback dispute process typically looks like:

- Step 1: Review the chargeback notification

- Step 2: Gather evidence to counter the chargeback process

- Step 3: Submit evidence to start the dispute process

- Step 4: Track your chargeback counter process

Every processor has different chargeback dispute process, below is how the process looks like for Helcim.

Let’s break down each step so you know exactly what to do.

Step 1: Review the chargeback notification

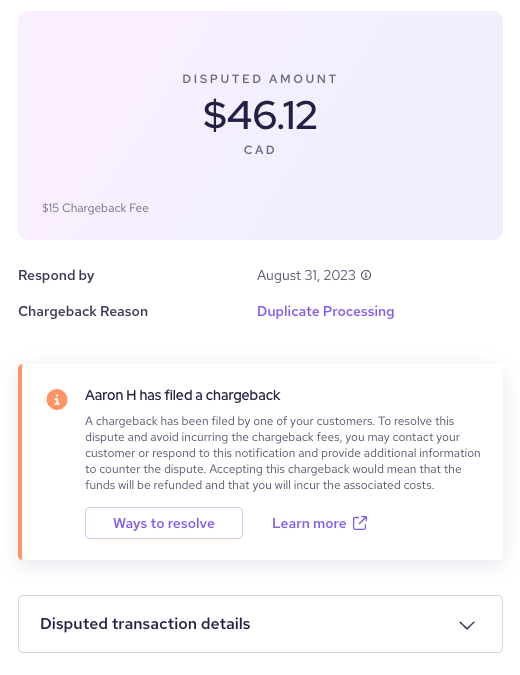

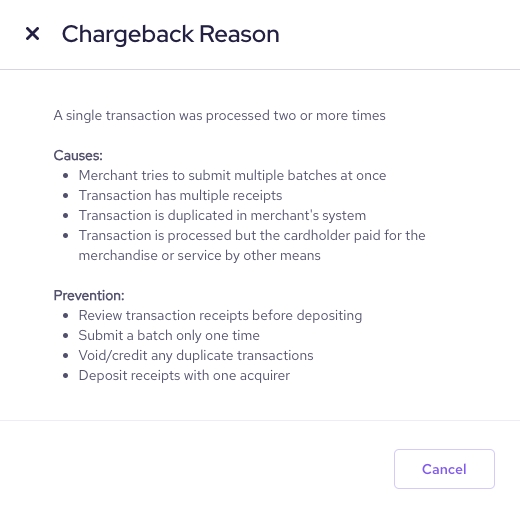

When a chargeback is filed, your payment processor will send you a chargeback notification via email or dashboard. This isn’t something you can ignore. The notification will also include key details like:

- The reasons of the chargeback

- The transaction date and amount

- The customer’s name

- Instructions for submitting your dispute

When a chargeback comes in, don’t hesitate to reach out to the customer politely and directly. Sometimes, chargebacks come from simple mix-ups—like a forgotten subscription or unclear billing.

Step 2: Gather evidence to counter the chargeback process

If you reach out to the customers and they drop the chargeback, make sure you gather proof that the customer canceled the dispute. An email or text thread is helpful, but the best-case scenario is a written statement from the customer confirming they’ve withdrawn the chargeback.

If you reach out to the customer and can’t resolve the issue—and you believe the transaction is valid—it’s time to decide whether to fight the chargeback. Start by reviewing the reason in the chargeback notification. It will tell you what the customer claimed and what kind of evidence you’ll need to respond.

Here’s the kind of evidence that helps build a strong case:

- Transaction history

- Receipt or invoice of disputed transactions

- Shipping and tracking details (with delivery confirmation)

- Signed proof of delivery or service completion

- Screenshots of product descriptions and return policies

- Emails or messages exchanged with the customer

- Evidence the customer used the product or service

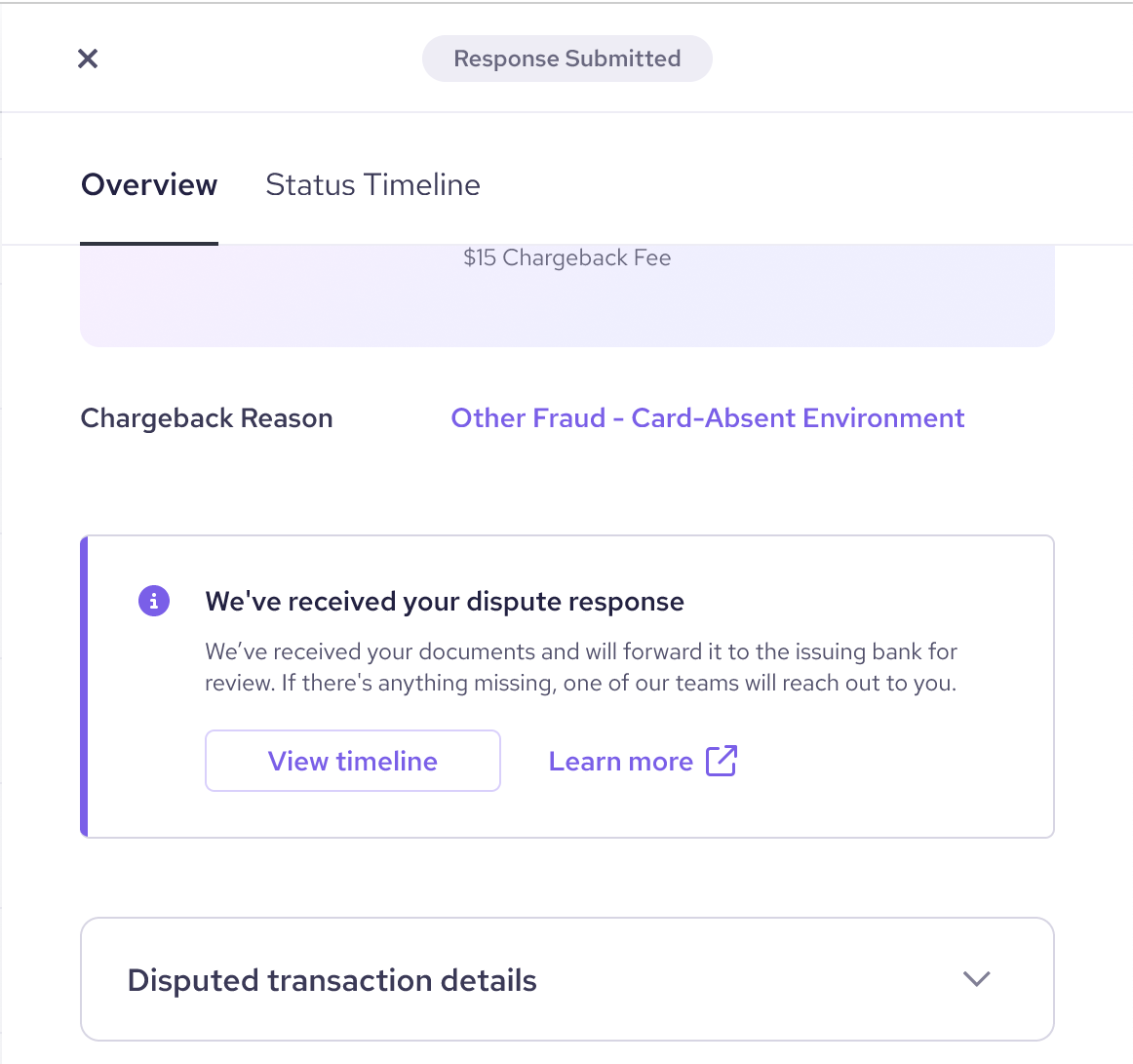

Step 3: Submit evidence to start the dispute process

Once you’ve gathered your documents, you can submit them through your merchant account dashboard. Start with a short summary explaining why you believe the chargeback is not valid. Walk through what happened, and point to the evidence you’re including.

Then, attach your supporting documents. Label each file clearly and, if possible, highlight key details—like delivery confirmation or matching customer info.

After you submit the evidence, you should see the success messages.

Step 4: Track your chargeback counter process

Once you’ve submitted your evidence, log into your payment processor’s dashboard regularly to check the status. Some processors will update you if the bank needs more information or if a decision has been made. If you’re Helcim’s merchant, you can view the chargeback dispute process timeline in the dashboard.

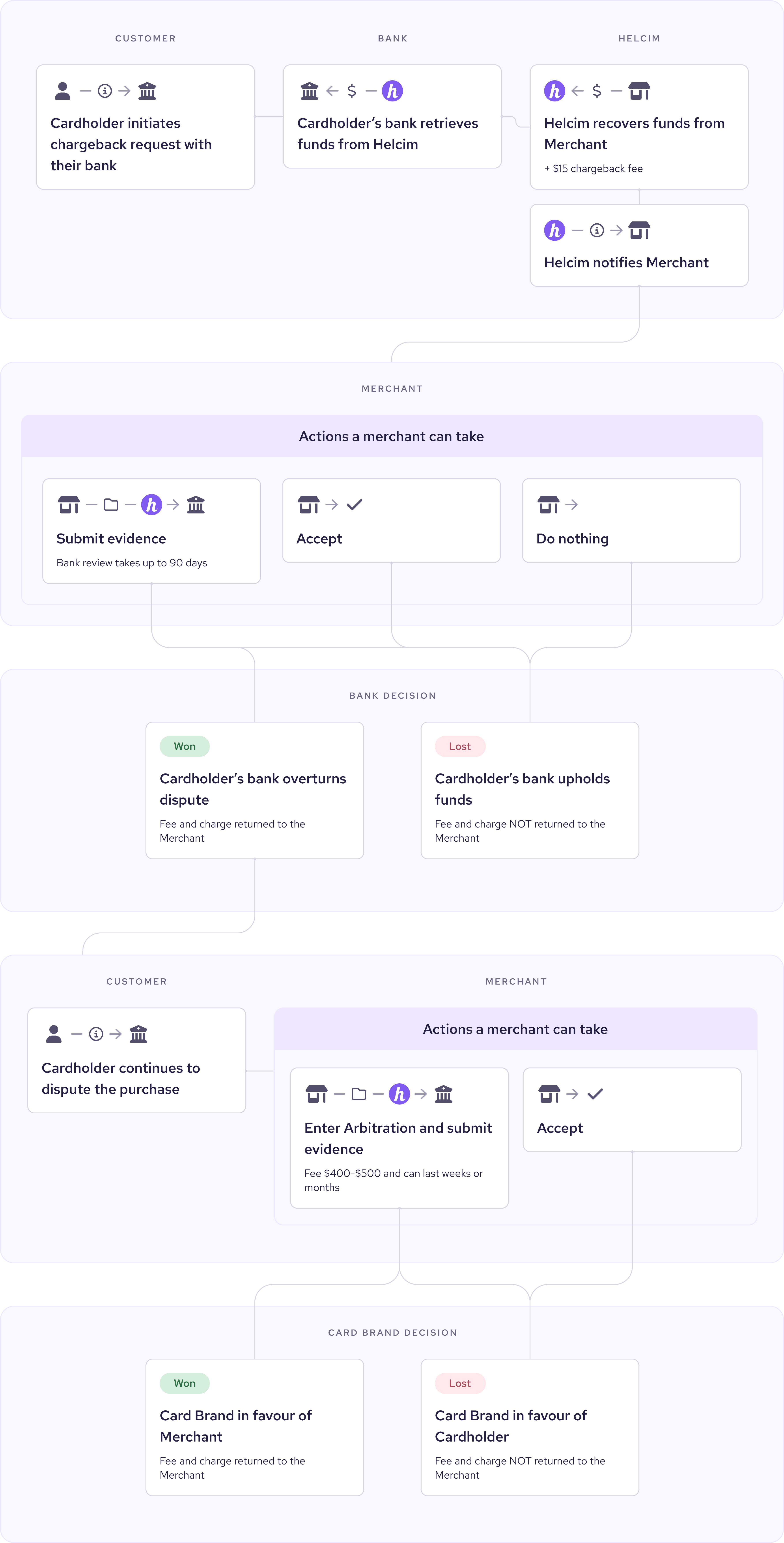

What happens after a merchant disputes a chargeback?

Once you’ve submitted your evidence, your payment processor will forward everything to the customer’s bank (card issuing bank) through the acquiring bank and card network. From there, the review begins.

- The card issuer investigates the disputed payment: They’ll look at both sides: the customer’s claim and your supporting documents. They’re trying to decide who has the stronger case based on the evidence provided.

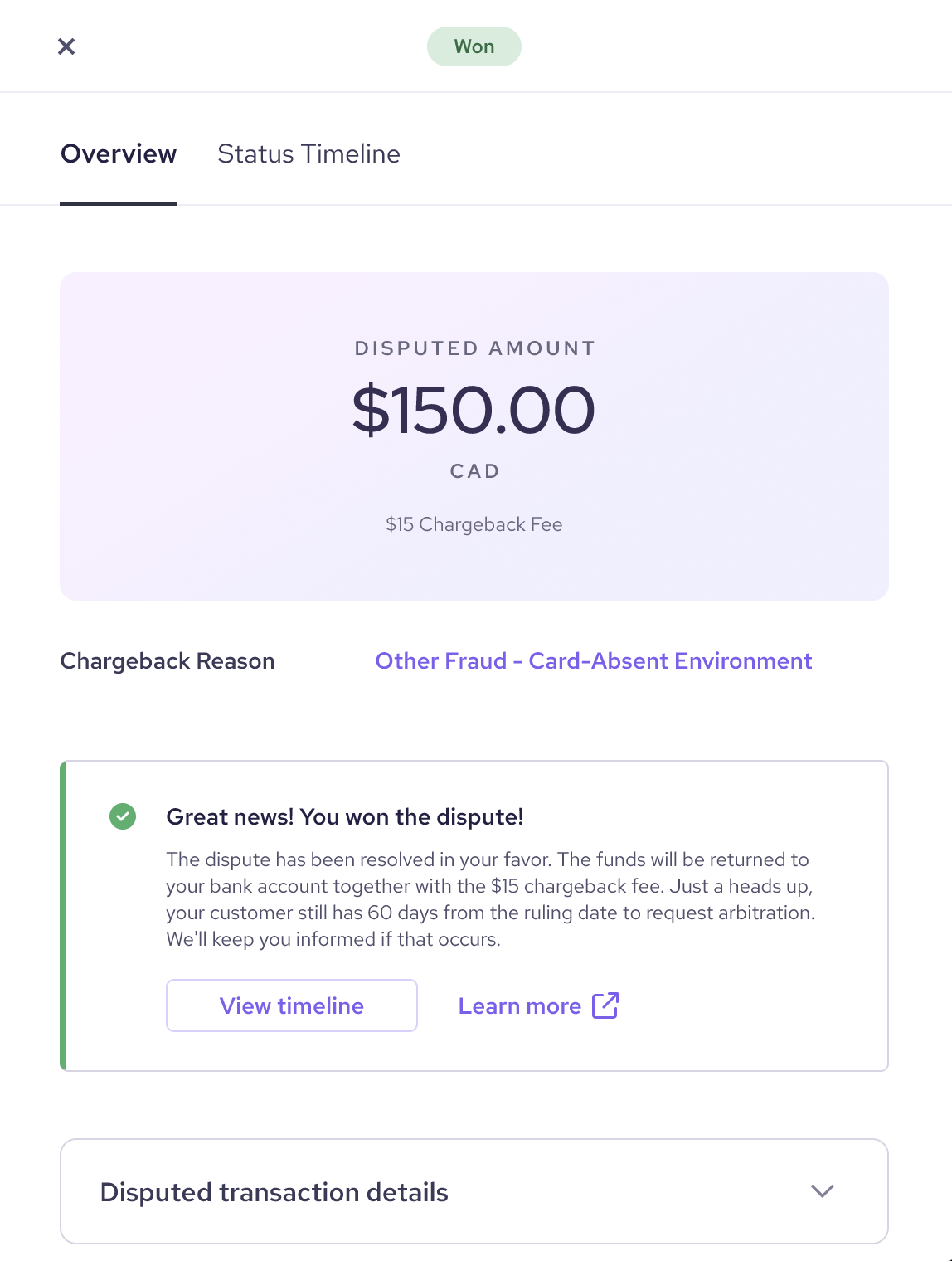

- A decision is made: If the bank sides with you, the chargeback is reversed and the funds are returned to your account. If they side with the customer, the chargeback stands—and you lose the money, along with the chargeback fees.

Will merchants get their money back if they win a chargeback dispute?

Some processors, like Helcim, return the merchant’s money and refund the chargeback fee ($15) if you dispute chargebacks and win. Others, like Stripe, keep the chargeback fee even if you win. That means you could do everything right, get your money back, and still end up paying just for defending yourself.

You’re charged a fee, from $15 to $35+, the moment a customer files a chargeback—whether it’s valid or not. This fee is meant to cover the administrative costs of handling the dispute, and it’s charged by your payment processor.

These fees can add up quickly—especially if you’re dealing with multiple chargebacks. That’s why it's so important to choose a processor with a merchant-friendly policies and to catch disputes early, before they turn into bigger losses.

What happens if a merchant wins a chargeback?

If you win a chargeback dispute, you get your money back. The card issuer will reverse the charge and return the funds to your account. But there are a few things to keep in mind:

The refund isn’t always instant: It can take days—or sometimes weeks—for the reversal to show up in your account.

You may not get the chargeback fee back: Some processors (like Helcim) refund the fee if you win. Others (like Stripe) keep it, no matter the outcome.

The chargeback still counts against your record: Even if you win, that chargeback still affects your chargeback ratio. If that number climbs too high (typically more than 1 chargeback per 100 transactions), your merchant account could be impacted negatively.

So yes, winning a chargeback means recovering the sale. But it doesn’t erase the cost entirely. That’s why preventing chargebacks matters.

What to do if you're getting too many chargebacks?

If chargebacks are piling up, here’s what you can do:

- Figure out what’s causing them: Look for patterns. Are customers confused about your billing name? Subscription billing frequency? Are certain products getting more complaints? Are most disputes related to delivery issues?

- Make your policies clear: Be upfront about your return, refund, and shipping policies—especially if there are delays, restrictions, or special conditions. Display them clearly on your website, order confirmation page, invoices, and emails. If customers know what to expect, they’re far less likely to file a chargeback.

- Improve communication: Reach out to customers quickly after a sale. Confirm orders, provide tracking info, and follow up if there’s a delay.

- Use fraud alert tools: Helcim’s fraud detection tool provides a risk assessment for each transaction, helping you spot potential fraud or chargeback risks before they happen.

Stopping chargebacks isn’t always possible—but reducing them is. A few small changes can go a long way in protecting your revenue and keeping your account in good standing.

FAQ

How can I prevent chargebacks in the first place?

Don’t ship the products if it looks suspicious (Helcim Defender can help you determine potential fraudulent transactions). Be clear with your product descriptions, billing terms, and return policies. Provide customer support and always confirm shipments with tracking info. The fewer surprises for your customers, the fewer chargebacks you'll face.

What evidence is most effective in disputing a chargeback?

The best evidence matches the reason for the chargeback. This could include receipts, shipping confirmation, proof of delivery, email conversations, or signed agreements. An email from the customer confirming receipt or satisfaction can be especially powerful.

How long do I have to respond to a chargeback notification?

Most processors give you between 7 to 14 days to respond, but the deadline can vary depending on the payment card network. It’s critical to act fast. Check the email or account dashboard’s notification to notice immediate chargebacks. Always aim to respond as early as possible.

Can merchants win chargebacks?

Yes, merchants can and do win chargebacks—especially when they provide strong, relevant evidence. Success often depends on how clearly you can show the transaction was legitimate. Clear documentation and timely response are key. While not guaranteed, a well-prepared case gives you a solid chance.