Credit card processing fees can be a challenge for businesses, especially when credit cards account for 32.6% of consumers' monthly payments in 2024, making them the most popular payment method.

As a business owner, understanding credit card processing fees is crucial to managing costs effectively. This article will help you break down what you’re paying for and how to reduce those fees.

What are credit card processing fee components?

Credit card processing fees are made up of two primary components: the interchange fees, and the processor margin.

1. Interchange Fees

The interchange fee is set by the card networks, such as Visa and Mastercard, and is paid to the cardholder’s issuing bank. The bank collects this fee for the risk and cost of processing the transaction. The interchange fee fluctuates on each transaction based on the type of card used (credit, debit, or rewards card), how the transaction is processed (in-person or online), and the industry you’re in.

2. Processor Margin

The credit card processing companies' margin is the fee charged by your credit card processor for handling the transaction and ensuring the funds are transferred securely. It’s essentially the processor’s profit. This fee can vary depending on your processor and the pricing model they use. Some processors charge a flat rate, while others use interchange-plus pricing, where you pay the actual interchange fee plus a fixed markup.

While some payment processors don’t provide a detailed breakdown of the rates they charge, Helcim’s pricing calculator offers full transparency. It breaks down the processing fees by card brand, card type, and whether the transaction is in-person or online, giving merchants a clear understanding of exactly what they’re paying for.

What makes the credit card processing fees high or low?

The amount you pay in credit card processing fees largely depends on the pricing model your payment processor uses. The two most common pricing models are flat-rate pricing and interchange-plus pricing.

1. Flat-Rate Pricing

Interchange fees fluctuate with every credit card transaction, making costs vary each time. To simplify things, many processors like Square, Stripe, or PayPal charge a fixed percentage for every transaction, regardless of the actual cost.

However, to ensure profitability, these processors often set higher fixed rates, meaning you overpay for most transactions. While flat-rate pricing offers predictability, it can be more expensive in the long run.

2. Interchange-Plus Pricing

Interchange-plus pricing is a more transparent and often more cost-effective model. With this structure, you pay the actual interchange fee, set by the card networks, plus a clear, fixed markup from the payment processor.

For example, Helcim charges Interchange + 0.40% + 8¢ per in-person transaction. While interchange fees may fluctuate based on the type of card or transaction, the processor's markup remains consistent. Despite the variable interchange fees, Helcim merchants typically save 25% on credit card processing fees on average compared to flat-rate processors like Square, PayPal, or Stripe.

How much are credit card processing fees?

The credit card processing fees are ranging from 1.7% - 3.5%, depending on the credit card processors.

Top processors with the lowest credit card processing fees for Canadian businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.39% (avg) + $0.25 | 1.76% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% + $0.30 to 3.3% + $0.15 | 2.5% |

| Stripe (flat-rate) | 2.90% + $0.30 + 0.5% for manually entered cards + 0.8% for international cards* + 2% if currency conversion is required | 2.7% + $0.05 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Top processors with the credit card processing fees for U.S. businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.49% (avg) + $0.25 | 1.93% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% to 3.30% + $0.30 | 2.60% + $0.15 |

| Stripe (flat-rate) | From 2.90% + $0.30 + 0.5% for manually entered cards + 1.5% for international cards + 1% if currency conversion is required | 2.70% + $0.50 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Helcim uses the interchange-plus pricing model, which passes the true cost of each transaction directly to the merchant. Want to know exactly how much you can save with Helcim, submit your merchant statement to get the saving estimate.

How to reduce credit card processing fees?

There are four tangible ways to reduce your credit card processing costs, one of which you can start doing today!

1. Use the interchange-plus pricing model

Unlike flat-rate pricing, which charges a fixed percentage on every transaction, interchange-plus passes you the actual fee of processing a credit card transaction. For example, Helcim’s interchange-plus pricing model saves merchants around 25% on fees compared to flat-rate processors like Square or PayPal.

Below are how much each industry save using interchange-plus pricing model compared to the flat-rate model:

| Industry Market | Total Savings (%) |

|---|---|

| Automotive | 28.31% |

| Cab & Delivery | 27.14% |

| Charity & Non-Profit | 31.04% |

| Contractors & Home Services | 26.37% |

| Education | 33.09% |

| Enterprise & Utilities | 48.45% |

| Financial Institution | 24.40% |

| Gas Stations | 40.54% |

| Government | 41.54% |

| Health, Beauty & Wellness | 31.62% |

| Healthcare | 25.09% |

| Hotels & Lodging | 23.36% |

| Online Sales | 20.66% |

| Organizations & Associations | 27.06% |

| Platforms, Apps & SaaS | 20.20% |

| Professional Services | 27.68% |

| Recreation | 27.01% |

| Restaurant | 31.49% |

| Retail Goods | 25.00% |

| Transportation | 20.36% |

| Wholesale | 23.23% |

2. Process more in-person transactions

While online payments are a convenient way to get paid when people can't visit your store (and bring your products to more customers), they are deemed higher risk by payment processing companies and card brands. Businesses often pay slightly more in payment processing fees for online payments than those processed when the customer pays in-person (known as a card-present transaction).

3. Get Helcim volume-based discounts fees

Some businesses qualify for preferred rates from payment processors due to their high transaction volume or large average transaction amounts compared to typical businesses. If your business processes a large number of transactions, it’s worth checking if your processor offers volume-based discounts.

With Helcim’s volume-based discount fees, the more you process, the more you save. Helcim automatically reduces your payment processing fees as your transaction volume grows, providing you with better rates—no need for negotiations or complex setups.

4. Ask about non-profit rates

If your business is a non-profit organization, you may be eligible for lower interchange costs and ultimately lower credit card processing fees. Many payment processors offer lower fees for nonprofits to support their missions, helping you keep more funds for your cause.

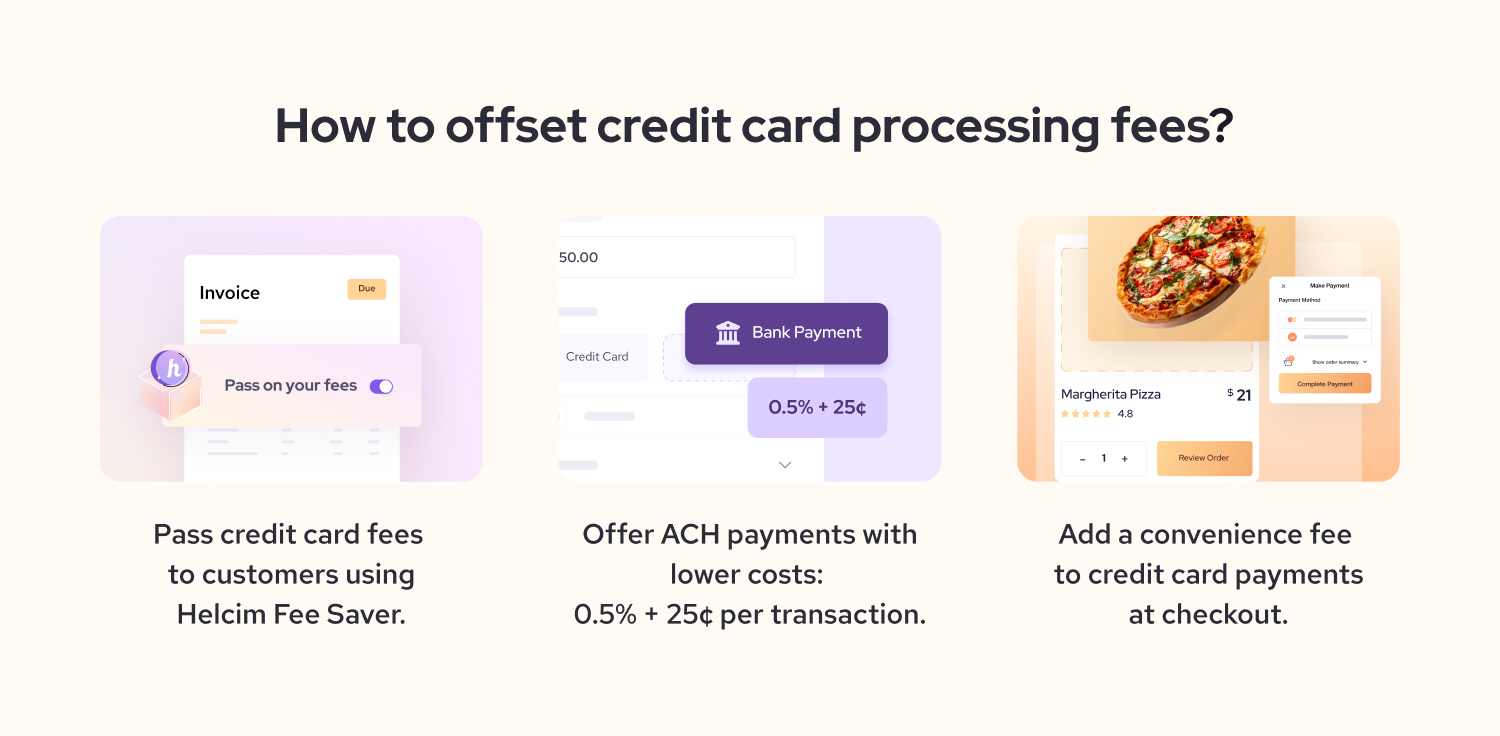

How to offset credit card processing fees?

Credit card processing fees can add up, but there are ways to offset or reduce these costs without sacrificing the convenience of accepting credit cards. Here are some strategies you can implement:

1. Implement surcharges

Through surcharging, the credit card processing fees are passed on to the customer when they choose credit card payment instead of lower-cost options like debit, ACH, check, or cash. With Helcim Fee Saver, you can set up surcharging with just one click, avoiding the hassle of complicated setups and confusing rules.

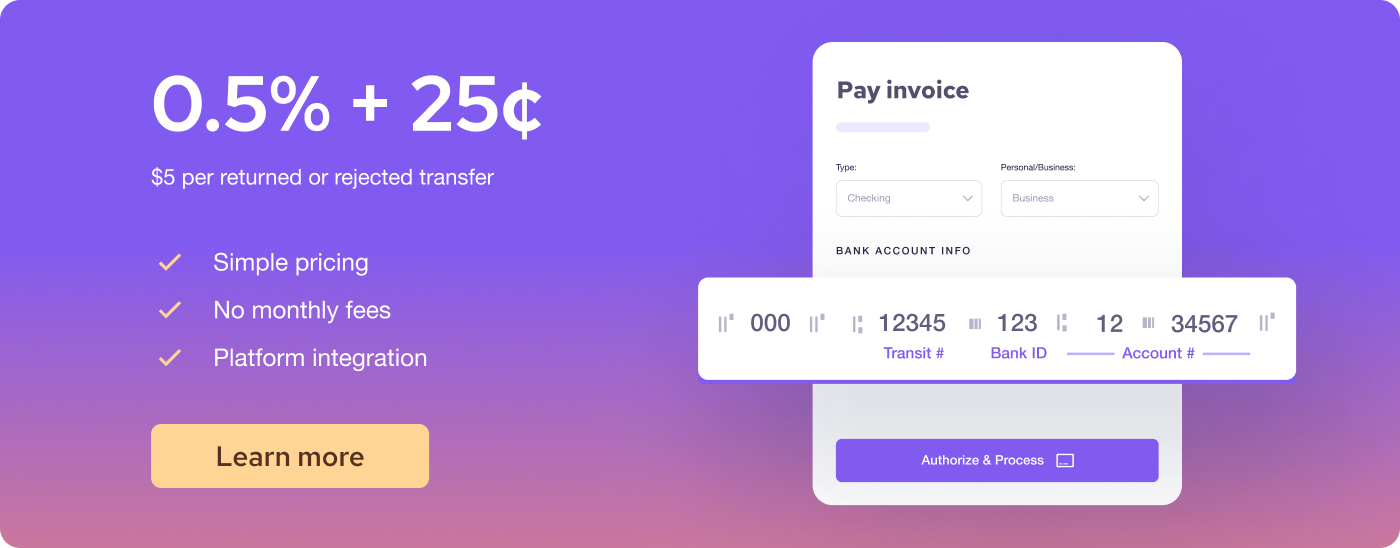

2. Offer ACH payments

ACH payments typically have much lower processing fees compared to credit card payments. For example, Helcim charges 0.5% +25¢ for each ACH transaction, and the fees are capped at $6. Setting up ACH payments can help you save on transaction fees for high-ticket items or subscription-based services.

3. Use convenience fees

A convenience fee is a fixed charge applied when customers choose to pay by credit card instead of the usual payment method your business accepts. This fee helps cover the additional costs of processing credit card payments, offering customers the convenience of using their card.

Hidden credit card processing fees and costs

Now besides the credit card processing fees, there are other hidden costs that merchants can be charged by their credit card processor.

The bad news is that many of these fees are entirely unnecessary and are only "standard" in the industry because too many companies have been reaping benefits from these fee schemes for years.

Here are a few of those hidden fees that you'll want to keep an eye out for when you're shopping around for credit card processors:

1. PCI compliance fees

Merchants must comply with PCI (Payment Card Industry) standards to ensure secure transactions. Many processors charge PCI compliance fees, typically ranging from $50 to $200 annually, to cover the cost of certification. However, Helcim helps you stay PCI compliant at no extra cost.

2. Credit card chargeback fees

If a customer disputes a transaction and requests a chargeback, you may be charged with a chargeback fee. This fee, usually between $20 to $50 per chargeback, covers the administrative costs of handling the dispute. For Helcim merchants, there’s a free tool available to help you manage and counter chargebacks. Best of all, if you successfully win the dispute, there’s no cost to you. According to Kount, merchants win 77% of the time when countering chargebacks, making a tool that streamlines the process invaluable.

3. Early contract termination fees

Some credit card processors require you to sign 3-4 year contracts and charge early termination fees if you decide to switch providers before the contract ends. These fees can reach several hundred dollars, so make sure to check the terms and conditions before signing up with a processor. If you're currently stuck in a credit card processing contract, check out our guide on how to exit them for both US and Canadian merchants.

4. Non-qualified credit card fees

Some credit card processors advertise low transaction fees but may add extra charges when a transaction doesn’t meet their hidden criteria, such as when a rewards card is used or the card details are manually entered instead of swiped or tapped. These “non-qualified” credit card transactions often cost the processor more than their advertised rates. As a result, they charge these additional fees to maintain profitability.

5. Initial setup fees & application fees

Most credit card processing companies charge a setup fee when you open a merchant account. Some even include a separate, non-refundable "application fee," meaning you’ll be charged even if your application is declined and you can’t accept credit card payments. Additionally, some processors impose an "annual fee," which essentially acts as a recurring setup fee, charged each year—typically in December or January. These annual fees can exceed $100 and are often hidden in the fine print of your contract, so it's important to read the terms carefully.

Save 25% credit card transaction fees with Helcim

If your business wants to accept credit cards at a low cost without monthly fees, contracts, or hidden charges, Helcim is the ideal solution. Why should you process credit cards with Helcim?

-

Helcim offers 25% lower fees on average compared to other flat-rate credit card processing companies like Square, PayPal, or Stripe. This means more savings for your business.

-

You get a free merchant account and tools for accepting in-person and online payments, such as invoicing, virtual terminal, and POS software.

-

You only pay transaction fees. There are no hidden fees, no monthly fees, and no long-term contracts that lock you in.

Sign up now and start accepting credit cards at low cost with Helcim.

If you're ready to switch to Helcim but feel stuck with your current provider, we’ve got you covered. Our Merchant Buyout Program offers up to $500 in credits to cover your contract cancellation or equipment costs.

Besides, we'll guide you through the entire process—from handling cancellation paperwork to migrating your data to Helcim.

Break up with your current provider for better service and lower fees. Switch to Helcim with our Merchant Buyout Program.