Looking for a payment processor can be kind of like dating.

Maybe the relationships you've had up until this point have been less than ideal; you know, the kind where you put in all the effort and they somehow take you for everything you've got.

So now, a little jaded and a little more wary, you're back on the market looking for the one.

Don't worry. We've put together a quick guide on finding the perfect (payment processor/ merchant) match in 2023.

Whether you're looking for someone who matches your busy lifestyle or career, or someone who is dependable, consistent and good with money. We've got it all.

We get down to the nitty-gritty on what a merchant services account is, why you need one (or don't), and supply you with the questions you need to ask prospective merchant services providers. By the end, we hope that you'll feel ready to get back out there and find the right match and, ultimately, make the best decision for your business.

What is a merchant account?

With all these names and terms flying around, it's important to understand what a merchant account actually is - by the way, some merchant service providers offer them, and some don't.

A merchant account is a type of business bank account, and it allows your business to accept payments.

The merchant account is founded on an agreement between your business, your bank, and your credit card processor for the settlement of card transactions processed at your place of business — basically, it is an agreement that stipulates how you get paid and where the funds go for the card transactions your process.

Think of a merchant account like a Venn diagram. You and the payment processor are on either side, with the merchant account in the middle. The funds flow into the middle account and can be accessed or pulled from either side.

The funds received from processing credit cards at your business are first deposited into your merchant account and then fed to your business bank account, usually on a daily or weekly basis.

A merchant account is not an official bank account, and it does not store funds for an extensive period. It functions as a hub where funds can be deposited and frozen if there are any chargeback claims or suspicion of fraud.

Why do I need a merchant account?

You might be asking yourself, "why can't the money be transferred directly into my bank account?"

The answer: It comes down to risk.

There is always a risk that online transactions just won't go through. There may be fraudulent charges or chargeback claims made, and processors need a way to hold funds or withhold future payments until those claims are resolved instead of retroactively requesting funds be returned. Once the claims are resolved the funds can be transferred within a couple of business days.

Plus, a merchant account can actually be helpful by collecting the funds from multiple locations and batches and consolidating your payment into one rather than numerous.

What type of merchant account do I need?

Not every payment provider offers its merchants a designated merchant account.

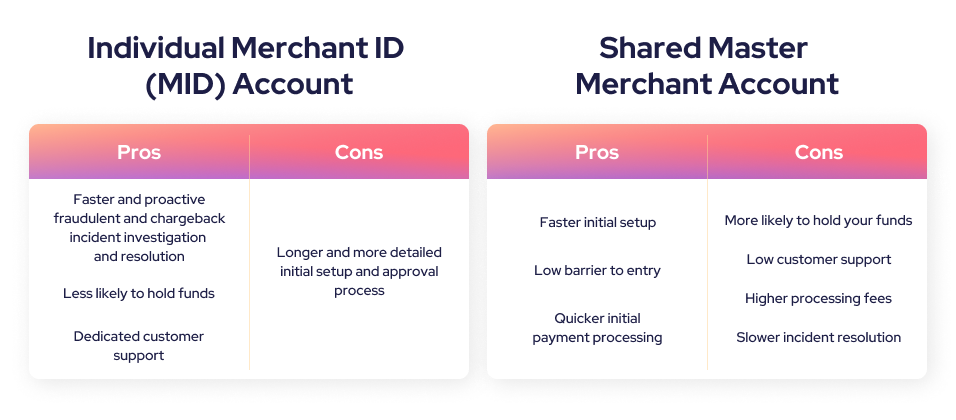

For example, with some national payment processing providers like Square, business owners don't have an individual merchant ID (MID) but instead share one master merchant account that belongs to their payment processor.

A shared account means that all the merchants who process payments with that processor share one merchant account where the funds are deposited and then transferred to your personal bank account.

Whether you want to sign up with a service provider that offers a designated merchant account to your business or with a provider like Square will depend on your business needs and personal preferences.

There are pros and cons to each, mostly surrounding the initial setup time and ease, underwriting process, and fraud protection/ processes. See how both types measure up:

How difficult is it to open a merchant account?

While providers like Square or Paypal are known for their low barrier to entry and simple signup, there are often trade-offs with providers that don't offer a merchant account such as fund holds, higher fees, and disappointing customer support.

The advantage of an individual merchant account is that your approval is predicated on a higher degree of confidence in your legitimacy as a business, resulting in a lower risk of fraudulent activity to the processor. This means you are much less likely to have your funds frozen for suspicion of fraud.

P.S speaking of frozen funds, watch our Facebook video recalling a merchant horror story that involved over 100k frozen by another payment processor.

With all that being said, there are rare providers who encompass all the advantages that a modern provider like Square can offer (like no contracts or hidden fees, fast and easy signup process, custom pricing, and a comprehensive technology solution), as well as the advantages that some of the more traditional, established providers can offer customers. That includes lower rates, great customer service, comprehensive merchant services solution, and your own merchant account.

Here's a hint, you've stumbled upon one such unicorn payments provider by clicking on this very article.

Why do merchant accounts need to be approved?

Payment processors are diligent about approving merchant accounts in a scrutinous manner because they can be held liable for refunding customers.

For example, they would have to cover the cost of a chargeback if a merchant accepts a payment but is unable to deliver their product and their business goes under or they commit fraud.

Similar to loan approvals, processors will look at a number of factors before approving your merchant account to ensure nothing fishy is going on to mitigate any potential risk.

These factors might include:

- The industry your business is in.

- Credit and debit cards volume.

- The average size of your transactions.

- The delay between when a customer pays and when they receive their products.

Typically, a processor will also perform a personal credit check on the owner of the business or ask for your business's financial statements to make sure it can support potential refunds and chargebacks.

Taking the time to approve a merchant account helps protect merchants, customers, and payment processors.

Questions you should ask merchant service providers

So now you know what a merchant account is and how you can go about getting one. If you're new to accepting credit card transactions, whether they are in-person, online payments, contactless payments, or something else, it's essential to know what your business needs are and what you should be looking for when seeking out a provider.

Don't get duped into another dead-end relationship with hidden baggage like surprise fees. Payment providers know all the right things to say to seem like prince charming - get catfish savvy by familiarizing yourself with these common industry tactics.

If you already have a merchant account, you're well on your way to having established your business and setting up consistent cash flow; it's worth considering the following questions and asking yourself if you are getting the most out of your relationship with your service provider. If you think you might be paying too much in fees, or there are some things about your contract that you don't understand, you may want to consider how to get out of your merchant contract or switch.

The last thing you want, though, is to switch to another provider that is just as bad or worse than your current one.

Whether you're shopping around for payment options for the first time or looking for a new MSP relationship, we've put together a list of five questions for you to ask prospective merchant service providers:

1. What are the contract terms and conditions?

Many merchant service providers have lengthy long term contracts that are difficult or impossible to escape. Ask your current provider how long your contract is, what happens if you want to end the contract early, and what you need to do to cancel the contract when the term is up. (Pro tip: look for a processor who offers a merchant account on a month-to-month basis).

The term is expired, but that doesn't always mean your contract is over. Some payment processors may also include auto-renew clauses that business owners should know of. Being aware of this clause will keep you from inadvertently being signed up for a monthly fee for another term for example. Ensure you fully understand the terms and conditions of the contract you're signing to avoid future frustration and regret.

2. What is the real processing fee?

When going through the signup process, make sure you clearly understand if you're getting an "introductory rate" that will increase at some point. Or ask if there is any rate guarantee that the payment processor can offer. Credit card processing rates will vary depending on the type of transaction, the card used, and the business's monthly processing volume. If the processing rate you're being offered as a merchant seems lower than what you expected, clarify exactly which transactions or card types the rate does and does not apply to.

Be sure to clarify if the processing fee is a flat rate or a percentage of your transaction volume. How a payment processor calculates their processing fees can make a big difference in what you end up paying monthly. As a general rule, you should try to go with a processor that offers interchange-plus pricing, as it's widely regarded as the most affordable way to process credit cards.

3. Are there any additional fees or charges that I should be aware of?

Cancellation fees, early termination fees, PCI Non-Compliance fees, chargeback fees, account change fees, and equipment rentals are all additional costs that you and your business should look out for when it comes to shopping for a merchant account. These are usually charged in addition to your processing fees, and they can add up pretty quickly. Understanding why you're being charged this extra cost and how you can avoid it will save your business money in the long term. Try to find a provider who is very clear and upfront about not charging your businesses any hidden fees on any transaction, whether they are online transaction or in person payments.

To manage fees, merchants can offset their processing fees by passing them off to their customers, often referred to as a surcharge fee. You can also utilize a cash discount incentive to get the customer to pay in cash instead of using a credit card to reduce processing fees.

4. If I have a problem, how can I get help?

Each merchant account provider will provide different customer support options and what works best will vary based on a business's preference. Whether you prefer to submit an email, chat online, or pick up the phone and speak to someone, it's important to know how you can contact your payment processor and when their support team is available.

If a merchant account provider outsources their customer service instead of training an in-house team, this may also impact your decision on who is the best fit for you. Having a knowledgeable team that actually works within the walls of your provider can give you peace of mind in knowing that there is a team dedicated to offering support when you need it.

There aren't many merchant account providers who invest heavily in merchant support, and many businesses just outsource their support to save money or don't even have a customer support line. This may not seem like a critical consideration when researching your payment options here, but like any business that has already been accepting credit cards knows, it's very important to be able to get good help when you need it.

5. What software or integrations do you offer?

Specific software integrations can help streamline your business and make you more efficient. For example, if you use QuickBooks, it would be beneficial to ensure your payment processor can integrate with their platform. Whether you're setting up an online store or managing your inventory, or looking to take electronic payments, confirm which software services your payment processor already offers and which software integrations they support to avoid frustration down the line.

By asking these questions ahead of time, you are protecting your small business from surprises like unknown fees and inaccessible customer service teams. Not to mention, ensuring your credit card processor offers complementary software is a great way to prepare your small business for growth in the future.

What is the best merchant services provider?

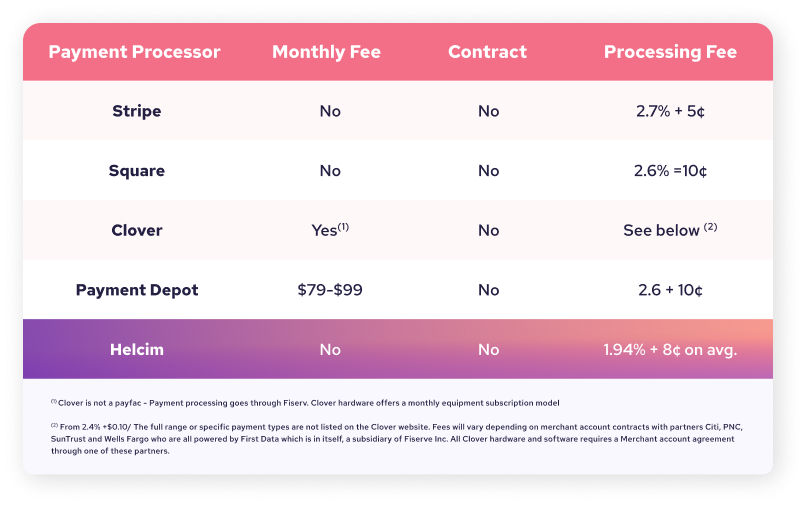

Setting up a merchant services account with a credit card processor is a significant step in taking your business from the bedroom to the big-time. Still, it's essential to understand what you're getting from your services provider, in return for paying for their service unwavering loyalty. Every business will have different needs, so ask the right questions. We put together a brief comparison chart to help you narrow down your needs, understand contracts and fee structures and get a better idea how these five merchant service providers can help you service your customers effectively in 2023.

Final thoughts

Choosing a payments provider can be a complex process, but understanding what options are available to you and how each provider differs can keep you from falling in with the wrong processor. We hope this guide was helpful and that you can find the merchant service provider you've been searching for!