-

Content

"Helcim provides credit card processing the way small businesses need it: with complete transparency." -PC Magazine

Have you ever felt like you've fallen victim to a sales ploy? Or felt like you overpaid for something that definitely wasn't worth it? It can be pretty unsettling when that cognitive dissonance settles in and you're left to deal with the fallout. Needless to say, if there is one thing we can all relate to - it's feeling ripped off.

One culprit of the post-purchase blues in business owners is the questionable tactics employed by a lot of traditional payment processors in how they apply their fees. Of course there are the set-up fees, the cancellation fees, the PCI non-compliance fees, and a host of other things your payment processor can charge you for seemingly on a whim, but what about the basic pricing structure of your agreement? Could that be the thing that is actually costing you the most?

Traditional payment processor pricing

Most traditional payment processors use what is known as interchange differential pricing, which charges a merchant different fees per transaction based on which of those transactions are classified as "qualified" and "non-qualified". Oftentimes, payment processors would quote merchants the qualified rate to persuade them into signing a contract, but what went unsaid is that very few transactions actually end up "qualifying" for this more attractive rate, and the business owner was left paying more than they ever anticipated for the majority of their customers' purchases.

Interchange differential pricing is similar to another form of pricing, called tiered pricing. Unfortunately, this method of pricing has few advantages for merchants besides being relatively easy to understand and it is widely regarded as an expensive and often unfair arrangement between merchant and provider.

Not better left unsaid

Another reason you might be paying more than you had initially hoped for your processing services is that the company may have inserted some unfortunate terms into your contract without you noticing. When a payment processor includes a specific rate within their terms that seems too good to be true, it very likely is. And if you ever notice a fine print that reads something like "plus applicable fees" with no description of what those fees are or how much they could be, you should run as far away from that company as possible.

A better alternative

Now, imagine a payment processing company that isn't trying to pull the wool over your eyes, but uses a transparent pricing model and partners with you to help your business grow. Thankfully (at least in the payments world), unicorns do exist!

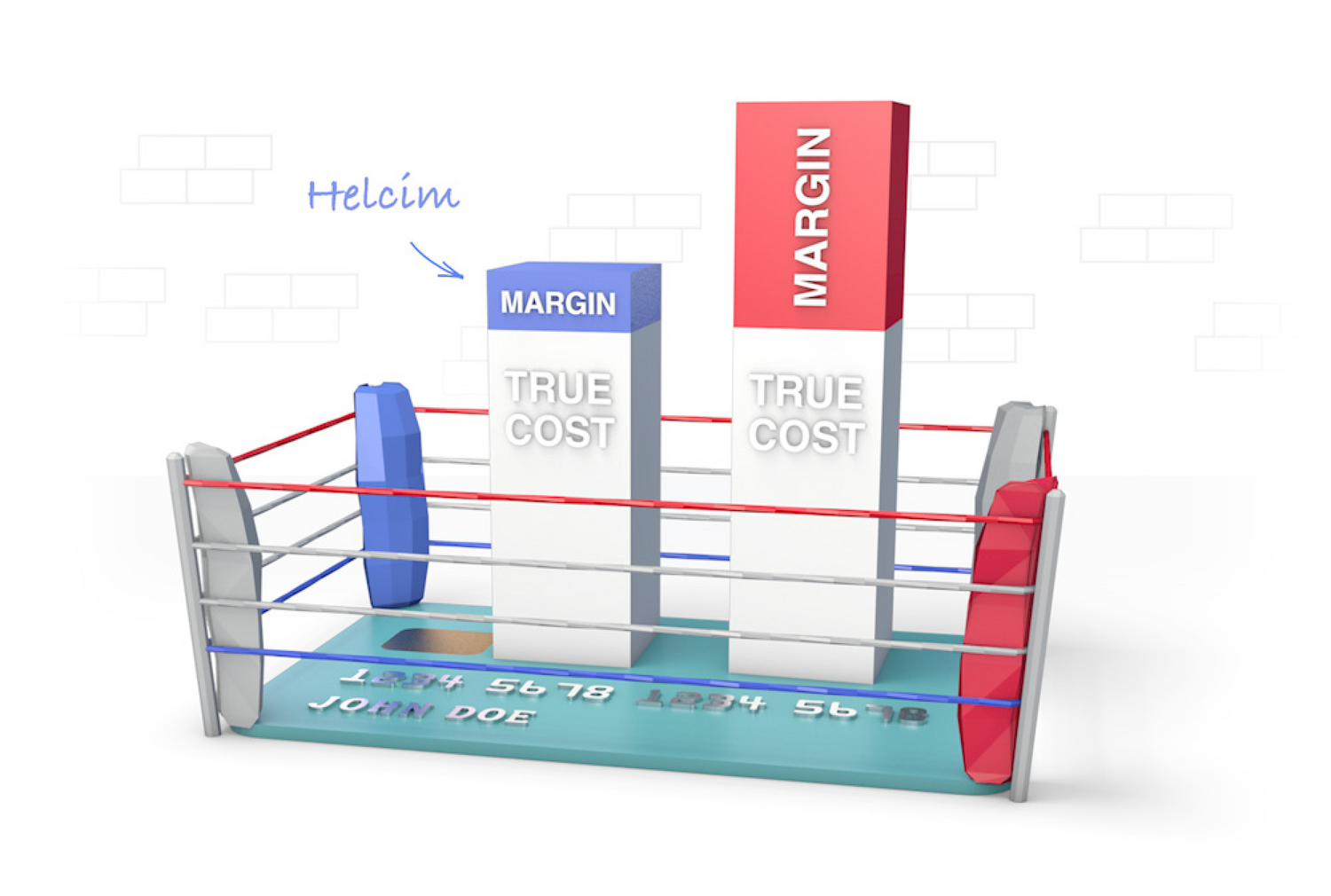

Helcim's unique Interchange Plus pricing model may seem complex at first glance, but this method of processing payments comes with no hidden costs, and gives you the relationship you deserve to have with your service provider.

Interchange Plus pricing

All card providers (like Visa, Mastercard, or Amex) charge a standard fee for every card transaction known as the interchange. However, these fees can change based on what type of card is being used by your customer and whether the transaction is being processed card present (in person) or card not present (e.g. online). For example, a basic cash-back Visa card may have a relatively low interchange fee, but something like an Avion card, which is considered a premium credit card, will typically be more expensive.

How Interchange Plus pricing works for you as a merchant is you get to see exactly what the interchange rate is for every transaction you process. Helcim's margin, on the other hand, never increases based on the interchange rate, but remains a set amount. In fact, Helcim's fee only decreases the more transactions you process thanks to our volume discounts that are applied automatically!

Save 25% credit card processing fees with Helcim

Credit card processing fees are a pain for most merchants. With Helcim's interchange-plus pricing, thousands of merchants have reduced their credit card processing fees by ~25%.

If you're ready to switch to Helcim but feel stuck with your current provider, we’ve got you covered. Our Merchant Buyout Program offers up to $500 in credits to cover your contract cancellation or equipment costs.

Besides, we'll guide you through the entire process—from handling cancellation paperwork to migrating your data to Helcim.

Break up with your current provider for better service and lower fees. Switch to Helcim with our Merchant Buyout Program.

Break up with bad rates.

Feeling stuck with your provider? We'll waive $500 of your processing fees when you switch to Helcim.

Related Articles

-

What Do Payment Processors Do?

Alivia Massimillo | April 16, 2024

-

Your guide for the world of payment processing

Ryleigh Stangness | September 8, 2023

-

Choosing a Payment Processor for Seasonal Merchants

Ryleigh Stangness | April 26, 2023

-

Are Payment Processing Fees Tax Deductible?

Ryleigh Stangness | March 28, 2023

-

How to reduce your credit card processing fees

Ryleigh Stangness | November 1, 2022

-

Payment Processing Horror Stories

Danny Randell | October 31, 2021

-

Understanding Different Payment Processing Pricing

Chris Reid | September 12, 2020

-

Top 5 Misleading Tricks Used by Payment Processors

Nic Beique | July 9, 2020