In addition to being upsetting for your customers, declines also represent lost sales for your business if not resolved. Understanding the reason behind why declines happen in credit card processing can help you to resolve the issue and prevent declines in the future.

Who Decides if a Card is Approved or Declined?

When a credit card is approved, it is the customer's issuing bank, not the payment processor or the card network, that is approving the card. An approval means that the credit card number and expiry dates are valid, the customer has enough credit for the transaction amount requested, and that the card has not been reported as stolen or compromised. It is important to note that an approval is not a guarantee of the transacted funds. There is always the chance that a chargeback is filed at a later date by the cardholder, either because their card was stolen or because of a dispute with the merchant.

Why Does a Credit Card Get Declined?

When a credit card is declined, it is typically declined by the cardholder's issuing bank, the entity that decides the outcome of the transaction. Most issuing banks do not provide a detailed reason for the decline to avoid fraudsters from "testing" credit cards and trying to determine the reason for the decline. If you get a decline notice, there are a few primary reasons that are most likely the cause. We list them below:

Main Types of Credit Card Declines

DECLINED - INVALID CARD

When you receive an "Invalid Card" error, it means that the system has completed a MOD10 check, the checksum formula used to validate a variety of identification numbers, and the formula was unable to validate the card numbers meaning the card entered is invalid. This is usually because the credit card number was entered incorrectly.

DECLINED - EXPIRED CARD

If a customer has a card that has passed the expiry date listed on the front, then the card network won't be able to process it and they will need to present an alternate payment method or provide the updated expiry date. A large portion of declines are due to this reason.

DECLINED - ND

If you receive this message, then it is a normal decline by the bank. The most common reasons for a Declined - ND message are due to insufficient funds or a restriction placed on the card (such as reaching the credit limit).

DECLINED - CALL FOR AUTH

This is also a decline, but there is a pathway for potential approval. In this case, the bank is unsure about the transaction and would like the merchant to call the processor's call-for-auth center to do further verification on the transaction. If approved over the phone, the call center agent will provide you with an approval code for the capture.

DECLINED - PICK UP CARD

This decline means that you should "pick up the card" if you are in the physical presence of it. Think of movies where the waiter takes scissors and cuts the card in front of the customer. This is because the card has been taken out of circulation, either because it was lost and has been replaced, or was reported stolen. While not a certainty, this can be a warning sign that a customer is trying to process a fraudulent transaction using a stolen card. It should be noted that a merchant should never compromise their safety in trying to repossess a credit card.

Other types of credit card decline codes

Address Verification System (AVS) Failure

If you receive an AVS decline code, it could indicate a mismatch between the billing address provided by the customer and the address on file with the issuing bank. Payment processors and issuing banks ask for the customer's address to compare it against the one they have on file to protect the cardholder from fraudulent transactions.

This decline means that the transaction should not be processed, as it may be a warning sign of potential fraudulent activity.

AVS decline codes include AVS A (the street address matches, but the postal code does not.)

AVS R refers to an indeterminate outcome, retry, may apply when the format is incompatible, the address information is not verified, or the system is unavailable or has timed out.

AVS U means unable to verify.

AVS Z refers to a partial match on the postal code only.

Providing additional fields for shipping addresses different from the billing address may help prevent auto declines on AVS checks. This way, you are still verifying that whoever is using the card has all the additional details the cardholder would know, like a CVV or security code and billing address, while providing them options to buy gifts or have their items shipped elsewhere.

Although they can sometimes result in inconvenient declines, AVS systems can also help prevent card attacks and lower your processing rates since you will reduce your risk of fraud.

Suspicious or high-risk transactions

Fraud and suspicious activity can happen with in-person transactions and online. A fraudster can tamper with your terminal, use a stolen credit or debit card, or use a stolen card for a purchase and request a refund on another card leaving you to deal with the cardholder's chargeback for the initial transaction.

By following best practices for card-present and card-not-present transactions, you can reduce your risk of processing a fraudulent transaction.

However, if you come across a decline code related to a suspicious or high-risk transaction, it may mean the transaction has been flagged for further review or investigation.

This doesn't always mean the cardholder is a fraudster, it may mean that the transaction amount is unusual, they've made more transactions than usual that day, or some other change in acticity such as travelling.

Some of the standard codes that indicate this include

- 200 (Decline - suspected fraud)

- 201 (Call issuer - suspected fraud)

- 203 (General decline - suspect fraud)

Insufficient Funds

Another reason for a declined transaction could be insufficient funds, typically indicated by a decline code related to the specific reason for the decline.

For instance, code 51 (Insufficient funds) could mean that the cardholder's account does not have enough money to cover the transaction amount.

Code 57 (Transaction not permitted - card) could indicate that the card cannot be used for the attempted transaction type.

Finally, code 61 (Exceeds withdrawal limit) suggests that the cardholder has reached their limit for withdrawing cash.

While you might not see the code on the terminal, these are some reasons a declined payment method may occur, even when the customer is sure the funds are available.

Tips for Dealing with Credit Card Declines

-

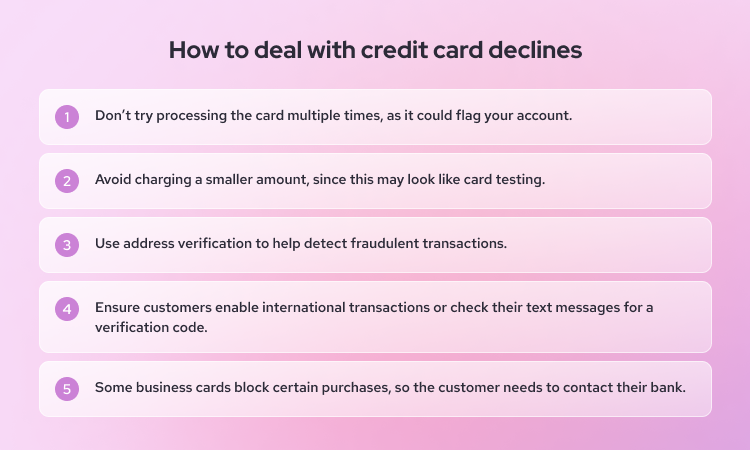

Don't try processing the credit card multiple times. You will continue to receive decline messages and your merchant account may be flagged for potential fraud or abuse. Instead, ask the customer for another payment method.

-

Try to avoid processing the credit card for a smaller amount, as this may be seen as "testing" the card limit, and the transaction may be flagged for fraud. Instead of trying the transaction again at a lower amount, ask for another payment method from the customer.

-

Use services like the address verification service to help determine the validity of transactions and avoid processing fraudulent transactions.

-

For international transactions, some credit cards can have restrictions by default to decline all international payments. In this case, the customer would need to call their issuing bank (the number can be found on the back of the card) and let them know they are trying to process an international transaction. The bank will "unlock" the card, and you can try processing it again.

-

Some credit cards, especially business and corporate cards, can have restrictions on the type of purchases that can be made. Each merchant account has a SIC (standard industry code) associated with it, and a specific SIC could be prohibited from charging certain types of cards. In such an event, the cardholder again would need to contact their issuing bank to unlock the card before you can try processing the transaction again.

How to lower credit card decline rates

While a credit card decline can help flag credit card fraud and payment failure due to issues with the credit card issuer or cardholder, failed payments can also hurt your customer experience, loyalty, and bottom line when the payment failure is the business's fault.

Familiarize yourself with the types of credit card fraud that can harm your business and follow industry best practices to follow to reduce errors and declined payments when processing a credit or debit card. Begin by ensuring that the payment gateway and software are current, using fraud detection tools, verifying customer information before processing transactions, and following industry best practices for payment processing.

FAQS

What is a soft credit card decline?

Have you ever had a card decline that left you befuddled and embarrassed? The merchant might ask if you want to try another payment method, and you may reassure them you have the funds in your account; you just need to try again. You find yourself letting out an unexpected sigh of relief when "Approved" blinks on the screen.

Soft declines are a type of decline that is categorized by the transaction stage where the failure occurs. Typically associated with debit cards, the decline will happen after the card is approved by the issuing bank, indicating the card is authorized. However, the message was lost somewhere along the way back in the credit card processing cycle, and it came up as declined.

**Some common reasons this occurs include: **

- Insufficient funds

- The card has reached its expiration date

- The card has reached its credit limit

- The credit card payment amount is an unusually large purchase

- The card issuer has limited the number of transactions the cardholder can authorize.

Sometimes this is a temporary authorization failure and may be successful if you have your customer try again.

What is a hard credit card decline?

A declined credit card or debit card may be considered hard if the transaction fails to be authorized by the issuing bank. Typically, these failed payments occur when a credit card transaction uses a stolen or invalid card or their bank account has been closed. In this case, you must ask your customer for a different payment method.

Can a declined payment still go through?

Yes, there may be a timeout or network error wherein a payment may have been processed, but the terminal received a network error message. Customers may notice these charges on their statements or see a duplicate charge. In these cases, it is always good practice to provide your customer with their receipt of the transaction and print a merchant copy in case they need to file a chargeback later for a duplicate transaction or if they paid but did not receive the product, etc.