-

Content

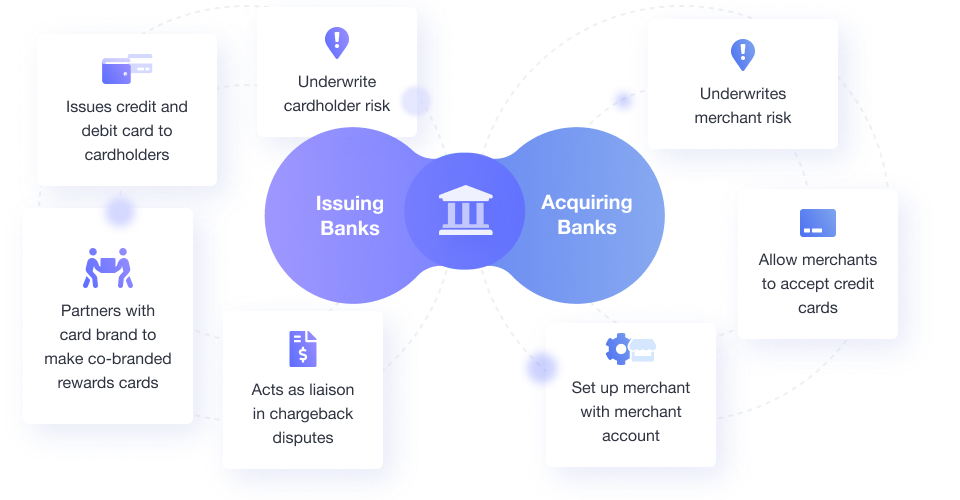

Acquirer vs. Issuer: How Are They Different?

Acquiring banks and issuing banks (sometimes referred to as "acquirers" and "issuers") are two important institutions in the credit card processing ecosystem.

Knowing the role that each bank plays when you process a transaction can help you understand how payments are processed and who is responsible for what at each step.

In this article, instead of redefining what these institutions are and what they do, we'll be talking specifically about how they differ, and use some examples to help demonstrate those differences.

The ultimate guide to accepting credit cards.

Discover essential knowledge and industry insights to increase your bottom line.

Two Sides of the Same Coin

Issuers and acquirers really are like two sides of the same coin. Though they differ in their function and in who they service as an institution, they aren't exclusive of one another when it comes to credit cards. To put it another way, one can't exist without the other. These institutions rely on one another to facilitate the millions of transactions processed every day via the credit card networks.

One core difference between the two is this: acquiring banks accept payments, whilst issuing banks make payments.

Another distinguishing feature of these entities lies in who they service, and for acquirers, that's businesses, while for issuers, it's people like you and me, or anyone who has a credit card.

Banks Issue Cards and Acquirers Help Merchants Accept Those Cards

When you boil down the essence of these two types of financial institutions, you get one that's customer or "cardholder" facing, and another that's merchant or business facing. You see, in order for Visa and Mastercard to get their cards into the hands of customers, they need issuing banks to take on the risk associated with credit card debt (which they gladly do for the privilege of offering their customers access to the card networks and the interest they stand to gain from unpaid debt). On the other hand, the card brands need acquiring banks to bear the financial burden associated with accepting what are essentially debt payments in order to get businesses paid.

To recap, in general when you think of acquiring banks, think business, and when you think issuing banks, think personal.

Example 1:

If a cardholder has an issue with an unfamiliar transaction or suspected fraud, they will contact their issuing bank.

Example 2:

If a merchant has an issue with a settlement, they will need to contact their merchant service provider which in many cases is the acquiring bank.

Transactions: Where Issuers & Acquirers Meet

Though issuing banks and acquirers are very different entities, they do work closely together, and never closer than at the transaction point. It's here (when a customer taps their credit card, for instance) that the issuers and acquirers are working seamlessly in tandem to facilitate the transfer of funds from customer to merchant.

Note: There is the odd occasion where an issuing bank is also an acquiring bank, but this is very rare. In Canada, the only bank that performs both roles is TD Canada Trust.

Issuers and Acquirers are both necessary components of the payment circuit, and as mentioned above, one does not operate without the other.

PayFacs vs. Acquiring Banks

Payment facilitators like Helcim form another component of the payment chain. Though not an acquiring bank in their own right, both payment facilitators and acquiring banks can be merchant service providers.

It is up to the merchant when setting up their business if they'd like to work directly with an acquiring bank or a payment processor to set up a merchant account. Some of the benefits to not working with an acquirer is that payment facilitators typically have quicker sign ups, cutting edge software inclusions, and dedicated customer service.

Final Thoughts

Issuing and Acquiring banks both form an essential part of the payment processing ecosystem. Though they work differently and service different sectors, they work together to make the millions of transactions processed every day a possibility for customers and business owners.