Whether you are looking for an in-person POS system or a way to accept credit cards online, a merchant acquirer is a key player in the payment industry. When you process a customer's credit card payment, the transaction moves through multiple financial institutions and systems before the payment ends up in your business bank account. It's a complex chain of which one key component is the merchant acquirers.

Understanding the role of an acquiring bank and how it interacts with the other key players in the industry will help you understand the journey a credit card transaction takes and ultimately help you to better assess your options when looking for a payment processor.

Let’s dive in.

What is a merchant acquirer?

A merchant acquirer, sometimes referred to as credit card acquirer or acquiring bank, sets merchants up with merchant accounts, which is the processing arrangement between the business and their credit card processor. This agreement with the acquiring bank (or in many cases, the payment processor acting on behalf of the acquiring bank) allows for the exchange of funds with the card-issuing banks and your business.

Simply put, the "acquirer" is the financial institution that works with merchants, while the issuer is the financial institution that works with customers. Acquirers are the banks that allow merchants to accept credit card payments. Either the acquiring bank or the payment processor then facilitates the transfer of those payments from the merchant account to the merchant's business bank account (which is usually at an issuing bank).

The acquirer's role in credit card processing

Here's how an acquiring bank fits into the payment cycle:

When you process a transaction for a customer who has come into your store location or submitted an order through your online store or payment gateway, the transaction is processed through an acquiring bank. (Note: if you are using a payment processor, the transaction will be communicated through them first.) Acquiring banks allows merchants to accept credit card payments from cardholders and their issuing banks.

When a cardholder makes a purchase, the merchant’s acquiring bank works on behalf of the merchant to confirm with the cardholder's issuing bank that they are authorized to process the payment and that the cardholder has the funds available for the transaction. By settling funds at the end of the day, the funds that were previously authorized during the transaction can be pulled and paid from the cardholder's account to the acquiring bank or payment processor. The payment processor or bank will likely deposit the money into the merchant's bank account unless they see any red flags, in which case they might freeze the funds for the sake of avoiding chargebacks and fraud prevention.

Merchant acquirers may be less visible to merchants and cardholders compared to issuing banks because they often work behind the scenes, while their partners (payment processors like Helcim) are the ones who work directly with merchants during the signup process or when questions arise about the merchant's account.

Examples of acquiring banks

To make sense of what an acquiring bank is, let’s look at a few real-world examples. Acquiring banks are the backbone of credit card transactions for businesses, handling payments and making sure funds get to the right place. Each one operates slightly differently, but they all serve a similar purpose: making sure merchants can accept payments smoothly.

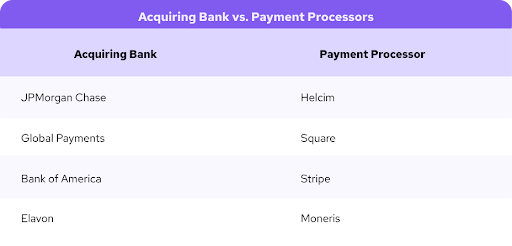

Take JPMorgan Chase as an example. Chase is one of the largest acquiring banks in the world, working with millions of businesses to make sure their payments process securely and efficiently. Every time a Chase-powered business takes a payment, JPMorgan Chase steps in behind the scenes, making sure that payment goes through.

Can a merchant acquirer be a payment processor?

Yes, a merchant acquirer can also be a payment processor, but they don’t always play both roles.

Let’s break it down.

Think of a merchant acquirer as the bank that "acquires" the money for a business when a customer pays with a card. The acquirer connects with other banks and card networks (like Visa or Mastercard) to make sure the payment reaches the business’s account. Meanwhile, a payment processor is like the middleman that moves all the data back and forth between the business, the acquirer, and the card networks, handling the technical work so transactions go through smoothly.

Some companies, like Elavon or Chase, are both acquirers and processors. They make sure the money gets to the business and also handle the technical side of the transaction. This setup is convenient for businesses because they have one provider for both parts, making setup and management easier. However, in many cases, businesses will use different providers for acquiring and processing. For example, a business might work with Bank of America as its acquirer and use Fiserv or Global Payments to handle the processing part. This flexibility allows businesses to pick the providers that best meet their needs, whether they’re looking for specific features, fees, or customer support.

What is the difference between an acquiring bank and an issuing bank?

Now that you have an understanding of a merchant acquirer or acquiring bank let's clarify the difference between them and the issuing banks. The issuing bank is the bank associated with your customer's card. Your customer will have to go through a bank to open an account and be approved for a credit or debit card. Every time they use these cards to make a purchase, the credit card machine reads their card details and communicates with the card networks, acquiring banks, and payment processors who act as a mediator to the customer's card-issuing banks to pull the funds out of the customer's account or credit.

How merchant acquirers make money?

Just like every player in the credit and debit card payment game, acquiring banks make money off the process. The way they do this is by getting together with the card network brands to determine a reasonable fee to charge payment processors to cover their own costs. This fee is called the interchange fee, and it is a cost that affects both the merchant and payment processors.

Payment service providers then need to make their own margin which they charge merchants, or in the case that you process directly through an acquiring bank, they will tack on a small margin as well. This is where your pricing model comes into play- but remember that no matter which processor you choose, they all pay the same cost, or interchange fees, to the acquiring banks and card networks.

For example, Interchange Plus pricing passes on the wholesale interchange fee with a small, consistent margin for various transaction types. Flat rate pricing, on the other hand, charges one flat margin, which accommodates their own cost for fluctuating interchange fees for low and high-cost transactions but doesn't pass on the savings.

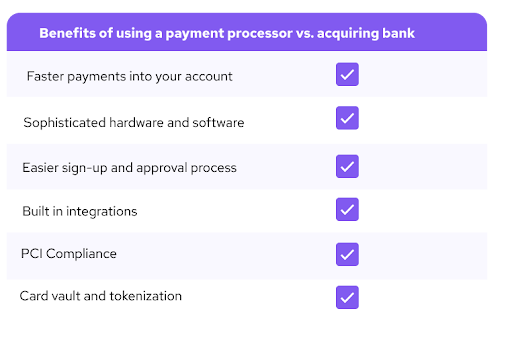

Accepting payments: payment processor vs. acquiring bank

Instead of signing up with an acquiring bank directly, you can instead choose to sign up with a payment processor. If you sign up with a payment processor, they will communicate with the issuing banks through their acquiring bank partner and act as a mediator between your business and the cardholder issuing banks.

Payment processors tend to be faster and more sophisticated when it comes to payment hardware and software options, but also when it comes to integrations and built-in tools. With a merchant account, your payment provider can also help get you up to speed to become and remain PCI compliant and relieve you from doing all the yearly work necessary to stay compliant and keep you and your customer's sensitive credit card data secure with tools like card vaults and tokenization.

If you're looking to get started accepting credit and debit card transactions, a payment service provider or merchant service provider may be an easier all-in-one solution for payment processing rather than trying to go directly through a merchant acquirer bank.

Final Thoughts

Understanding who merchant acquirers are and what they do is a great foundation for understanding how a credit card transaction works and the costs and hands that the payment process passes through, which ultimately contribute to the pricing model and fees you pay to accept payments. Both issuing and acquiring banks play an important role in credit card processing. If you'd like to learn more about how credit card processing works, checkout this article.

FAQs

Is Visa a merchant acquirer?

No, Visa isn’t a merchant acquirer. Visa is a card network, meaning it manages the network that connects banks, acquirers, and merchants to help process payments. Visa allows money to move securely between banks, acquirers, and merchants when customers pay with a Visa card, but it doesn’t directly acquire the money for a business. That’s the role of a merchant acquirer, which is typically a bank or financial services provider that connects with Visa’s network.

Is Mastercard a merchant acquirer?

Like Visa, Mastercard isn’t a merchant acquirer. Instead, it’s a card network that ensures secure and reliable communication between the merchant’s acquirer and the customer’s bank. Mastercard provides the infrastructure and security to make payments possible, but it doesn’t directly handle the acquiring process. Acquirers like Chase, Elavon, or Bank of America work with the Mastercard network to settle payments for businesses.

Who is the largest merchant acquirer?

The largest merchant acquirers are companies like Chase, Fiserv, Global Payments, and Worldpay. They process millions of transactions daily for businesses worldwide, both in-store and online. While it’s tough to say who’s the absolute largest, these names are consistently at the top due to the volume of businesses they serve and the extensive reach of their payment services.

Why do merchant acquirers exist?

Merchant acquirers exist to make accepting credit and debit card payments possible for businesses. Without acquirers, it would be hard for merchants to process card payments efficiently and securely. Acquirers connect businesses to card networks, handle the flow of funds, and provide support for handling disputes, fraud, and chargebacks. In short, acquirers make card payments easy, safe, and reliable for both merchants and customers, allowing businesses to focus on what they do best.