How long does it take to process a credit card transaction?

Accepting credit card payments may feel instantaneous at the point of sale, but behind the scenes, there’s a bit more going on. Once a transaction is approved, it typically enters a clearing and settlement process that can take 1 to 3 business days to fully process. This means the money doesn’t land in the business’s bank account right away which can cause some cash flow headaches, especially for small and mid-sized businesses trying to cover payroll, order inventory, or manage day-to-day operations.

To bridge this gap, many payment processors offer faster funding options to help merchants access their money sooner. These options generally fall into three categories: Next Day Funding, Same Day Funding, and Instant Funding. While the end goal is the same—faster access to funds—each method works a little differently.

Types of faster credit card funding options

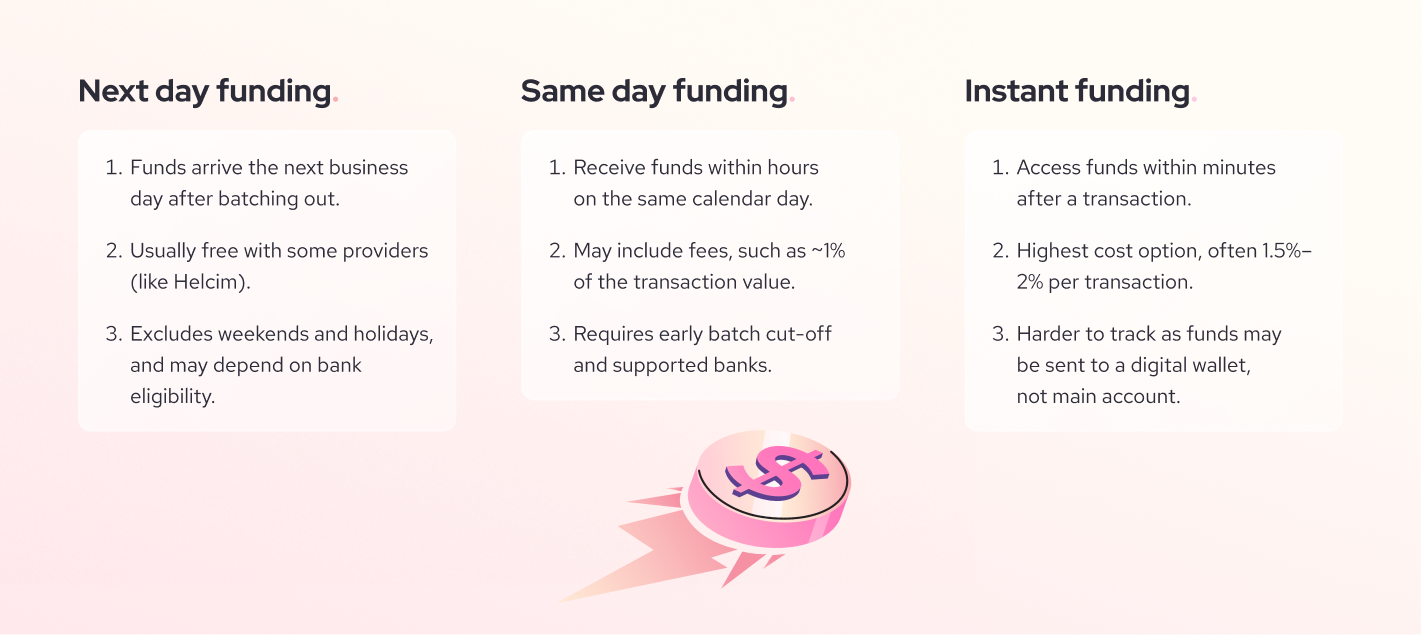

1.) Next day funding credit card processing

Next day funding credit card processing (also known as next day funding merchant services) is when a business receives its card transaction deposits on the next business day after a batch is closed. This funding option strikes a balance between speed and cost. While not as fast as same-day or instant options, it’s still significantly quicker than standard processing timelines.

The cost: Some providers like Helcim offer next day credit card funding free of charge to their merchants, while others may charge a premium or reserve it for high-volume merchants.

The disadvantages:

- Not all processors offer this for free. Some reserve it for high-volume merchants or charge extra.

- Eligibility may depend on the payment network your processor uses. If your bank isn’t part of that network, faster funding won’t apply.

- Often limited to weekdays, excluding weekends and holidays.

2.) Same day funding credit card processing

Same day funding means businesses receive their funds on the same calendar day they process the transactions—often within hours of batching out.

The cost: This level of speed may often come at a cost. Many processors charge a flat fee per deposit or a percentage of the transaction total (often around 1%).

The disadvantages:

- This service sometimes comes at a cost.

- Only available if you close your batch early enough to meet processor cut-off times.

- Not all banks support same day deposits.

- Often limited to weekdays, excluding weekends and holidays.

3.) Instant funding credit card processing?

Instant funding is exactly what it sounds like: immediate access to your card transaction revenue, sometimes within minutes of a sale.

The cost: This is typically the most expensive option, with fees ranging from 1.5% to 2% per transaction, or flat fees per transfer. It adds up fast, especially for high-volume businesses.

The disadvantages:

- It's typically the most expensive option, with fees ranging from 1.5% to 2% on top of processing fees.

- Daily or transaction limits may apply.

- Some processors may send your funds to debit cards or digital wallets, not your main bank account so your funds can end up in different places, making it harder to track what you earned.

Which faster credit card funding option should you choose?

Choosing the right funding speed depends on how often your business needs access to funds and how much you're willing to pay for that speed.

- Instant funding is great for emergency cash flow needs, but costly in the long run.

- Same-day funding can strike a good balance if you're okay with occasional fees and can meet the daily cut-off time for batch closures.

- Next-day funding offers the best mix of convenience, reliability, and affordability—especially if it’s free.

If you find yourself constantly waiting for deposits to cover expenses or to make timely business decisions, next-day funding is likely the best long-term option.

What factors affect credit card payment processing time?

Even with the right funding option, your deposits might not arrive as quickly as expected. That’s because the backend of your payment setup plays a significant role in when your funds hit your account. Here are the three most common influencing factors:

Merchant account type: Some merchant accounts offer faster settlement times depending on your provider, business type, or risk profile. For example, a high-risk merchant account might have longer hold times or reserve requirements, delaying your access to funds.

Payment processing system: The technology your business uses—whether it's integrated software, a standalone terminal, or a cloud-based system—affects how quickly transactions are authorized and passed along for settlement. Modern cloud-based systems may send batches in real time or on demand, while older systems may delay transmission until manual intervention.

Batch processing schedule: Transactions are typically grouped into batches that are submitted for settlement at the end of the business day. If you delay batching out (or forget to do it), your deposit will be pushed to the next business cycle. For instance, if you batch out after the processor’s daily cut-off time (often around 5–6 PM), your “next-day” funding may actually be delayed by an additional day.

Your transaction type can also impact timing. For example, processing online payments may have different flows compared to in-person payments.

Receive credit card payments faster for free with Helcim Faster Deposits

Many payment processors offer faster deposits, but few do it without extra fees.

With Helcim’s Faster Deposits, merchants can receive next-business-day access to their credit and debit card transactions at no additional cost. There’s no setup, no hidden charges — just faster cash flow to help keep your business running smoothly.

As long as your bank is supported through the Interac e-transfer (in Canada), and RTP network and FedNow service (in the U.S.) and very soon the Interac Instant network, Faster Deposits will automatically kick in after your first few batches are processed.

It’s one less thing to worry about, and one more way Helcim helps small businesses thrive.

FAQs

1.) Are credit card payments processed immediately?

They’re authorized immediately at the point of sale, but the actual transfer of funds to your bank account usually takes 1–3 business days without a faster funding option.

2.) Why do banks take so long to process credit card payments?

Credit card payments involve several parties—like the merchant, payment processor, acquiring bank, and issuing bank. And each step in the process, from authorization to clearing and settlement, takes time to complete especially when real-time payment systems aren’t being used.

3.) Do credit card payments process on weekends and holidays?

No. Most processors and banks operate on business days, so transactions processed on weekends or holidays typically begin processing on the next business day.