The way your funds are deposited by payment processors can significantly impact how you track revenue, manage cash flow, and plan for future expenses. Understanding the difference between net deposits and gross deposits is key to making the best financial decisions for your business. Let's explore how each funding option can shape your approach to managing your money.

What are gross deposits?

Gross deposits (also known as gross funding) are the total amount your payment processor deposits into your bank account before any fees are deducted. Processing fees are deducted separately in a different transaction. For example, if you’ve made $1,000 in credit card sales, that full $1,000 appears as a gross deposit in your account.

Gross deposit advantage: Gross deposit allows you to see the total sales amount, keeping your revenue separate from processing fees. As a result, it makes accounting simpler by providing a clear record of your sales figures.

Gross deposit disadvantage: However, the downside is that fees are deducted later, which means you need to track these deductions separately to accurately manage your cash flow. Some processors like Helcim take out these fees at the end of the day, while others do it at the end of the month. If your processor deducts fees daily, you'll see two transactions: one for the full sales amount and another for the fee deduction.

Who can benefit from gross deposits?

Gross deposits are perfect for merchants who prefer tracking the total sales amount, keeping the revenue separate from payment processing fees. For example:

Retail businesses: Seeing the total sales amount before any fees are deducted makes sales reporting and forecasting easier and more accurate, especially for holidays or shopping seasons.

Real estate agencies: Real estate agencies handling large transactions, such as property sales, can use gross deposits to track the total transaction value and accurately calculate commission for agents.

Event organizers: Gross deposits offer a clear view of total ticket sales. It provides transparency for stakeholders, sponsors, and partners by showing the complete revenue before any fees are deducted. This transparency helps build trust and ensures that everyone involved has a clear understanding of the event's performance.

What are net deposits?

Net deposits (also known as net funding) are the amount of money that gets deposited into your bank account after all processing fees have been deducted. For example, if you made $1,000 in credit card sales for the day, and your payment processor charges a 3% fee, you’d see $970 as your net deposit in your account.

Net deposit advantage: Since processing fees are deducted before the funds reach your account, you can easily track your actual cash inflow and budget more accurately.

Net deposit disadvantage: A downside of net deposits is that you don't see the full sales amount in your account. This means you have to manually add back the processing fees to calculate your total sales. This can lead to manual errors when trying to reconcile sales figures with deposits.

Who can benefit from net deposits?

Net deposits are particularly useful for businesses that need to understand their true cash flow after accounting for payment processing fees.

Automotive shops: Imagine you're running a busy shop. With net deposits, you know exactly what you have on hand at any given time to manage expenses, such as ordering parts, stocking up on tires, or covering payroll and utilities.

Service professionals: Whether you’re a freelancer, consultant, or lawyer, net deposits give you a clear view of your earnings after fees. For example, lawyers often handle multiple accounts, like client trust accounts and operating accounts. Net deposits help them see exactly how much money is available for their client and practice’s needs after all fees are deducted.

Non-profits: For nonprofits, every dollar counts. By using net deposits, organizations can know exactly how much is available for their programs and can plan their initiatives with confidence.

Overall, the net deposit is your actual take-home amount after processing fees. This method gives you a clearer picture of what you’re earning because it factors in the costs of using a payment processor upfront.

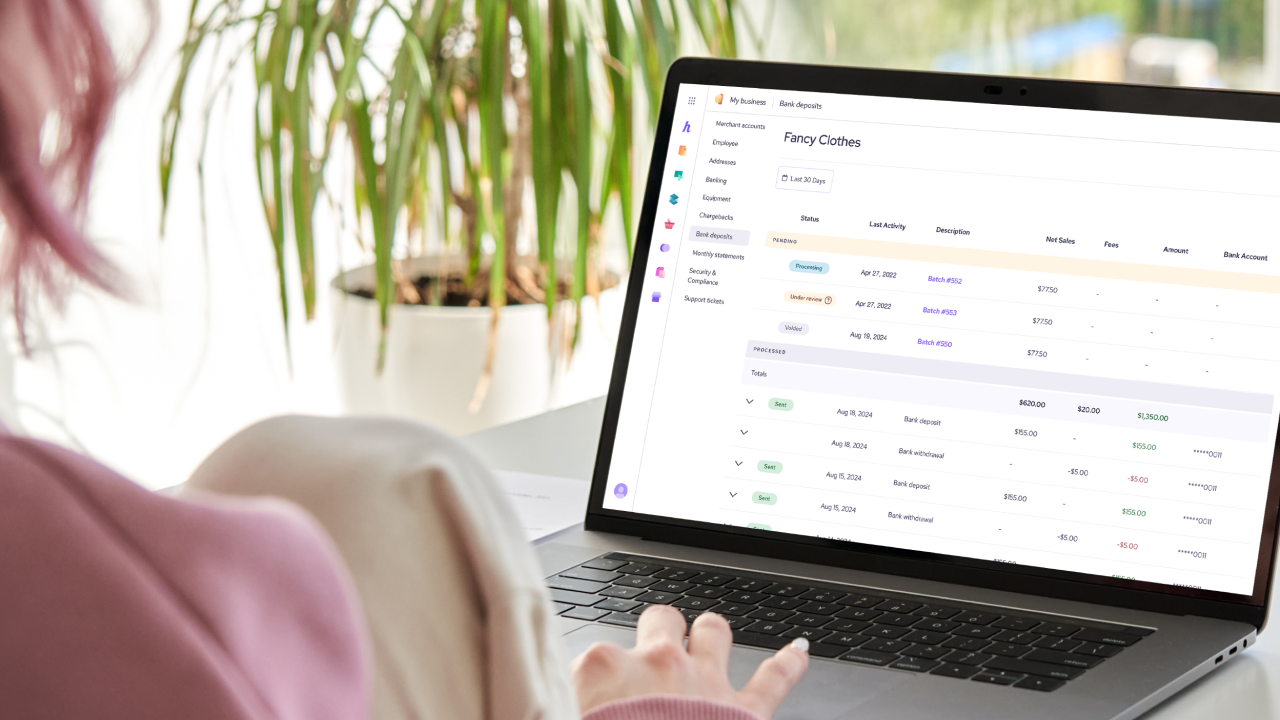

Get the best of both worlds with Helcim Gross Deposits

Helcim’s gross deposits make it easy to track your revenue and cash flow.

With Helcim’s gross deposits, you receive the full amount of your sales each day. By deducting fees daily instead of at the end of the month, you also get accurate cash inflow figures each day. As a result, you always know exactly how much cash you have on hand to manage your stock reorders, and other operating expenses.

Helcim also offers low processing fees. On average, Helcim merchants save 25% on processing fees compared to other popular processors like Square, Clover, Moneris, and PayPal.

If you’re interested in finding out how much you could save with Helcim, click here to get your estimated savings.

Don’t have a payment processor yet? Sign up with Helcim now for low processing fees, flexible funding options, and free payment tools—all with no monthly fees, hidden charges, or contracts required.