If you have been accepting payments and are wondering why it sometimes feels like your money is taking the scenic route before finally arriving in your account, you’re definitely not alone. Understanding how payment processing works and the timelines involved are key to keeping your cash flow steady. The truth is, not all payment methods move at the same speed—credit card transactions and ACH transfers each have their own pace. So, let’s dive into how long each method takes and what factors can speed up—or slow down—the journey, so you can plan ahead.

What is payment processing time? (and why does it feel longer for some payment methods)

Payment processing time is the stretch of time between when a transaction kicks off and when the funds finally make it to your account. There are different funding options for credit card payments like next day, same day, and instant funding. Payment processing time can vary significantly, influenced by the type of payment method and several other factors we’ll explore below.

For instance, credit card payments generally arrive faster since they’re approved almost instantly through digital networks. Other methods, like ACH transfers, can take longer as they go through additional verification steps and are processed in batches. Each “pit stop” along the way, from security checks to bank approvals, can add a bit more time to the journey.

Why payment processing time is essential for both businesses and customers

- For businesses, timely payment processing and funding ensures that they receive their money promptly, enabling them to manage their cash flow, pay bills, and invest in growth opportunities.

- For customers, on the other hand, fast payment processing and settlement means that their transactions are handled quickly and securely, minimizing the chances of declined payments, overdraft fees, and potential credit score impacts.

Common factors that affect payment processing times

Now that we’ve covered the basics, let’s explore the key factors that can influence how quickly you receive funds from your transactions:

1. Payment method

The type of payment method plays a significant role in determining the speed of processing. For example, processing online payments, such as credit card transactions, is faster than traditional methods like paper checks. A mailed payment, such as a paper check, can face delays since it relies on postal delivery and manual processing by the receiving bank, whereas online payments are typically posted as soon as they are approved. ACH payments, or Automated Clearing House transfers, fall somewhere in between paper checks and credit card transactions in terms of processing speed. Unlike credit card payments, ACH transfer transaction don’t happen instantly—they’re typically processed in batches, often taking 1-3 business days to clear.

2. Business type

High-risk industries, such as crowdfunding, tobacco, or medical and drugs, may face longer processing times due to additional compliance checks. These additional checks are necessary to reduce the risks of fraud and chargebacks commonly associated with these industries.

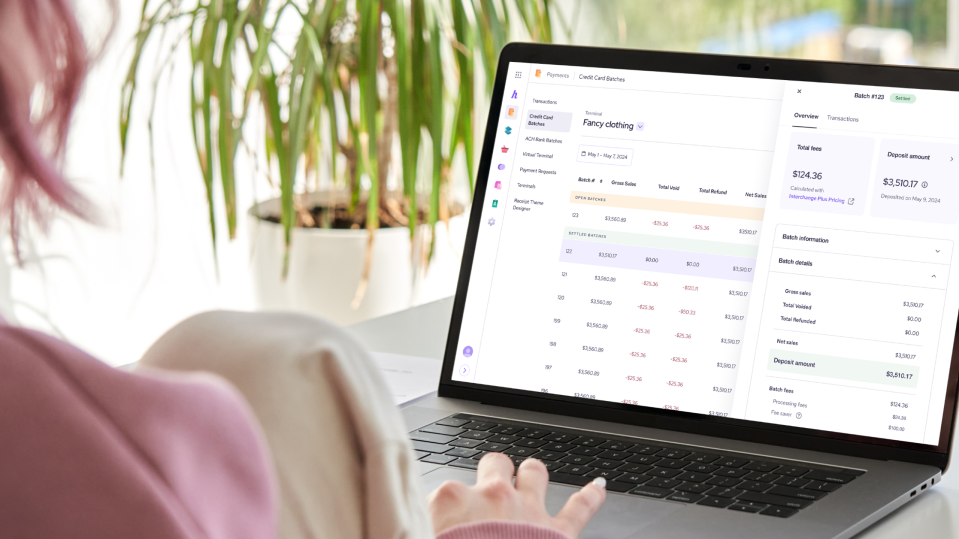

3. Payment processors

Different payment processors have varying timelines for settling funds, so it's crucial to choose one that aligns with your business needs. While some processors provide same-day or next-day deposits—often for an additional fee—this option can be ideal for businesses needing quick access to funds. However, be aware that some processors are sensitive to sudden spikes in transaction volume and may temporarily hold funds to verify the legitimacy of the transactions.

4. Bank holidays

Payment processors typically settle transactions only on business days. As a result, settlements can be delayed if a transaction falls near a weekend or a bank holiday. For example, if a transaction is processed on a Friday, the funds will likely be available by Tuesday at the earliest, as they will be batched with other transactions from the weekend.

5. Monthly volume

The monthly volume of transactions your business typically processes can affect how your payments are handled. If a business suddenly processes a higher volume of transactions than usual, exceeding the declared monthly volume, it can trigger an account review by the payment processor. This review helps ensure that the increase isn't due to fraudulent activity or other risks. During the review, funding times might be temporarily delayed while the processor assesses the situation. Maintaining a consistent volume or updating your processor if you anticipate a spike can help avoid these delays

6. Credit card issuer

The customer’s credit card issuer, a financial institution that provides credit cards to consumers, plays a role in the transaction timeline. They verify the customer’s credit card information and ensure sufficient funds, which can affect how quickly a payment is approved and processed. While this typically happens quickly, delays may occur if additional checks are needed. Now that you understand what influences your processing time, let’s dive into how each payment method differs when it comes to settlement timelines.

Credit card processing time: Faster, but not instant

When a customer pays using a credit card, the funds don’t immediately appear in your business account. Here’s a breakdown of how the credit card processing works:

1. Authorization

This is the initial stage where the cardholder's bank approves or declines the transaction. It typically happens in seconds.

2. Settlement

After authorization, the transaction needs to be settled, which usually takes 1-2 business days. During this stage, the funds are moved from the cardholder’s account to the merchant’s account.

3. Funding Transfer

Finally, the payment processor transfers the funds into your business account. This process can take another 1-2 business days, depending on your payment processor and your monthly volume.

In short, credit card funding time usually ranges from 1 to 4 business days, but some processors might offer faster like next-day or same-day funding options for a fee. Learn how to speed up credit card processing time here.

ACH payment processing time: Slower, but budget-friendly

ACH (Automated Clearing House) payments are a popular choice for businesses because of their lower processing costs, but the funds tend to take longer to reach your account than credit card payments. Here's how it works:

1. Pre-authorization

This is the initial step where the payer’s bank verifies that the payment request is legitimate and that there are sufficient funds to cover it. Think of it as a quick "thumbs up" before the real work begins.

2. Initiation

Once the ACH payment is initiated and authorized, it takes about 1 business day for the request to be submitted to the ACH network. This stage is like putting your payment request in line for processing.

3. Clearing

Next, the ACH network processes the request, which typically takes 1-2 business days. During this phase, the payment moves through the system, getting approved and verified by banks on both sides.

4. Settlement

The final stage is settlement, where the funds are transferred to your account. Depending on whether it's an ACH debit or credit, this can take another 1-2 business days for the money to actually land in your account. In total, ACH processing generally takes 3-5 business days. New businesses might experience slightly longer times initially due to risk assessments by banks and payment processors.

Want to learn more about the ins and outs of ACH payments? Check out our detailed guide below, complete with templates for notifying customers about processing timelines.

Other payment methods and their processing times

While credit card and ACH payments are common, businesses can also use other payment methods. Each comes with its own processing times, advantages, and considerations. Here’s a quick overview to help you understand the options:

Debit card payments

Debit card payments let customers use their debit cards for purchases, with funds drawn directly from their bank account. It's convenient for customers looking to avoid credit and typically settles within 24 hours, making it one of the faster options. However, it may be subject to lower transaction limits.

Peer-to-Peer (P2P) payments

P2P payments allow direct transfers between bank accounts or through apps like Venmo and PayPal. The processing is instantaneous within the P2P network but might take 1-3 days when transferring funds to a third-party bank account. It's speedy and simple for person-to-person transfers but it's not always designed for business transactions.

Contactless payments

Contactless payments are convenient as it's done by tapping a credit or debit card, or using a smartphone or wearable device, on a contactless-enabled terminal. The processing time is similar to credit card payments, usually taking 1-3 business days. However it typically has lower transaction limits versus the traditional chip and PIN.

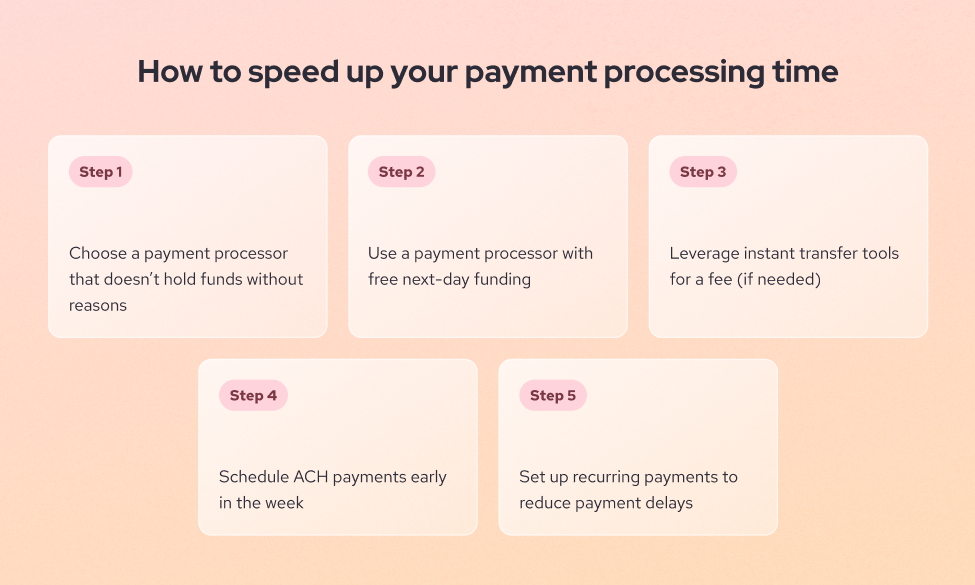

How to speed up your payment processing time

You might be thinking, “I don’t want to wait 3-5 days for my payments!” If that sounds like you, here are some strategies to speed things up:

1. Choose a payment processor that doesn’t hold funds unnecessarily

Look for a payment processor with transparent policies that won’t hold your funds or delay payments without reason. This ensures a smoother cash flow and fewer surprises. Pro tip: Unlike many other providers, Helcim offers small businesses their own individual merchant accounts, making fund holds far less likely.

2. Use a payment processor with next-day funding

Some payment processors offer next-day funding for credit card transactions, allowing you to receive funds faster.

3. Leverage instant transfer tools

Some providers offer instant payouts for a fee, giving you quicker access to funds when needed.

4. Schedule ACH payments early in the week

Since ACH payments don’t process on weekends, starting them on Monday or Tuesday helps avoid delays.

5. Set up recurring payments

Automating regular customer payments ensures consistency and reduces delays, improving cash flow predictability.

Wrap up: Get paid faster and smarter

For small businesses, understanding the ins and outs of payment settlements and their timelines is crucial. By choosing the right payment methods, optimizing your processing setup, and knowing when to expect funds, you can minimize delays and get paid faster. This helps you plan better, manage cash flow efficiently, and deliver a seamless experience for your customers.

Ready to take control of your payment process?

At Helcim, we offer more than just affordable processing cost —we provide transparent funding, fast deposits, and exceptional support. With features like ACH payments and automated recurring payments, Helcim makes it easier to get your money faster and keep your business growing. Learn more about how Helcim can fit your needs, or get started for free today.

FAQs:

What is the fastest payment method for small businesses?

If you don’t want to handle cash, credit or debit card payments will be the fastest payment method (versus ACH payments or paper checks), typically taking 1-3 business days to settle.

Why do ACH payments take longer to process?

ACH payments go through a clearinghouse system, which involves multiple banks and can take 3-5 business days for funds to be transferred.

Can my monthly volume affect my payment processing time?

Absolutely. If your business experiences a sudden spike in transaction volume, it might trigger additional fraud checks, which could delay your payments. However, some payment processors offer perks for businesses with consistent high volumes, ensuring smoother processing once they’ve verified your transactions are legitimate.

Does processing mean payment went through?

Not necessarily. "Processing" means the payment request has been received and is being handled, but it doesn’t guarantee that the payment has been completed yet. The funds may not be available until the payment status changes to "Completed" or "Settled."

How long can a company take to process a payment?

Payment processing times can vary depending on the payment method and the company’s policies. Typically, it can range from a few minutes for online payments to several days for ACH transfers or paper checks.

How long does it take once a payment is processed?

After a payment is processed, the funds are usually transferred to your account within 1-3 business days for credit card payments or 3-5 business days for ACH payments.

Why is my payment still pending?

Payments may remain in a pending status due to factors like bank holidays, weekends, or additional verification steps required by your bank or payment processor.

Can I cancel a payment while it’s processing?

It depends on the type of payment. Some payments, like ACH transfers, can be canceled if they are still in a pending status. However, once the payment is marked as "Processed" or "Completed," it’s usually too late to cancel.

Why do ACH transfers take longer than other payments?

ACH transfers involve multiple banks and a clearinghouse, which can extend the time it takes for the transaction to complete. This process includes verification and settlement, contributing to a longer timeline compared to instant payments.

Are there fees for faster payment processing?

Yes, some payment processors offer expedited services, like next-day funding, for an additional fee. This option can be helpful if you need quicker access to your funds.

What should I do if my ACH transfer is delayed?

If an ACH transfer is taking longer than expected, reach out to your bank or payment processor for more details. Sometimes, delays can occur due to risk reviews, incorrect account details, or system outages.

What happens if an ACH transfer fails?

If an ACH transfer fails, you’ll usually be notified by your bank or payment processor. Reasons for failure can include insufficient funds, incorrect account details, or the receiving bank rejecting the transfer.