Free credit card processing once seemed like an impossible dream for small business owners. With the arrival of surcharging, that dream has become a reality.

Small business owners can pass credit card fees on to their customers by way of a surcharge fee, offsetting the costs to their business. Although there are still some strict regulations, the process is quite simple.

Let’s explore the steps to get your business started with surcharging so you can start processing credit cards for free.

Step 1: Understand what a credit card surcharge is

It’s important we get on the same page of what a surcharge is. Basically, as a merchant, you have the option to pass a fee to your customers when they choose to pay by credit card. That additional cost is your surcharge fee.

To break it down even further, there are two different types of surcharges you can apply:

Brand surcharge: This is where surcharging is applied to all cards of a particular brand, such as Visa. This is an easy blanket way to cover all credit card payments from a particular brand, or extend it to all credit card brands. One exception is American Express. They do not allow you to implement a brand surcharge targeting only their cards.

Product surcharge: This is where surcharging is applied to specific card types within a brand, like TD® Aeroplan® Visa Infinite Card. This is a great way to target high fee cards only.

No matter which of the two you choose, a surcharge is meant to help you cover the cost of credit card processing by shifting the burden from your business to the customer. It may not be the best fit for every business, but it’s an option you have in your toolkit to help your business save money.

Side note: People tend to confuse convenience fees and service fees with surcharges. Although they are similar, they have different rules altogether. So let’s clear the air with some simple definitions:

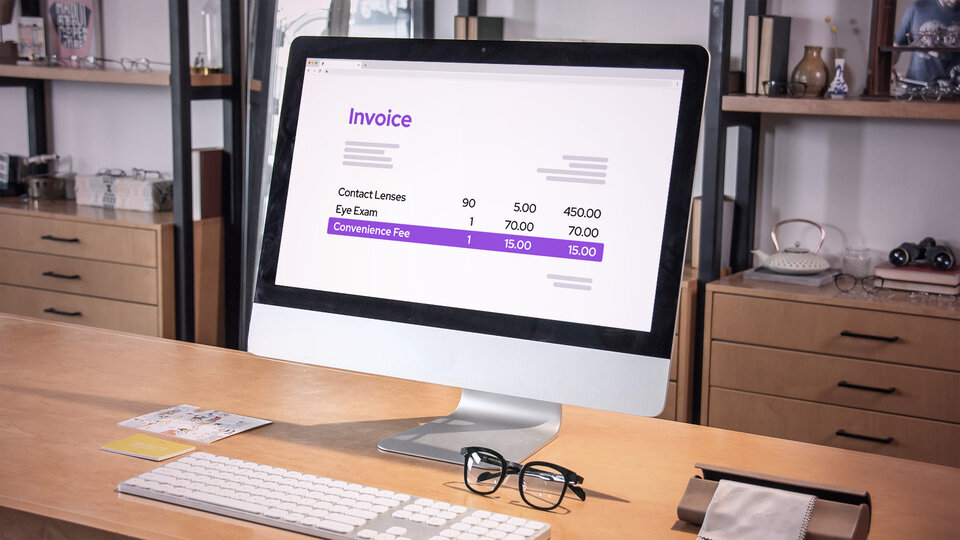

A convenience fee is an extra fee charged by a business when the customer chooses to use a payment method different from the typical method accepted by the business. For example, you run an accounting firm that prefers to be paid by ACH, but the customer insists on paying by credit card — so you charge them a convenience fee of 3%.

A service fee is a fee collected to pay for services that relate to a product or service that is being purchased. For example, you run a restaurant and decide to charge an automatic 18% gratuity for parties of 10 or more people. This gratuity is considered a service fee as you are adding an additional fee to cover the service provided.

Step 2: Check if your business is eligible to surcharge

Now that you have an understanding of surcharging, you’re probably eager to jump into it and start saving money. Before you do that, it is critical that you check your eligibility. Not every province and state in North America is treated equally. Both Canada and the United States restrict surcharging in certain regions.

Canada All Canadian provinces and territories are eligible for surcharging, with one exception: Quebec. The province of Quebec has consumer protection laws that prohibit merchants from applying a surcharge to purchases.

United States In the United States, surcharging is legal across most of the country. But there are a few areas where it is deemed illegal:

- Connecticut

- Maine

- Massachusetts

- Oklahoma

- Puerto Rico

If your business is in one of these areas, sadly you won't be able to surcharge.

Step 3: Notify the card networks

Assuming you’re eligible, it’s time to let the card networks know you intend to surcharge. Visa, American Express, and Discover are more relaxed and don’t require any notice. But Mastercard requires a minimum 30 day notice of your intention to start surcharging.

Luckily, Mastercard makes it simple with a form to fill out for the US and Canada. It asks for simple details like contact and business information. The one part you may get hung up on is the “Type of Surcharge” — brand or product. Just refer back to Step 1 for their definitions.

Step 4: Notify your acquirer or payment processor

Sorry to say, you're not done notifying people yet. Your acquirer or payment processor (whoever you use to accept credit card payments) also wants 30 days notice of your intent to surcharge. You can typically do this by phone or email, just make sure to save the email and its confirmation when applicable.

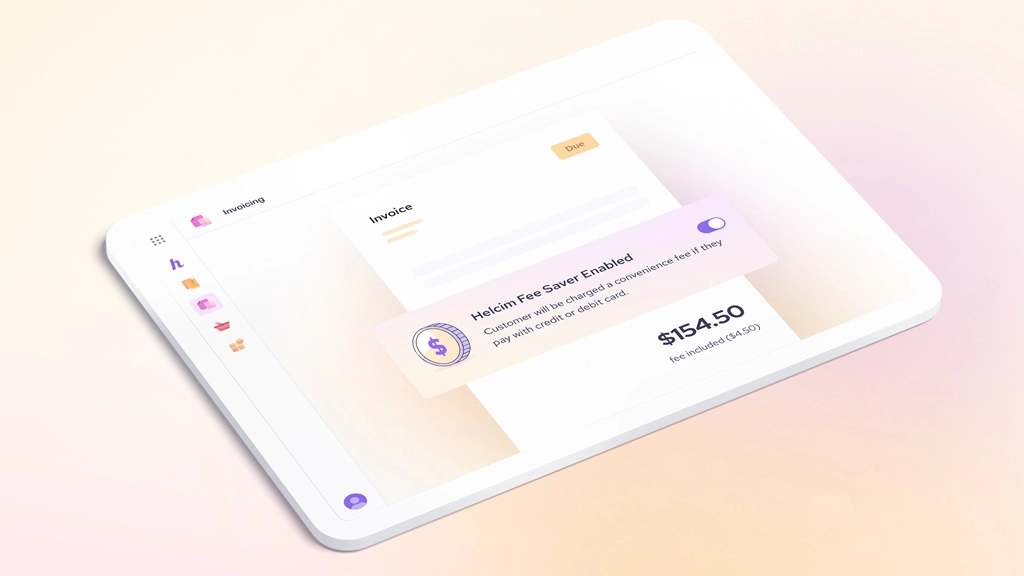

Quick tip: Our Helcim Fee Saver feature makes this process super simple. You just flip on a toggle and we get notified of your intent.

Step 5: Determine how much you want to surcharge

Now that you’ve notified all the big credit card folks, you can put a plan in place for how much you want to surcharge. You are essentially free to set your own rate as long as it’s below a maximum of 2.4% in Canada and 3% in the US, and the fee does not exceed the total cost for your business to accept the payment.

It is important to note that there can be nuances from region to region, so it is always vital for you to check your local rules and regulations before imposing any sort of surcharge fee.

Quick tip: With Helcim Fee Saver, we automatically apply a surcharge rate based on your location to ensure your rates are within the allowable limits for your region.

Step 6: Implement your credit card surcharge

With your rates determined, you can now start implementing it on your payment system. Most modern point-of-sale (POS) systems and payment processors have a feature that makes this easy to do. If you check with your payment provider and it's not supported, it may be time to switch.

Quick tip: Helcim’s Fee Saver feature makes this process incredibly simple. You flip on a toggle and get access to our fully compliant credit card surcharge feature.

Step 7: Set up proper surcharge disclosures

In order to comply with surcharging rules, you must clearly disclose to your customers that you are imposing the additional fee, both before they pay and on their receipt after. That means you need to at least do the following:

- Display the surcharge fee through in-store signage at your point-of-sale

- Show the surcharge fee on your online store before purchase

- List the surcharge fee as a line item on the customer’s receipt

If your business is in the state of New York, you are required to display the total price, including any credit card surcharges, before the customer completes their checkout. You have the option to either show a single total price with the credit card surcharge, or display a distinct cash price vs credit card price.

Always make sure to double check your local rules and regulations as they can change. It is important to do your full due diligence in your own local region when it comes to disclosure.

Step 8: Notify your existing customers

Although not mandatory, transparency is always appreciated by the people loyal to your business. If you have customers or clients that frequent your business, you can notify them with an email about your new surcharging policy. It helps to explain why you are doing it, the new rate they can expect, the effective date, and recommend alternative methods of payments to avoid the surcharge fee.

By going the transparent route and notifying your customers, you will likely receive questions. Here is some material to help you prepare:

Why am I being charged for paying by credit card?

Credit card alternatives such as ACH, EFT, debit card, or cash are our preferred method of payment because it saves you and our business the transaction fees. However, for your convenience, we offer the option to pay by credit card for a fixed fee.

What if I don’t want to pay the fee?

If you prefer not to pay the fixed fee for using your credit card, you may use other payment methods such as cash, debit card, or ACH/EFT payments.

Start surcharging and passing your fees with Helcim

Helcim Fee Saver is one of the simplest ways to get your business up and running with surcharging. With the flip of a toggle you get access to our fully compliant surcharging feature on our Smart Terminal. When you accept in-person payments and your customers choose to pay with credit cards, Fee Saver adds a surcharge fee to the final bill to offset the credit card fees for you.

If your business does online sales, Helcim Fee Saver will add a convenience fee, instead of a surcharge, when customers choose to pay by credit card over ACH payment. This feature is available on our online invoices, payment webpages, and embedded payment modals.

If you’re ready to dive into the world of free credit card processing, get started with Helcim here.

FAQ

What are my obligations for surcharging?

You are obligated to stay up to date with your local rules and regulations for surcharging so that you remain compliant. That includes knowing whether it is legal in your region, notifying the proper institutions, knowing the allowable rates, and displaying the proper disclosures for your customers.

How do I notify customers of a surcharge?

Customers need to be informed of the surcharge before they complete the transaction. That means in-store signage, verbal communication, and listing any surcharges on your online store. Once the purchase is complete, the receipt or invoice must include a separate line item displaying the surcharge fee.

Can I add surcharging to my online payments?

Yes. Surcharging can be applied to both online and in-person payments. If you are using Helcim Fee Saver, online payments will use a convenience fee instead of a surcharge, but both will give you access to no cost credit card processing.

Can convenience fees and credit card surcharges be applied together?

No. There are strict rules stating that you can only use one or the other. You are not allowed to combine the two.