Changes to Canadian Interchange Rates

Interchange fees can be complicated to read- there are rows and rows and pages and pages of fee structures, merchant codes, and rates to sift through but only a few are usually relevant to small and medium sized businesses. So while you can find the rates posted on our site, we’ve created a shorter guide in this article which outlines changes to interchange rates that are most relevant to our Canadian merchants.

This article covers the changes to interchange rates for major card brands like Visa®, Mastercard®, Discover®, and American Express® since last April of 2022, when the last changes were announced.

What are interchange rates?

Once you understand how interchange fees work and [how they are determined,](and that each card brand network has their own set of interchange fees) you can begin to look at how the fees change every April and October and what those changes mean for your business.

Of course, businesses don’t pay flat interchange fees, these are just a component of their processing fees which vary depending on the pricing model of the payment company you work with to accept payments at your business.

While changes to interchange rates won’t be as useful to a business who has a flat rate pricing model, for example, it can be an opportunity for businesses who use interchange plus pricing to cut costs on their processing by finding and taking advantage of lower rates — or avoiding higher ones.

The rates are set by the card brands and based on factors such as the type of card the consumer is using. For example, high rewards cards tend to be more expensive to accept and other factors like the transaction type, the cost of the transaction, and risk factor will also contribute to the set rate.

So for those who are already taking advantage of interchange plus pricing, let’s dive into the changes to Interchange rates and how it may impact your payment processing costs.

New programs and changes this October of 2022

Visa®

For Visa® interchange rates in Canada, the rates that are changing are as follows:

- NEW VISA® Non-Chip Transaction Integrity Fee

- NEW Visa® B2B Virtual Program

- NEW VISA® Settlement fee for non-domestic currency transactions

- NEW VISA® Large ticket program for commercial transactions

- CHANGES VISA® B2B Virtual Payments Program Changes

Mastercard®

For Mastercard® interchange rates in Canada, the rates that are changing are as follows:

- Updates to the “Interregional Consumer Interchange Program”

- Changes to the Transaction Processing Excellence (TPE) program

American Express® OptBlue

For AMEX® OptBlue interchange rates in Canada, the rates that are changing are as follows:

- Some MCC codes will be moved to new industry categories

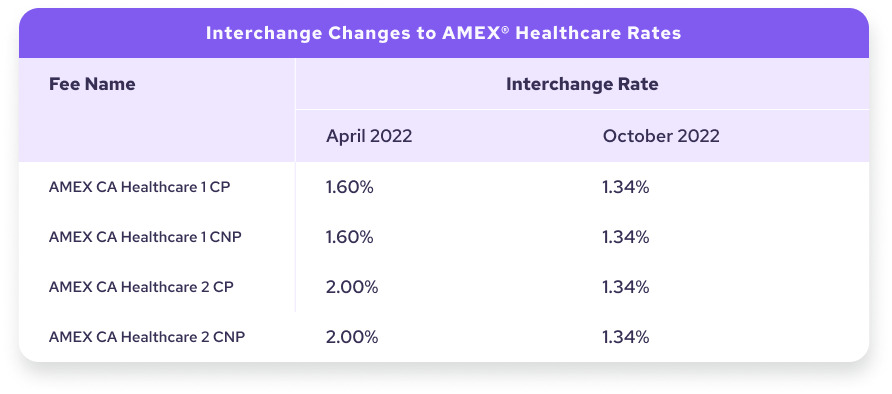

- Changes to Healthcare rates

- Foreign-issued discount rate will now extend to all industry categories

Interac ®

For Interac® interchange rates in Canada, the rates that are changing are as follows:

- Interac® Flash transactions will be adjusting their pricing structure and adding new tiers.

American Express® OptBlue changes

New MCC codes and industry categories mean new industries can take advantage of lower rates. Specifically, the industry category is being replaced, with MCCs shifting as they can only be in 1 category. For the most part the new industry categories have a lower interchange rate compared to the current industry category. As a result merchants with those MCCs should benefit from lower rates.

A few changes to healthcare industry pricing was also observed in the changes this fall. New industry categories include emerging markets, residential rent, and utilities. Finally, all industries qualify for the Foreign-Issued Debit Card Program rates. Changes to AMEX® OptBlue Healthcare Rates

This fall businesses in the healthcare industry may be intrigued to learn about a few changes to the AX Canada Healthcare Tier 1 & 2 rates that saw a 26% and 66% decrease respectively, giving healthcare industries a small break.

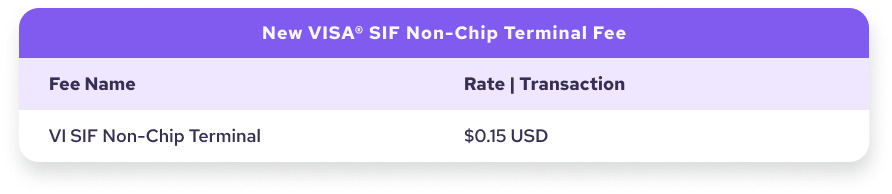

New fees for Visa® non-chip POS transactions

As you probably already know, we’ve been telling our merchants for some time now that Swipe is becoming obsolete. Not only is it a much less secure transaction method than EMV, but now card brands like Visa are cracking down by imposing a non-compliance fee, or System Integrity Fee, starting October 15th, 2022. What does this mean? Your card reader, or point-of-sale (POS) has to be compatible with chip technology to avoid an extra charge on each transaction.

Helcim merchants who process in-person transactions will not be impacted as our Helcim card reader is chip, PIN and NFC enabled.

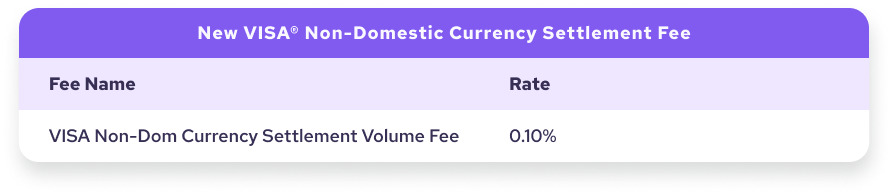

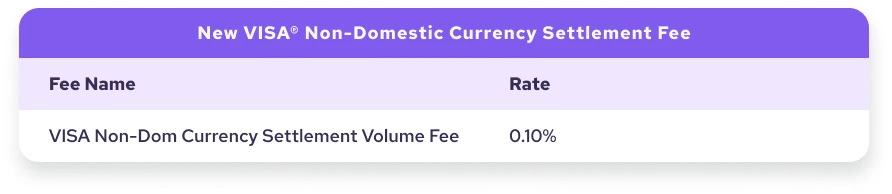

New Non-Domestic Currency Settlement Fee for Visa®

If your business accepts Visa® cards that were issued outside of Canada, meaning the currency for the transaction will settle as another currency other than Canadian, you will be charged a rate of 0.10%.

VISA® B2B Virtual payment New product and rate changes

There are two changes to this program. First, there are new lower rates for this program that could result in lower interchange rates for merchants accepting this new type of corporate card.

Second, Visa is expanding qualifying Merchant category codes so more merchants could potentially benefit from these lower rates. These transactions will have lower rates due to lower security and fraud risk since these cards don’t run the same risks of physical cards such as stolen data or loss and these transactions tend to be PCI compliant by nature.

Merchant category codes being added to this program include

- Local transportation

- Food and alcohol establishments

- Flower shops

- Movie theaters

- Golf courses

- Specific government services

New Visa® Commercial Large Ticket Rates

Unless you’re processing around a quarter millions dollars at any given time then the new Commercial Large Ticket Interchange Program in Canada probably won’t be of interest to your business.

For those who are, however, changes will apply to corporate cards, purchasing cards, fleet cards, and virtual B2B cards.

Although this is a new interchange program this October rates are low for such a large ticket amount indicating businesses processing these large volume transactions are getting a break. Coming in at 1.30% for transactions between $100 and $250 grand and will be reduced to 1% for anything higher than a quarter million. Compare this to a regular corporate rate of 1.9% - 2.0% that could be a 50% savings in processing fees on every transaction.

Mastercard® TPE program changes for declined transactions

These changes will echo earlier changes this October for new U.S rates from both Visa® and Mastercard® in what looks like a crackdown on fraud. What this will mean for Canadian merchants starting November 7th, is that Mastercard® will be capping the amount of authorization attempts a merchant can try from 20 to 10.

After that, merchants will start to accumulate extra charges at 0.40 cents more for every attempt rounding it to half a dollar. Merchants will particularly start to feel the sting if they fall prey to card attacks, prompting a healthy revisiting of card-not-present security practices.

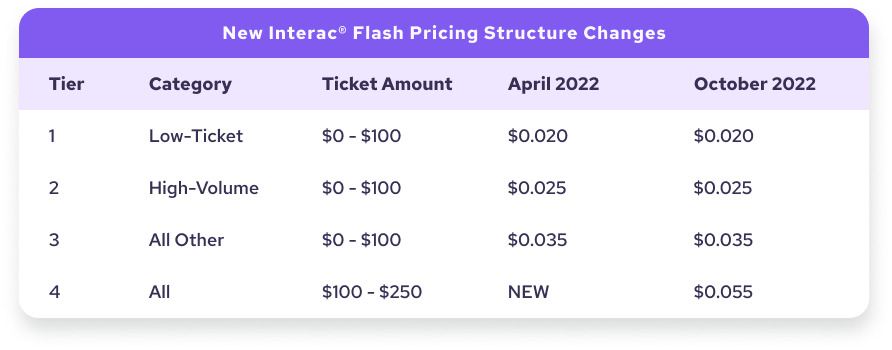

Changes to pricing structure for Interac® Flash Transactions

Interac will be introducing a new pricing structure for various tiers per transaction volume.

For transactions up to $100 for tier 1-3 will not change, however for transactions between $100-$250 a new tier has been created, tier 4. A flat fee of $0.055 will be charged on all those transactions.

The Benefits Of Being A Helcim Merchant

As we said earlier, changes to interchange rates could mean savings for businesses processing with Interchange Plus Pricing. For Helcim merchants that means this fall you get access to lower AMEX OptBlue interchange categories, lower rates on the Visa B2B Virtual payment program and competitively low rates for those large ticket prices.

If you’re not a Helcim merchant, changes to interchange pricing can be a great time to switch since some processors will also change their pricing. One of the tips we mention in our article on how to get out of your merchant contract alludes to the Code of Conduct for the Credit and Debit Card Industry in Canada which allows merchants to cancel their contract within 90 days of the change. So if you are still processing with a flat rate pricing model, you might be able to get out to take advantage of lower rates.

If you are looking for the right pricing model to start accepting debit and credit card payments at your business whether online or in person, our article on pricing models helps to outline different payment processing options out there.