The Concept of Currency

The way we think of currency today is a far cry from where our ancestors started with the concept. As civilizations across the globe evolved, so did the way we pay-but the history of payments is far from linear. The ancient Greeks may have been using coins at the same time Northern Europeans used a barter system. Similarly, coinage was absent among Indigenous populations until the arrival of Europeans, who almost exclusively used coins back home.

Trade as we understand it today is predicated on two main ideas: value and convenience. Trade has always been based on value (e.g. how a basket of vegetables might be equal in value to a certain amount of grain), and currency (though also based on value) was born out of an effort to make trade more convenient.

Think about it. That's why we use coins or paper. A thousand years ago, it was a lot easier (it still is!) to bring a couple of coins to the market than to carry an armful of vegetables or a cart full of wool to trade for some meat.

The Barter System

Before the money we are familiar with existed, people considered their wealth in terms of possessions. This could be in the form of livestock, land, or other physical goods.

The primary goal of life on earth has always been survival, so it should be no surprise that the things people owned (fields of grain, sheep, etc.) were instrumental in helping them preserve their lives. Only later, when humans either found they had extra, or found themselves without something they needed or wanted, would trade become necessary.

For example, I've got too many extra goats: perhaps I can trade a couple for some wine or vegetables. Different civilizations assigned different values to these items, and over time, a person might begin to focus on the production of a single type of good that was valuable for trade, and use it to acquire the necessities of life, rather than try to produce everything you need to live all on your own.

Gold and Silver

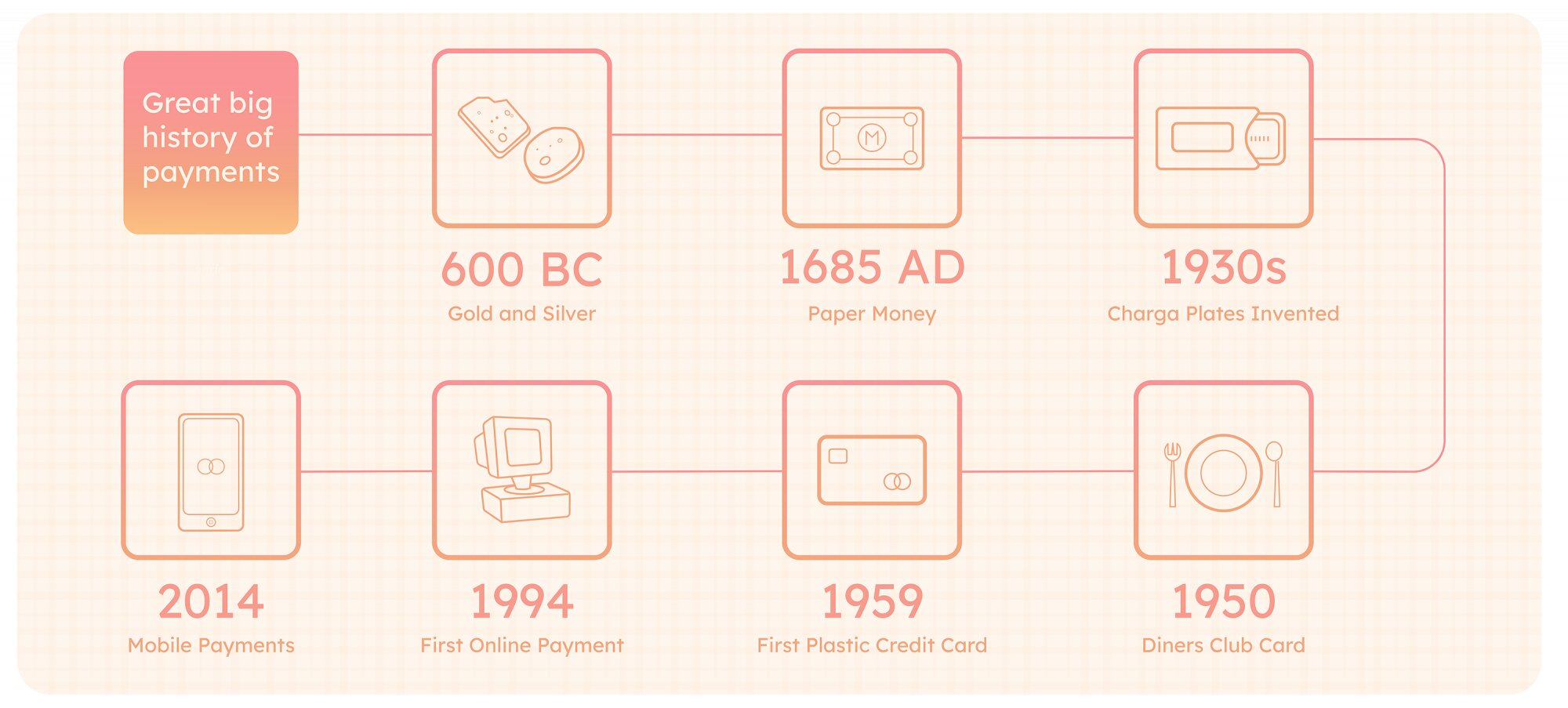

The Lydian Empire, spanning across modern day Turkey, was the first to use gold and silver coins. Croesus, the last king of Lydia, was the first monarch to mint purely gold coins.

After Croesus' defeat at the hands of Cyrus the Great of Persia, the Persian Empire began using gold coins as their primary currency. The Greek city-states were minting their own coins around the same time, and as the Greeks & Persians battled for territory in the following centuries, their respective coinage went with them wherever they conquered.

The Roman Republic started minting coins around the third century BC, and would achieve dominance in the Mediterranean by the first century BC, supplanting the Greeks and Persians as the dominant superpower in the region. The Romans would subsequently take their conquests far away from their home shores, and ultimately introduce coinage to Northern Europe.

Gold and silver coins would go on to be used by every major European power, and were carried to the Americas when Europeans began taking voyages there in the late fifteenth century.

Paper Money It is actually due to the exploratory voyages of Europeans in the fifteenth century and onwards that we owe the widespread adoption of paper currency. The first known record of paper money outside of ancient China is found in 1685 AD, and was in the form of an IOU. Because the transfer of silver, gold, and other supplies from Europe to America could take months, authorities began to issue paper documents which would guarantee some form of monetary compensation for the holder of these papers.

This eventually led to banks and governments issuing "banknotes" which could be redeemed (according to the face value of the note) for its equivalent in gold and silver. The only key difference between this form of currency and ours today, is that ours is no longer backed by (and can not be redeemed for) precious metals.

The Credit Card

After the widespread implementation of paper money, the next big innovation in the way people paid was the credit card. The very first credit card (which only moderately resembles the modern version) was the Charga-Plate; invented in the 1930s as a way for businesses to track a consumer's account credit accurately and efficiently.

Though the creators of Charga-Plate were onto something, the real breakthrough for credit cards came in 1950, when the revolutionary Diners Club card offered consumers a way to charge their bills at a select group of restaurants (and later hotels and other retailers) to a credit account, and pay for all of their purchases at once at the end of the month. This payment format pioneered by Diners Club would become the standard model for credit card companies going forward.

American Express and BankAmericard (now Visa) soon joined the emerging charge card market in 1958, with Amex debuting the first plastic credit card in 1959. (They had previously been made out of cardboard.)

Credit cards revolutionized the way people paid by making debt readily available to consumers, as well as offering them a streamlined checkout experience. Today, these payments are faster than ever with the advent of EMV and NFC technology, and it's estimated that around 200 million Americans possess a credit card.

Online Payments

The first online payment was processed by Visa in 1994, marking the start of a new age-few back in 1994 could have imagined the way in which online payments would impact our world. Online retailing giant Amazon was founded in 1995, and today has expanded from its humble beginnings to be one of the world's largest and most profitable companies.

The internet now fuels the transmission of billions of dollars worth of transactions every year, and e-commerce has become one of the primary ways in which consumers interact with businesses and each other.

Today, most businesses have an online store; whether they subscribe to a service like Shopify, upload products to Etsy, or use a payment gateway on a website they built themselves.

Mobile Payments

One of the last major innovations in payments is even more recent than the internet. Accepting mobile payments was possible because of NFC technology. It lets people make and accept payments wirelessly when they are on the move. QR codes are another form of mobile payment that's making it easier for people to pay and get paid. Consumers can scan a code with their mobile device camera and pay in just a few clicks.

Payments now are almost entirely digital. Whether online or in-person, money is moved electronically at lightning speed; we've come a long way from trading physical goods or gold coins.

The Future of Payments

The future of payments is uncertain; with new innovations in technology every day, it's impossible to say where the next big thing will come from, and what it will be. Cryptocurrency is certainly a hot topic, and already changing people's perceptions around what currency really is. Does it need to be government sanctioned? Can it be completely electronic? Should it be backed by something external?

Canada for example, is at "A critical junction" in regards to it's payment and financial services and their ability to compete on a global scale.

In the same way economists are always trying to comprehend the markets and stay ahead of recessions, there will likely always be debates around currency and payments. At the end of the day, if an individual sees value in something they own, they want some form of compensation before they're going to be willing to part with it.

Payments ultimately need to be functional, and are simply meant to help drive the exchange of goods and services that has carried on among humans for so many millennia. As long as they do that-perhaps better or faster in the future-people will adapt to and adopt new forms of paying and getting paid.