You made it through a year of inflation spikes, whispers of a looming recession, labor shortages, and supply chain chaos. It’s been a ride. But now, as we wrap up the year, let’s take a closer look at your business costs and find ways to keep more of your hard-earned revenue.

Chances are you’ve already been cutting costs in other areas of life: clipping coupons, choosing public transit over paying for parking, even canceling unused subscriptions. But there’s one area most business owners overlook when it comes to saving: payment processing. Yep, credit card processing fees—often seen as a “necessary evil,” like insurance or utility bills.

Here’s the thing: not all credit card processing companies are the same, and with a little know-how, you can actually cut costs here. That means real savings on this essential part of running your business. Read on for tips and tricks to help you lower those fees and boost your profitability.

Cutting down payment processing fees (Yes, it’s possible)

Let’s talk about credit card processing fees. For most business owners, these fees are just a standard line item, almost like rent or utility costs—unavoidable and, frankly, annoying. But here’s the plot twist: payment processing costs don’t have to be a financial black hole.

Different credit card networks, such as Visa and Mastercard, influence the fees you pay, with each network having its own assessment fees and variability in processing charges. Understanding the fees associated with accepting credit card payments is crucial for businesses to manage costs effectively.

One great way to kickstart your new saving habit is by taking a closer look at how much you’re spending on credit card processing fees. With the right provider, you could actually start saving on these fees rather than letting them chip away at your profits.

Understanding credit card processing fees

Before you switch providers, it’s crucial for businesses to know what these credit card processing fees are, and make informed decisions about their payment processing needs. These fees are a necessary cost for businesses that accept credit card transactions, but they don’t have to be a mystery. Let’s break down the three layers of charges you might encounter:

- Interchange fees: These are paid to the credit card network and are typically the largest component of your processing costs. They vary based on the type of card and transaction.

- Assessment fees: Also paid to the credit card network, these are usually a smaller percentage of the transaction amount.

- Markup fees: These are charged by your merchant account provider and can vary widely depending on your provider and pricing model.

On average, credit card processing fees range from 1.5% to 3.5% of each transaction. However, even though most card processors offer flat processing fees, the true fees can fluctuate based on the type of credit cards you accept, how you accept them (online vs in-person), and the pricing model your provider is on.

While some businesses opt to pass credit card fees on to customers, it’s not always feasible or customer-friendly. Negotiating lower fees can be challenging, but understanding these components is the first step toward managing your costs effectively.

Give your profitability a year-end audit

Now that you understand the fee structure you are on, the next thing to do is to give your profitability a year-end review. Think of it as a financial checkup to ensure you’re entering the next year with a clear sense of what’s working and where there’s room to improve. Here’s a checklist to guide you:

Review your pricing

Are you charging what you’re worth? Don’t be afraid to adjust prices if it’s time. Many business owners avoid this, but a modest increase can offset rising costs and improve profitability.

Examine your expenses

Check everything from software subscriptions to office supplies. Are you paying for tools that overlap? (Hint: Helcim can cover invoicing and in-person payment processing, so you can cut down on multiple subscriptions.)

Scrutinize monthly fees

Payment processing fees can add up, especially if you’re on a “flat rate” or subscription model. Take a hard look at your processor’s monthly fees and see if a different structure could save you money.

Assess efficiency

Review your workflow and consider where you can streamline processes. Could automation tools help cut down time and costs? Every little improvement helps.

Know your processing fees

Dive into your monthly statements and look for hidden fees. This simple step can reveal unexpected expenses you may be able to negotiate or eliminate with your processor.

Recognize your hidden cost drivers

Certain expenses are obvious—like inventory and labor—but others, like credit card processing fees, batch fees, monthly fees, often slip under the radar. Here’s a breakdown of cost drivers that can eat into your profits if left unchecked:

- Labor costs: Staffing shortages mean many businesses are paying a premium. Look for opportunities to cross-train employees and keep staffing efficient.

- Inventory management: Over-ordering ties up cash, while under-ordering leads to missed sales. Keeping this balanced is crucial.

- Payment processing fees: These are a huge semi-hidden cost. Many business owners see them as non-negotiable, but with the right processor, they don’t have to be. From interchange fees to sneaky admin charges, these costs deserve a closer look.

- Monthly fees and rentals: Paying $30 a month for equipment rental? Do the math—it might be cheaper to buy upfront and avoid the monthly fee. Subscription models with a higher monthly fee might offer lower transaction fees, which could be beneficial for businesses with higher sales volumes.

- Hidden fees: Payment providers—and other service vendors—can get pretty creative when it comes to slipping hidden fees into your statements. That’s why it’s essential to review your monthly statements closely for charges like “admin fees”, “service fees”, and “software fees.” Payment processor fees can encompass various costs, including monthly fees, per-transaction fees, and equipment lease fees.

By staying on top of these, you’ll have a clearer understanding of what each fee entails and avoid paying for anything unnecessary. The key takeaway: While these costs are often overlooked, understanding where your money goes can help you optimize and potentially save significantly.

Steps to reduce credit card processing fees

With credit card transaction fees taking up a guaranteed 1-4.5% of every sale, they’re undeniably a high-priority area for savings. If you’ve done your homework and pinpointed areas to improve, it’s time to take action. Here are some key steps to get you started:

Understand your contract

In payment processing, a contract can often be a red flag. Why? Because it typically means lock-in periods and monthly costs that can become costly if you want to switch providers. Many other providers offer the same (or better) services without contracts or monthly fees. If it's inevitable to go with a merchant without a contract, do keep an eye out for hidden costs like early termination fees, equipment rentals, and “PCI compliance” charges—these fees can often be negotiated or even avoided entirely with the right provider.

Know your statement

Build the habit of looking into the fine print during your monthly statements. Familiarize yourself with the line items and look for high or unnecessary fees. You can also compare your current statement with other payment processors to ensure you're always getting the best deal for your business.

Consider interchange-plus pricing

Because actual credit card fees fluctuate, many payment processors use flat-rate pricing for simplicity. However, these rates are typically set high to ensure profitability, which often means you end up overpaying. In contrast, the Interchange-plus pricing model offers transparency, giving you more control and potentially more savings over time.

Skip monthly equipment rentals

Leasing equipment can add up fast. If possible, buy equipment outright to avoid rental fees. Hint: Helcim offers flexible installment plans for their hardware, so you can spread out the cost without a hefty upfront payment—and the equipment is yours to keep!

Beware of flat-fee pricing models

While simple, flat-fee pricing might not be the most cost-effective choice for your business. Card brands periodically adjust interchange fees, and when they rise, flat-rate processors typically increase their rates to protect their margins. However, when interchange fees drop, many processors keep rates unchanged, pocketing the difference instead of passing savings on to you. For example, in October 2024, The Globe and Mail reported that Stripe would not lower its merchant fees, despite agreements by Ottawa with credit card firms to reduce fees for businesses.

Ask for volume discounts

Many providers offer discounts based on transaction volume, so it’s worth asking if you’re processing regularly. Hint: With Helcim, volume discounts are applied automatically—no need to negotiate or ask for it! The more you process, the more you save.

How Helcim help you save an average of 25% in credit card processing fees

At Helcim, we know small businesses need an affordable payment processor without the headaches. Here’s how we help reduce fees:

- Interchange-plus pricing: Interchange-plus pricing is all about transparency. Helcim offers every merchant a direct view of what they're really paying. Instead of one flat rate, merchants get the actual interchange rate plus a small markup (that goes down over time as you process more), making it a smart, cost-effective choice. It’s like paying the true wholesale price for payment processing, so you know exactly where your money goes with every transaction.

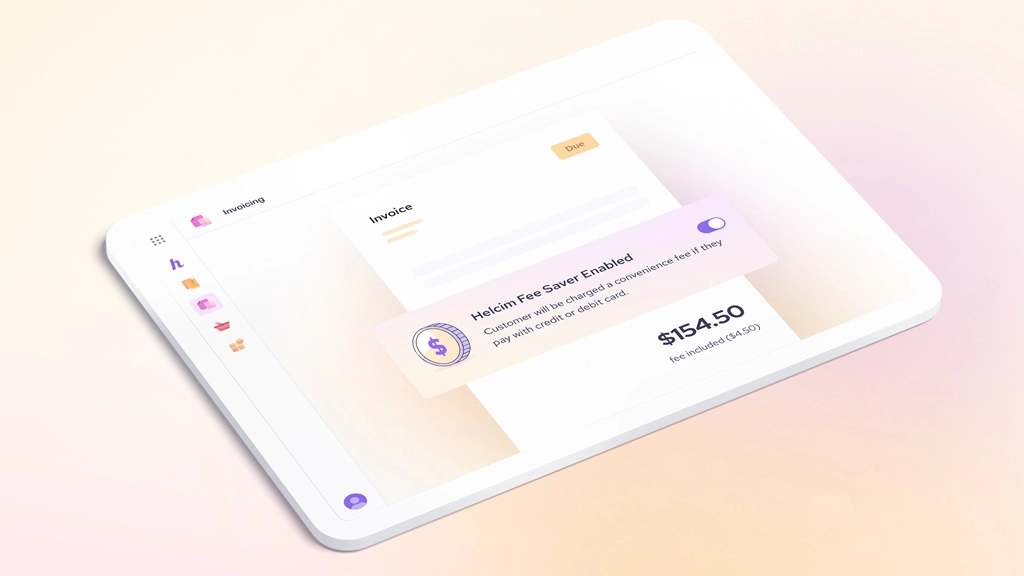

- Fee saver: Want to avoid paying processing fees altogether? With Helcim’s Fee Saver, you can pass on credit card processing fees to customers who choose to pay with a credit card. This means you keep more of every sale, allowing customers to cover the cost of their chosen payment method.

- Level 2 and Level 3 data: Level up your savings on B2B and B2G transactions. At Helcim, eligible merchants get automatic access to our Level 2 and 3 optimization. This means we include additional transaction data—like itemized purchases, tax breakdowns, and purchase order numbers—so you get rewarded with lower rates. Credit card networks appreciate the added detail and transparency, so qualifying payments become cheaper to process. Think of it as reducing costs by meeting higher data standards.

- Automatic volume discounts: Processing more? Save more. Helcim automatically applies volume discounts based on your transaction totals, meaning your per-transaction fees shrink as your business grows. It’s an effortless way to maximize savings without any negotiation—just let the savings roll in as your business scales.

- Switching has never been easier: Helcim’s Merchant Buyout Program brings savings right to your doorstep. Receive up to $500 to cover cancellation costs, from equipment fees to early termination charges, when you move from another provider. Plus, Helcim’s dedicated support team and step-by-step guides make migrating customer and card data a seamless experience, ensuring a smooth transition from day one.

As the new year approaches, take the steps to put more money back into your business. Choose a payment provider who’s as invested in your success as you are.

FAQs on cutting payment processing fees

Q: How can small businesses reduce payment processing fees?

A: Reducing payment processing fees starts with understanding your contract and fees. Look out for hidden charges like early termination fees, equipment rentals, and compliance charges. Also, consider switching to an interchange-plus pricing model, which offers greater transparency and often lower costs than flat-rate pricing. Regularly reviewing your statements for unnecessary charges can also help you avoid overpaying.

Q: What are credit card processing fees, and how can I lower them?

A: Credit card processing fees are charges merchants pay to accept card payments, including transaction fees, interchange fees, and service fees. To lower them, opt for a transparent pricing model like interchange-plus, which separates the base cost (interchange) from the markup. You can also avoid costly monthly rentals by purchasing equipment outright.

Q: Why are credit card merchant fees important for small businesses to monitor?

A: Credit card merchant fees can add up quickly, impacting your profit margins. Small businesses often overlook these fees, but by monitoring statements and choosing a provider with low-cost credit card processing, you can save significantly over time. Helcim’s transparent pricing is designed to help businesses keep more of their revenue.

Q: What are the common drivers of costs in credit card processing fees for small businesses?

A: Common cost drivers in credit card processing fees include the pricing model (flat rate vs. interchange-plus), hidden fees (such as PCI compliance and batch fees), the cards you accept (high-reward cards vs consumer), the method you accept them (online vs in-person) and equipment rentals. Processing fees for credit or debit card transactions can significantly impact merchants, as they are compelled to accept card payments, making these fees an integral part of their operational costs. By understanding and auditing these factors, you can better control your credit card processing fees and keep costs down.

Q: What is interchange-plus pricing, and is it good for small businesses?

A: Interchange-plus pricing is a model where you pay the wholesale rate (interchange) plus a small markup, rather than a flat rate for each transaction. This model provides transparency and can save small businesses money compared to flat-rate pricing, as it reflects the true cost of processing each transaction. Helcim offers interchange-plus pricing to help small businesses get low-cost credit card processing.

Q: How can I find a low-cost credit card processing option for my small business?

A: Look for a provider that offers transparent, interchange-plus pricing without hidden fees. Avoid processors with monthly fees, long-term contracts, or expensive equipment rentals. Helcim’s pricing structure is designed with small businesses in mind, eliminating hidden fees and unnecessary charges for a lower cost of credit card processing.

Q: Are flat-rate credit card processing fees better for small businesses?

A: Flat-rate processing fees are straightforward but can be more expensive in the long run, especially if interchange rates go down and those savings aren’t passed to you. If you’re looking for savings, interchange-plus pricing is typically more cost-effective. With Helcim, you get transparency and potential savings, as our pricing adapts to the actual interchange rates rather than sticking to a high, flat fee.

Q: How does Helcim help reduce credit card processing fees for small businesses?

A: Helcim offers transparent, interchange-plus pricing with no monthly fees or hidden charges, which helps small businesses save around 25% on credit card processing fees. Additionally, Helcim’s Fee Saver program lets businesses pass processing costs onto customers, and our support for Level 2/3 data processing can further lower rates by qualifying transactions for discounted interchange fees. Plus, if you’re ready to switch providers, our Merchant Buyout Program can cover up to $500 in cancellation fees, making the transition easy and affordable.

Q: Why do credit card processing fees for small businesses vary?

A: Fees vary based on factors like transaction types (in-person vs. online), card types (rewards vs. standard), and the pricing model you’re on. Small businesses can lower their fees by choosing a provider with transparent interchange-plus pricing and avoiding providers that tack on hidden fees.