Repeat customers are gold. But repeat payments? Those can feel like Groundhog Day. Every time Sheryl, your favorite regular, walks in, you ask the same question—“How would you like to pay today?”—like you haven’t seen the same card four days in a row. The machine beeps, the receipt prints, and everyone pretends this isn’t somewhat annoying.

What if there was a way to skip the payment ritual entirely?

Enter: Card-on-file payments—the modern version of starting a tab minus the “I’ll settle up later” anxiety. It’s faster for you, easier for your customers, and just flat-out smarter for your business.

If you’re a small business owner looking to simplify repeat billing or take some of the friction out of getting paid, this guide is your go-to. Let’s break down what card-on-file payments are, how they work, where they shine—and how to set them up the right way.

What are credit card-on-file payments?

Let’s start with the basics—because you deserve a plain-English explanation.

A card-on-file payment is when a business stores a customer’s credit or debit card information for future use. The customer gives permission, the business saves the card (safely, of course), and the next time a charge is needed, voila—it’s already set up.

You’ll see this in action with subscriptions, invoices, recurring appointments, or simply with regulars who are tired of fishing their wallet out every visit.

But here’s the thing: storing card data responsibly isn’t optional. It’s regulated by PCI-DSS—the Payment Card Industry Data Security Standard. These are global rules designed to keep credit card data safe and reduce payment fraud. So while card-on-file refers to the practice of keeping payment data on hand for later use, how you store it matters. That’s where tokenization comes in (more on that shortly).

How do they work?

Let’s demystify the process. Because while the tech behind card-on-file payments sounds complex, the experience is refreshingly simple.

Here’s how it typically goes:

- Your customer agrees to have their card saved on file (usually during checkout or through a signed agreement)

- An online form can also be used to obtain customer consent for storing card details, efficiently managing customers' credit and avoiding repeated requests for card information

- Instead of storing the actual card number, the data is turned into a secure “token”—a digital placeholder that only your payment processor can decipher. This is done through a process called tokenization.

- When it’s time to charge them—whether it’s next week, next month, or when a job is done—you just hit “charge now” and that token will do it’s thing

- That’s it. No swiping, no awkward “can I get your payment info again?” emails, and no hardware required. It’s all done through your payment provider.

What’s the difference between card-on-file and tokenization?

Let’s clear this one up—because the terms might get used interchangeably, but they mean different things. Card-on-file refers to the practice of storing a customer’s card details for future use.

Tokenization, on the other hand, is the security layer. It replaces sensitive card data—like the card number and expiry date—with a unique, encrypted token that can only be used by your payment processor.

So:

- Card-on-file = What you're doing (saving the payment method)

- Tokenization = How you're doing it securely (so no one can hack it)

The two work hand-in-hand. A reliable payment provider will never store raw card data directly—they’ll tokenize it the moment it’s submitted. Think of it like writing a customer’s tab in invisible ink. You can read it. Hackers can’t.

Tokenization keeps your business compliant, protects your customer, and ensures that even if someone tried to snoop around, they wouldn’t be able to do anything with the data.

Are card-on-file payments safe?

You’re dealing with real money, real people, and real trust—so yes, safety matters. The good news: card-on-file payments are safe when you follow best practices. That means:

- Never storing raw card data yourself

- Using a PCI-compliant provider that handles tokenization and encryption

- Always getting clear customer consent before charging or saving their card

If you're using a provider like Helcim, all of this is built-in. So you don’t need to be a security expert to do things the right way.

Bottom line? When done properly, card-on-file payments are not only safe—they're often safer than asking for card info again and again.

Are there any downsides?

As with any payment tool, card-on-file comes with a few caveats—not dealbreakers, but definitely things worth being aware of.

First, there’s customer trust.

Not everyone’s immediately comfortable saving their card info, especially if it’s their first time doing business with you. It takes transparency, clear consent, and a bit of relationship-building to ease those concerns.

Second, card-on-file payments rely heavily on authorization agreements.

If you’re going to charge someone later—especially when they’re not present—you need to have crystal-clear consent and terms in place. That protects both parties and keeps you compliant with payment rules.

There’s also the issue of stale card data. Cards expire.

They get reissued. Customers cancel them. If your system doesn’t flag that—or if you're not staying on top of updates—you could run into failed payments and delayed cash flow.

And finally, keeping it safe.

While the security burden is mostly handled by your payment processor (if you’re using a provider like Helcim), you’re still responsible for using it correctly. That means not storing card details outside the system, being transparent with customers, and following the proper procedures for authorization and usage. In short: card-on-file is an incredibly helpful tool—but like anything in payments, it’s only as smooth as the setup behind it.

What are the alternatives?

Depending on your business model and customer preferences, you might explore a few variations:

- ACH payment processing – Save a customer’s bank account instead of a credit card. It’s ideal for large payments and typically comes with lower processing fees

- Digital wallets – Like Apple Pay or Google Pay. The card is technically stored—but on the customer’s device, not yours.

With Helcim, you can offer all of these payment methods in one platform. That means your customers get options, and you stay flexible without cobbling together a dozen tools.

How can a small business actually use this?

You don’t need to be a giant company to use card-on-file. In fact, small businesses often benefit the most from this kind of setup. Here’s where it fits:

- Personal services – Massage therapy, coaching, dog grooming—charge after sessions without chasing payments

- Professional services – Consultants and freelancers can automate invoicing and reduce back-and-forth. Explore the top 5 invoicing softwares for freelancers here.

- Retail – Let customers save their card at checkout to make reordering easier

- Home services – Store cards for monthly or seasonal visits and bill after the job is done. Securely storing customers’ card details facilitates future transactions and enhances customer experience.

- Subscription services – Businesses like gym memberships use card-on-file payments to manage monthly recurring payments

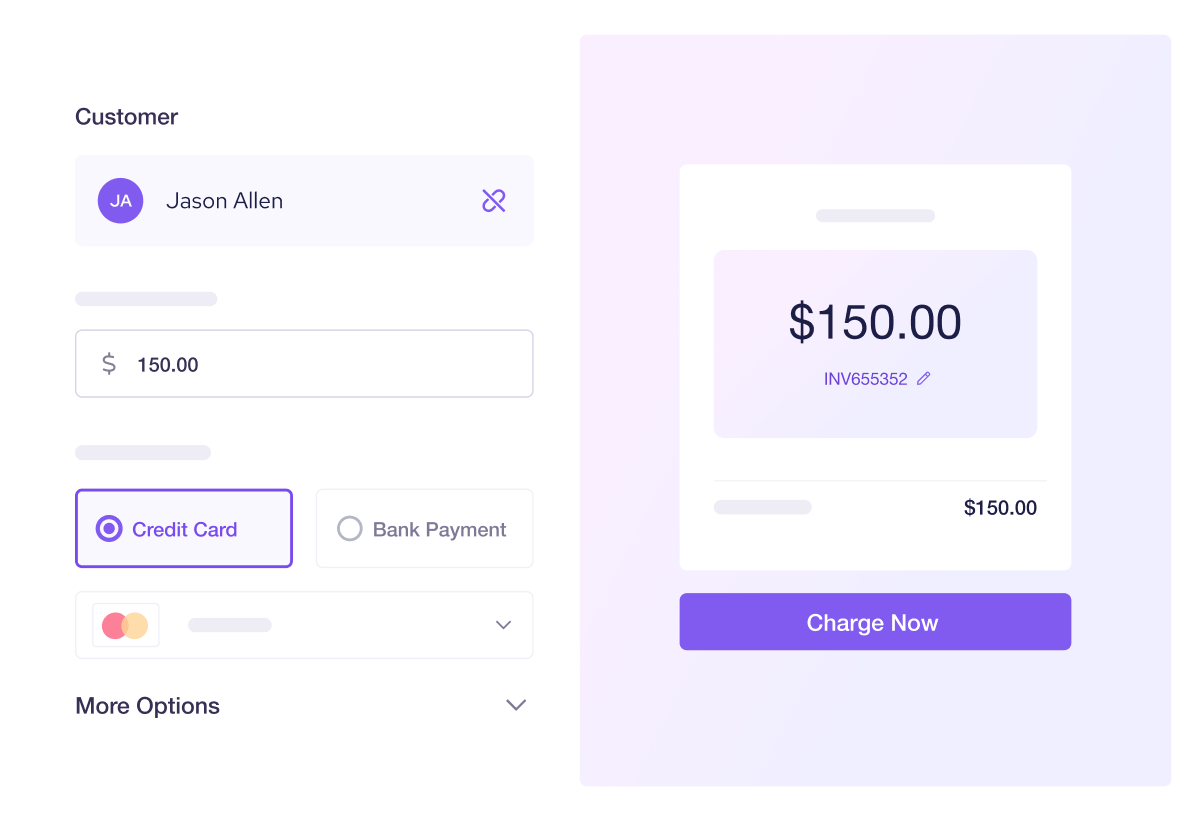

Using a virtual terminal to make card-on-file ridiculously easy

Here’s the thing—card-on-file sounds great, but if setting it up feels like launching a spaceship, most business owners will peace out before liftoff. That’s why Helcim’s Virtual Terminal exists. It’s one of the easiest and quickest ways to process card on file payments—without the tech headaches. From any browser, you can:

- Take payments over the phone, in person, or remotely

- Manually enter a customer’s card (or ACH bank transfer details–it has both!), with their authorization

- Securely save that info for future billing

- Initiate payments later with just a few clicks—no swiping, no extra hardware

- Detect if a card or payment method is about to expire or has been compromised

- Automatically bill customers for future purchases, enhancing efficiency

While Helcim’s Virtual Terminal is the easiest way to get started with card-on-file payments, it’s not the only one. You can also securely store and charge cards through other powerful tools like online invoicing system and Recurring payments —no card reader or special setup required. All you need is your Helcim account, a customer’s permission, and a reason to get paid—whether it’s once, on a schedule, or whenever the job’s done.

It’s especially great for:

- Service businesses that invoice after work is complete

- Professionals who want to simplify repeat billing

- Merchants who hate having to say “Can I grab your card again?”

- Businesses who want to start offering card-on-file, but don’t want to overhaul everything

The best part? It’s free to use. You only pay when you process a transaction. If you’re looking for the easiest way to get started with card-on-file payments, this is it.

Best practices to keep things running smoothly

Choosing a PCI-compliant provider is half the battle—but the other half is making sure your business holds up its end of the deal. That means things like:

- Always getting clear customer consent before processing payments

- Never storing raw card data manually—use tokenization and encryption

- Being upfront about your billing policies so customers know exactly how and when they’ll be charged

- Obtaining signed agreements or pre-authorization for recurring or delayed charges

- Keeping stored payment details up to date to avoid declines and failed payments

- Following PCI-DSS guidelines to stay compliant and protect your business

Get these right, and you’ll not only protect your business—you’ll make payments something your customers don’t have to think twice about.

Wrapping it all up: Set the tab, keep it secure, get paid

Card-on-file payments aren’t just for giant retailers and SaaS companies. They’re for the dog groomer, the freelance designer, the HVAC team, the shop owner who doesn’t want to waste time re-typing the same card every time a job wraps up.

They save time, reduce friction, improve cash flow, and make the payment process a whole lot easier on everyone involved by facilitating easier future transactions. And with providers like Helcim, you don’t need special equipment or complex systems to make it happen. You just need an account, a customer, and a reason to get paid.

FAQs

Can I keep a customer’s credit card on file?

Yes, with their permission and a PCI-compliant provider. It is crucial to securely store customer payment credentials and obtain proper consent for their use in billing cycles.

Can I charge a card that’s on file?

Yes—if the customer has given consent, you can charge their card based on the terms you’ve agreed to. There are two types of transactions this applies to:

- Consumer-initiated, where the customer agrees to run the charge at the point of sale—either in person or online.

- Merchant-initiated, where you charge a stored card for recurring or delayed payments without needing the customer to re-enter their details—so long as they've authorized it. Card-on-file is especially useful for subscriptions and ongoing services, where predictable, pre-approved billing keeps things easy and efficient for everyone.

What should I never do with cardholder data?

Never write it down, email it, or store it in plain text. Use a provider that has tokenization and encryption, and always follow PCI-DSS standards to protect your customers and your business.

Are card-on-file payments safe?

Yes. When handled properly, they’re one of the safest and most convenient payment methods available. The card on file benefits include consistent and timely payments from customers, which is crucial for maintaining cash flow. Additionally, businesses can securely store multiple credit cards and manage various payment types seamlessly, aiding in operational efficiency and scalability.

Do all providers notify me when a card is about to expire?

Not all providers do—but the good ones should. Some payment processors offer card updater tools or automatic alerts when a card on file is about to expire, has been replaced, or is no longer valid. Helcim, for example, flags expiring cards so you can update them before a payment fails.

What types of card payments can I store? Can I use debit cards too?

Yes. Most major credit and debit cards can be securely stored and used for card-on-file payments, depending on your provider. Some can also store ACH payment-on-file information too.