Did you know that 80% of Americans prefer using credit or debit cards over cash and that for small businesses, card payments can account for up to 70% of all transactions? If you’re running a business, having the right credit card machine isn’t just a nice to have—it’s essential for improving your customers' checkout experience and meeting modern business needs.

But how much does a credit card terminal really cost? Should you buy one, lease it, or look for alternative options? And what about those pesky fees? Let’s dive into all the details so you can make the best decision for your business.

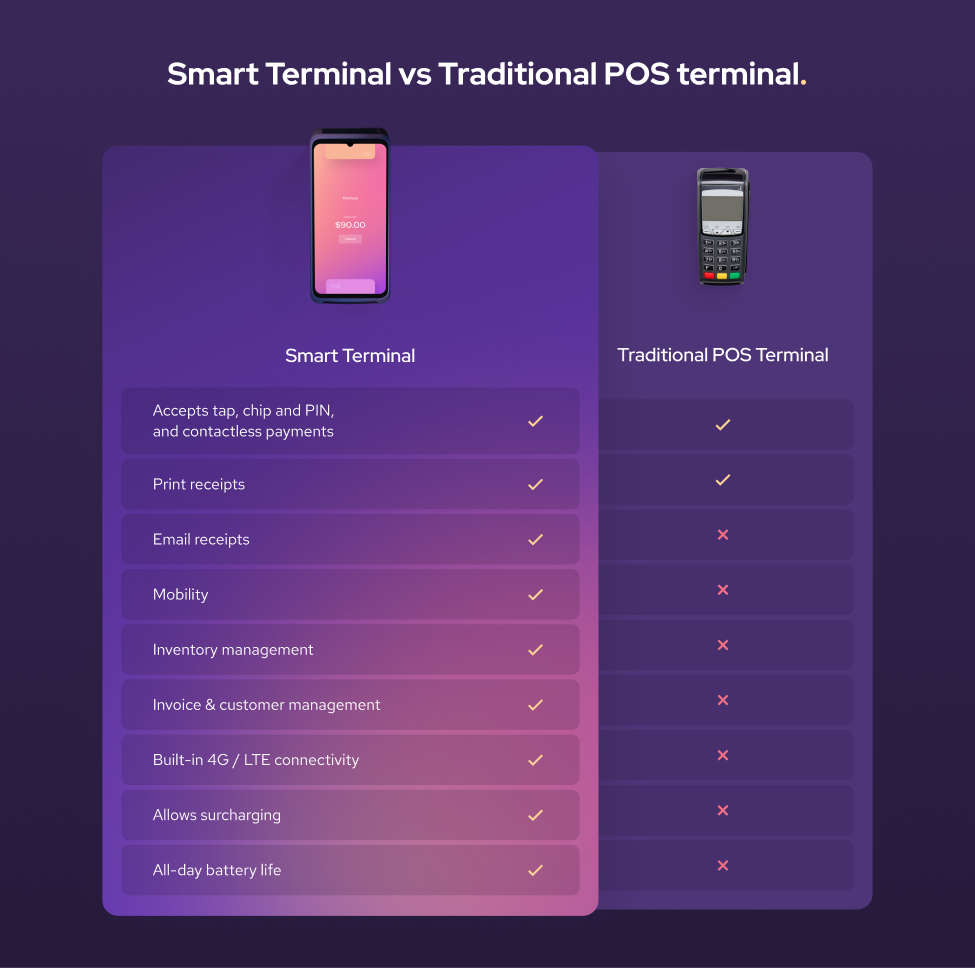

What are the different types of credit card machines?

Credit card machines are like tools in a toolbox—different ones work best for different jobs. Here are the most common options:

1. Traditional credit card machine

These are the classic devices you’ve probably seen at retail stores or cafes. They’re connected to a phone line or Ethernet and handle chip, swipe.

Best For: In-store transactions.

Example: Your neighborhood boutique or favorite coffee shop.

Bonus: Some traditional machines include a cash drawer for easy handling of multiple payment methods.

2. Mobile or wireless credit card terminals

If your business goes where your customers are, wireless credit card terminals are the perfect fit. They connect via Wi-Fi or cellular networks, allowing you to accept payments on the go. Many models of card readers support contactless payments for seamless transactions.

Best For: Food trucks, pop-up shops, landscapers, and mobile service providers.

Pro Tip: Look for an all-in-one device that supports both chip cards and Apple Pay to simplify your payment process.

3. Tap to Pay on iPhone

Tap to Pay on iPhone transforms your iPhone into a powerful payment tool, eliminating the need for additional hardware. Using the built-in NFC technology on your iPhone, you can accept contactless payments, including credit cards, debit cards, and digital wallets like Apple Pay.

Best For: Home service providers, tradespeople, markets, personal trainers, and any business owner who values simplicity and portability.

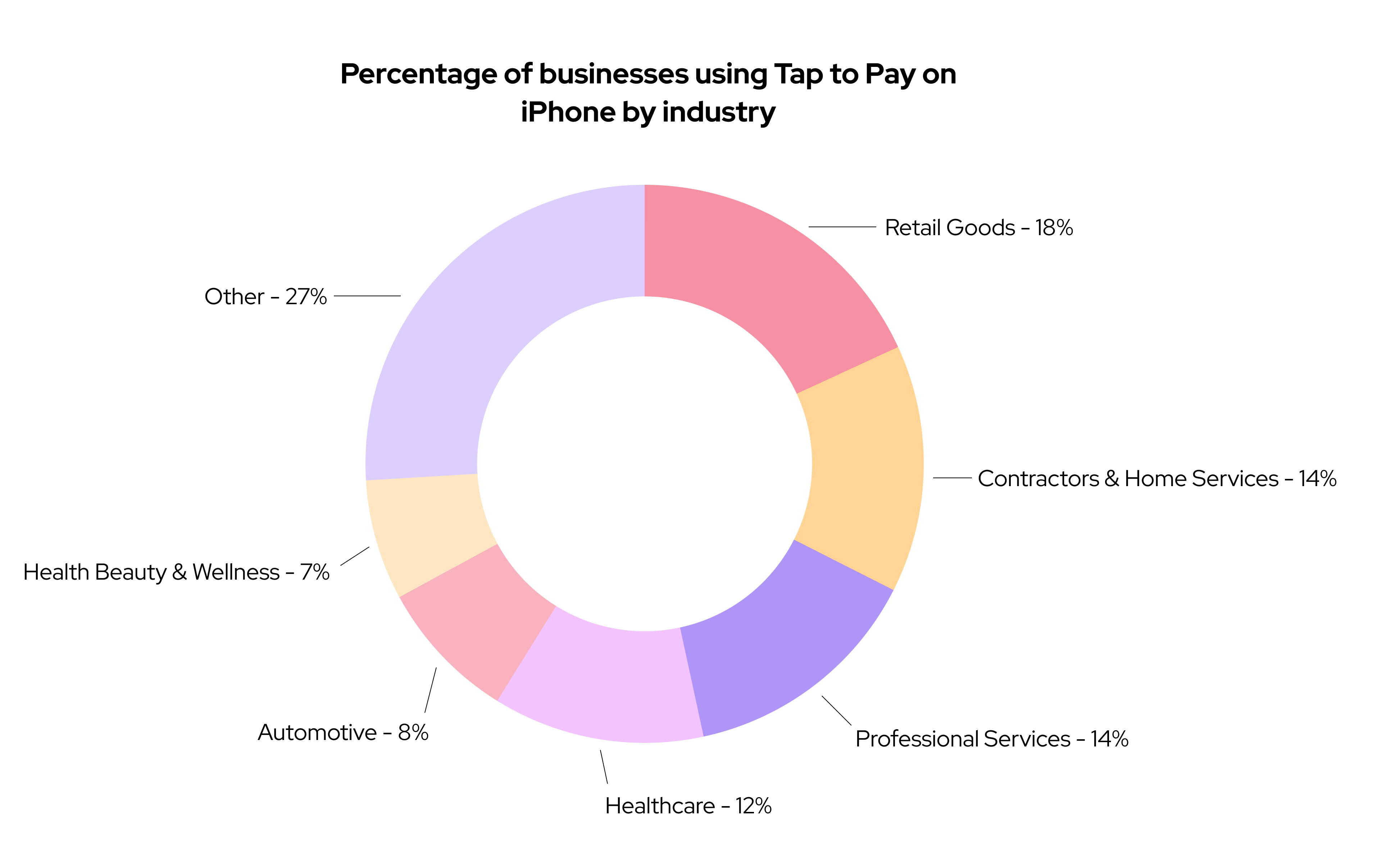

Out of all Helcim merchants who use Tap to Pay on iPhone, a handful of industries make up the most adoption: Retail Goods (18%), Contractors & Home Services (14%), Professional Services (14%), Healthcare (12%), Automotive (8%), and Health Beauty & Wellness (7%).

How It Works: Customers simply tap their card or smartphone on your iPhone to pay. Transactions are secure and fast, making it an ideal choice for on-the-go professionals or businesses without dedicated payment terminals.

Pro Tip: Ensure your payment provider supports Tap to Pay on iPhone and offers competitive processing rates to maximize your earnings. It's also a great way to reduce upfront hardware costs!

How much does a credit card machine cost?

Ah, the million-dollar question (don’t worry, it’s not actually that much). Here’s a breakdown of what you can expect to pay:

Hardware Costs

Traditional Credit Card Machines: $150–$850.

Wireless Credit Card Terminals: $50–$479.

Fancy, Feature-Packed Models: $400–$850 (think touchscreens and payment security features).

Processing fees

Let’s understand the difference between Flat Rate vs. Interchange Plus: Flat rates are simple and predictable—one fixed percentage per transaction—while interchange plus gives you more transparency by showing the exact costs set by the card networks plus a small markup. Understanding these fee structures can help you pick the pricing model that works best for your business needs.

Credit Card Fees: Usually between 1.4% and 3.5% per transaction, depending on the card type.

Debit Card Fees: Lower, around 0.25%+5 cents to 1.15% per transaction.

Monthly fees

Some providers charge monthly service fees, which can range from $10–$50. If you’re using software or integrations for payment processing, expect to pay an additional $20–$100+ monthly.

Add-ons and extras

Contactless Payments (e.g., Apple Pay): May require upgrades. Receipt Printing: Machines with built-in printers improve the customer checkout experience but cost more. Custom Integrations: Extra fees for POS compatibility or specialized features.

Hidden costs to watch out for

Beyond these standard fees, be mindful of additional costs like PCI fees, inactivity fees, and contract termination fees. These can add up and eat into your profits.

Side bar: Helcim has no monthly fees, no hidden costs and no contracts.

How to pass credit card machine fees to customers

Wondering how to cover those transaction fees without eating into your profits? Here are some options:

- Surcharging: Pass on the fees of credit card transactions to your customers. Many businesses do this, but be sure to check local regulations first and determine if it's right for your business.

- Cash Discounts: Offer a lower price for cash payments—it's like reverse psychology for savings.

- Transparency: Always let customers know about any fees upfront to avoid surprises. Passing fees transparently or offering incentives to use cash not only covers your costs but also maintains customer satisfaction by keeping them informed.

Should you lease or purchase a credit card machine?

Leasing might sound tempting because of the lower upfront cost, but let’s break it down:

Leasing Pros and Cons

Pros: Lower initial cost and predictable monthly payments. Cons: You could end up paying way more over time, especially with long-term contracts.

Purchasing Pros and Cons

Pros: No ongoing lease payments. Once you own it, it’s yours.

Cons: Higher upfront cost.

Our Advice: Buy it outright if you can—it’s usually the more cost-effective option. If you’re stuck in a lease, Helcim can help with our buyout program, so you can switch to a better payment solution without the headache.

How to get a credit card machine for your small business

Getting a credit card terminal for your small business is easier than you think:

- Choose a Provider: Look for one with transparent pricing (like Helcim!) and solutions tailored to your business needs.

- Select the Right Terminal: Decide whether you need a traditional or wireless credit card terminal.

- Sign Up: Complete your account setup and payment process agreement. 4.** Purchase or Lease:** Buy the terminal outright or choose a lease plan (hint: buying is usually better).

Ready for a credit card machine?

Getting the right credit card machine isn’t just about the cost—it’s about finding a payment solution that improves your customer checkout experience, offers strong payment security, and meets your business needs. Whether you choose a traditional machine, a wireless credit card terminal, or a cutting-edge all-in-one device, Helcim has you covered.

And if you’re stuck in an expensive lease? Helcim’s buyout program makes it easy to switch and start saving while keeping your customers happy with Apple Pay and other contactless payment options.

Ready to make payments simple? Explore Helcim’s credit card terminals today and discover how we can help your business thrive.

FAQs

1. How can I accept credit card payments without a machine?

No machine? No problem. You can use virtual terminals or mobile payment apps to handle payment processing on your phone or computer. You also have the option of Tap to Pay on iPhone where your iPhone becomes your terminal.

2. What’s the difference between a card reader and a terminal?

Card Reader: A basic device that connects to your phone or POS system.

Card Terminal: A standalone all-in-one device with more features like receipt printing and touchscreens.

3. What’s the difference between a card machine and a POS system?

Card machine: Focuses on payment processing only.

POS system: Combines payments with inventory management, reporting, and other business tools.

4. Do credit card machines charge a fee?

Yes—transaction fees, monthly service charges, and optional add-ons often apply. But with the right provider, you can minimize those costs while maximizing customer satisfaction.