A merchant account is essential for any business looking to accept credit and debit card payments. In this article, we’ll walk you through the key criteria that merchant account providers (also known as payment processors) look for, so you can start accepting payments with confidence.

What is a merchant account?

A merchant account is a special type of bank account that lets your business accept credit card payments and debit card payments, as well as other electronic payments like online ACH transfers.

Think of it as a middleman between your customer and your business bank account. When someone makes a purchase with a card, the payment first goes into your merchant account. After everything is processed and verified, the funds are then transferred to your business bank account.

How do you qualify for a merchant account?

Merchant account providers (also known as payment processors) evaluate several factors before approving a new merchant account. These criteria are in place to verify that your business is legitimate, ensure it’s not operating in prohibited industries, and minimize the risk of fraud and chargebacks that could result in losses for the payment processor (learn how to dispute customer chargeback here).

Here are four key criteria that payment processors evaluate when reviewing your application.

Your business’ industry: Some industries are considered higher risk due to higher rates of fraud and chargebacks. For example, online gaming, travel services, and insurance tend to be more prone to chargebacks compared to other industries. The nature of your industry can impact the approval rate and terms of your merchant account, depending on the level of risk the processor is willing to assume. To see where your business may fall, you can check Helcim's prohibited and restricted business list as an example.

The average size of transactions: The average dollar amount of your transactions is another important factor. For instance, if you process very high amounts in a single transaction, the payment processor is exposed to a significant amount of risk. This increased risk in one transaction requires careful evaluation to ensure the processor can manage potential chargebacks and disputes effectively.

The delay between the purchase and delivery of the product: If there’s a significant delay between when a customer makes a purchase and when they receive the product or service, it can increase the risk of chargebacks. For example, a construction project might take several months to complete. The longer the time between purchase and delivery, the greater the window for potential chargebacks, increasing the risk for the merchant account provider.

Financial health of the merchant: Payment processors may request additional information or documentation based on the risk of your account. This helps them assess the financial health of both your business and you as the merchant.

There’s no universal guideline on how your business should meet each criterion because every processor has its own methods for evaluating applications and weighing risk factors

Don’t worry if you don’t perfectly meet one of the criteria. Payment processors won’t decline you outright for not perfectly satisfying one or two areas. Instead, they may offer different options and conditions to make them more comfortable approving your application.

How to get a merchant account

Getting a merchant account is the first step for your business to accept credit and debit card payments. In the past, this process requires lots of paperwork, but now payment processors have designed a fast-track so that you can complete the application and get approved quickly.

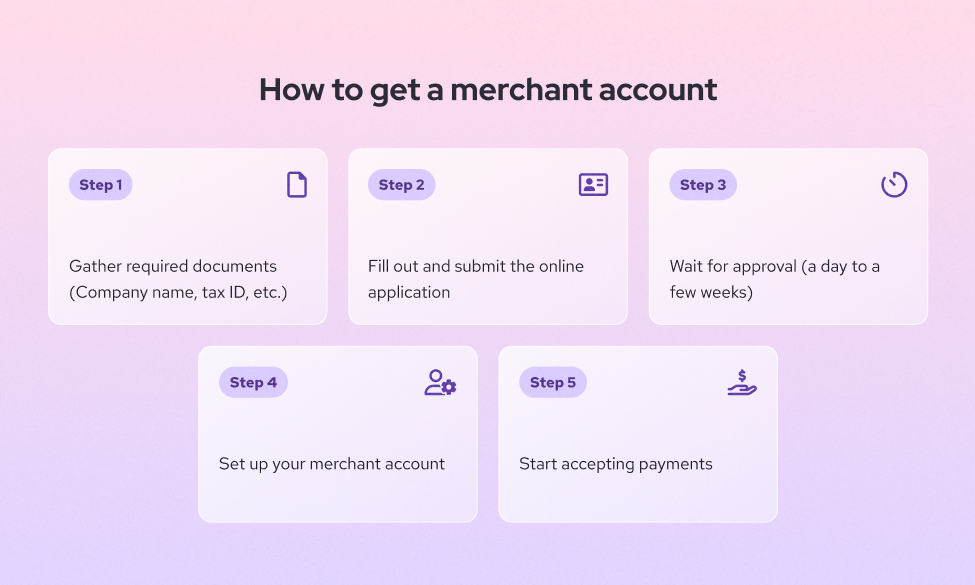

Step 1: Gather required documents

Before applying, gather the necessary documents and information.

Business Information:

- Company name

- Company tax ID or employer identification number (EIN)

- Contact information

Payment processing information for merchant account providers to better understand your business:

- Your industry and business structure

- The estimated monthly processing volume and processing history

- The products or services you offer

- The payment methods you intend to accept

- Whether you'll be processing transactions in person, online, or both

Personal Information for verifying business owner's identity:

- Your name and contact information

- Social Security Number (SSN) or equivalent identification number

- A government-issued ID (like a driver’s license or passport)

- Payment processors may ask for additional information to ensure that the business and its owners can financially support any chargebacks or refunds that might occur.

Step 2: Fill out and submit the application

Modern processors like Helcim have simplified the complicated paperwork into a quick online form. The entire application process usually takes about 5 to 10 minutes. Be prepared to provide detailed information about your business and yourself.

Once you've completed the application, submit it for review. Some providers may require additional verification or documentation, so be ready to provide any extra information they request.

Step 3: Wait for approval

The approval process can take anywhere from a day to a few weeks, but with Helcim, new applications often receive approval in less than 24 hours. Once the merchant account provider receives your business information, they will review the documents, and if anything is missing, they’ll typically reach out to let you know right away.

Step 4: Set up your merchant account

Once approved, the provider will guide you through setting up your merchant account. This process may include adding your business details, customer information, inventory information, and setting up payment terminals.

Modern payment processors like Helcim offer interactive guides that help you onboard and get your business set up quickly. If you have any questions, you can reach out to the customer success team, and they will assist you every step of the way.

Step 5: Start accepting payments

With your merchant account set up, you can start accepting credit and debit card payments from your customers. Make sure to test the system to ensure everything is working smoothly.

How long does it take to get approved for a merchant account?

Overall, the entire process typically takes between a couple hours to a few weeks. The reason for this variation is that the payment processors need to thoroughly review your submitted documents.

This review process is handled by the underwriting department. This department’s task is to assess the risk of providing a merchant account to your business. They evaluate your financial stability, credit history, and the potential risk associated with your industry.

By doing so, they ensure that your business is capable of handling card transactions securely, which ultimately protects both you and the merchant account provider from potential issues down the line.

Open your merchant account with Helcim

Getting a merchant account at Helcim is straightforward. Simply complete the sign-up that takes as little as 5 minutes. No paperwork required.

Once your application is approved, Helcim will guide you through setting up your account, including providing any necessary hardware and software.

Why choose Helcim?

- Save on processing fees: Enjoy savings of up to 24% on credit card processing fees compared to other merchant account providers.

- All-in-one account: One merchant account for accepting in-person payments and online purchases.

- Comprehensive tools: Free access to all the tools you need to accept payments and run your business, whether in-person or online.

- No hidden costs: No monthly fees, no contracts, no hidden fees – you only pay for what you process.

If you’re currently with another provider, Helcim’s Merchant Buyout Program will waive up to $500 in processing fees to cover your early termination fees or equipment leases. We also provide step-by-step support to help you migrate your data to Helcim.

Start your journey with Helcim today and experience seamless, cost-effective payment processing.

FAQ

Can I cancel a merchant account?

Yes, you can cancel a merchant account, but it's important to review the terms of your contract first. Some providers may have early termination fees or other penalties if you cancel before the end of your contract period.

Do merchant accounts require a credit check?

Yes, having good credit can be important when applying for merchant accounts. Payment processors often require personal credit checks or business financial statements to ensure that the business and its owners are financially stable and capable of handling any chargebacks or refunds that might occur.

What are high risk merchant accounts?

High-risk merchant accounts are designed for businesses that operate in industries with a higher risk of fraud, chargebacks, or financial instability. Examples include businesses involved in crowdfunding, tobacco, or medical and drugs. The risk level can also be influenced by the volume of credit card transactions being processed. High monthly volumes or large amounts per transaction are often seen as riskier by payment processors.

Do I need a merchant account to accept credit cards?

Yes, you need a merchant account to accept credit card payments. A merchant account ensures that funds are securely transferred from the customer’s bank to your business bank account. Besides, a merchant account grant you an access to merchant services and tools to process payment online and in person. However, if you sell on marketplaces like Amazon, Etsy, or eBay, you won't need a separate merchant account since these platforms have their own integrated payment solutions.

What is merchant account underwriting?

Merchant account underwriting is the process payment processors use to assess the risk of providing a merchant account to a business. During this process, the processor evaluates factors like your industry, financial stability, credit history, transaction volume, and average transaction size. This helps determine if your business can securely handle card transactions and manage risks such as fraud and chargebacks.