There are many ways to accept online ACH payments using various ACH payment processing tools — including ways to set up recurring payments. We will cover those in this article, plus our top tips on how you can use ACH payments as a more affordable method.

What is an online ACH payment?

ACH transactions (automated clearing house payments) are simply another method to transfer funds. They are a form of electronic payment, or electronic fund transfer (EFT), made directly from one bank account to another through the ACH network. The automated clearing house network that ACH payments travel through facilitates these pre-approved bank-to-bank moves. Although not as snappy as credit cards, ACH keeps chargeback risks low and has the added bonus of cost-effectiveness due to lower payment processing fees.

How can I accept ACH payments online?

If you're looking to accept your first ACH payment here are the steps you will need to get started:

- Step 1: Find a processor that offers ACH payment processing

- Step 2: Get the customers to sign the ACH authorization form

- Step 3: Offer ACH as a payment method on an online tool

- Step 4 (optional): Give your customers a reason to pay via ACH transfer

1. Find a processor that offers ACH payment processing

Because ACH uses a different network, double-check that your processor supports ACH debit specifically. You'll also want to determine how much ACH payments cost. For example, Helcim charges 0.5% + 25¢ per ACH transaction. The ACH fees are capped at $6 for transactions below $25,000.

2. Get the customers to sign the ACH authorization form

Before accepting ACH payments, you'll need your customers to fill out an NACHA-compliant ACH authorization form. You can send this form by email, or your payment processor can include it directly on the payment tool. Customers fill in their bank account details right there, making it quick and easy for everyone.

To find the bank account details, all your customer has to do is log in to their online banking, copy their account and routing numbers, and paste them into the form.

3. Offer ACH as a payment method on an online tool

Accepting online ACH transfers is simple and intuitive with the right payment processor and tools. Tools that make the most sense to accept ACH payments with include:

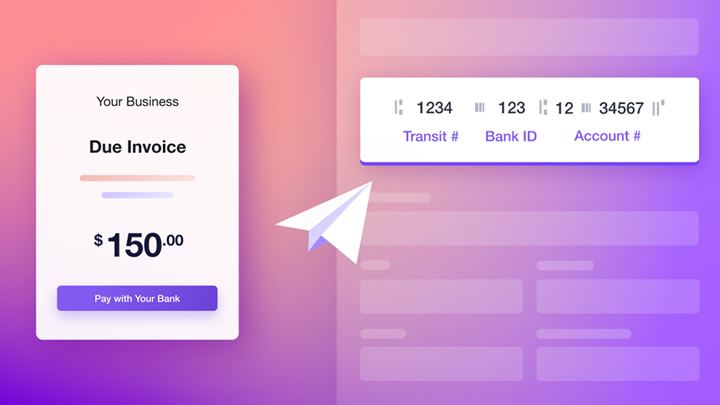

- Invoicing: You simply send your customers an online invoice by email. They enter their bank details directly on the invoice payment page.

- Recurring Payments: After your customers submit the authorization form, the recurring payment software will automatically pull their funds on the scheduled cycles.

- Online Checkout: On the checkout page, customers enter their bank account details to make a purchase, just like they would with a credit card.

- Payment Requests: Send your customers a payment request link by email or text. They follow the link, input their bank account details, and make the payment.

- Virtual Terminal: Payment processors like Helcim securely save your customer’s ACH payment details so that you can retrieve and process repeat transactions faster with a Virtual Terminal.

4. Give your customers a reason to pay via ACH transfer

Before your customers switch to ACH payments, they'll need a good reason to move away from their credit cards. After all, ACH might seem unfamiliar or inconvenient at first—especially if they're used to quick card transactions.

One effective way to get customers comfortable with ACH is by offering incentives, like giving a small discount when they use ACH or adding a convenience fee for credit card payments.

Clearly explaining these benefits helps ease customers into the idea. It also helps to remind them that they only need to enter bank details once. After that, their information is securely saved in a system for future purchases, making checkout fast and easy every time.

How do ACH payments work?

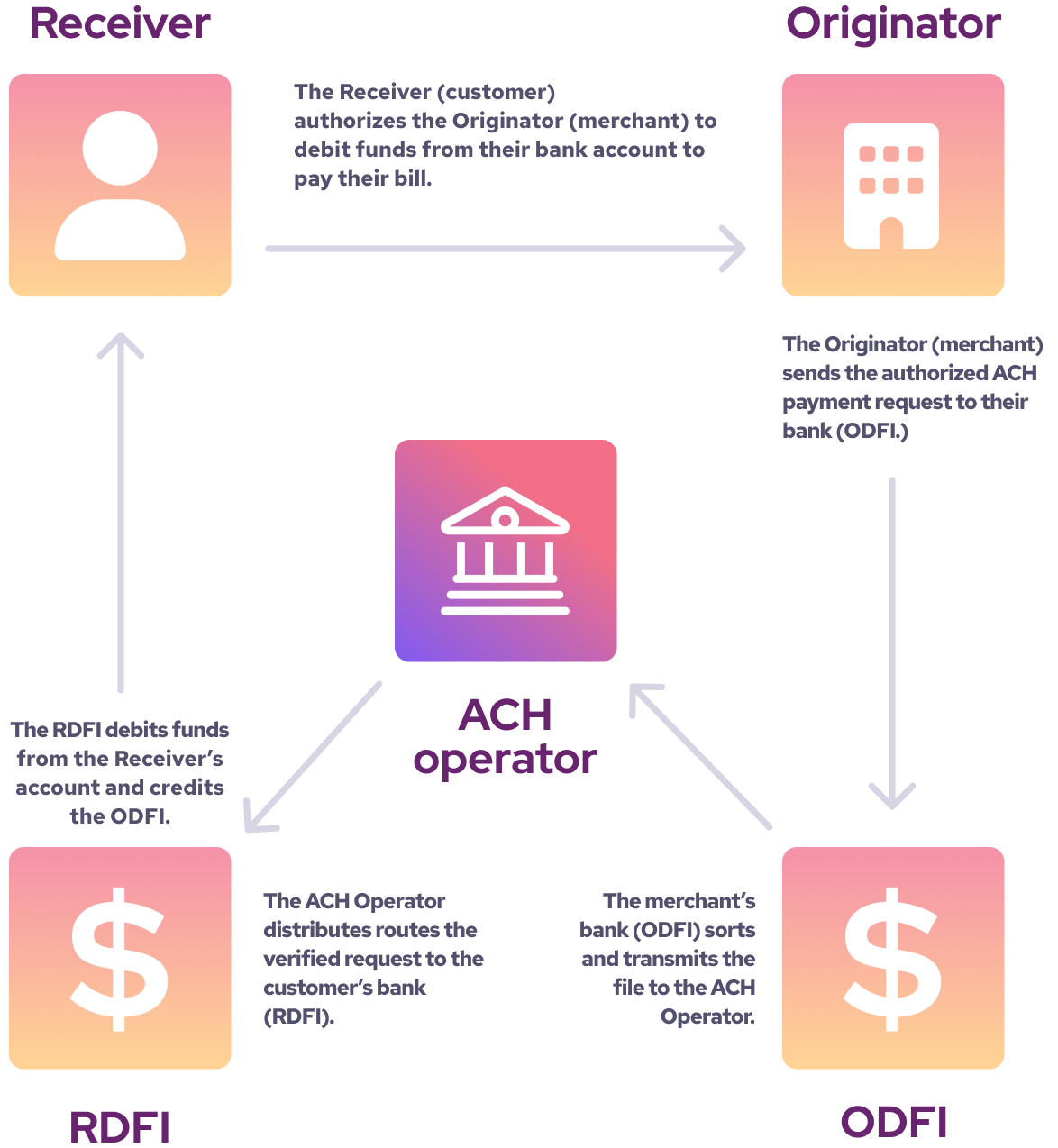

Step 1. Collect the customer’s bank details: First, your customer must give you explicit permission to take money from their bank account. They can provide this permission through a NACHA-compliant ACH authorization form. You need their bank account number, routing number, and the amount they agree to pay.

Step 2. Submit the payment request: You then enter the customer’s details and transaction amount, and your payment processor creates and submits the payment request. This kicks off the transaction through the ACH network.

Step 3. The ACH network processes the payment: Your request travels through the ACH network. This network sends the payment info securely from your bank (the Originating Depository Financial Institution, or ODFI) to your customer's bank (Receiving Depository Financial Institution, or RDFI).

Step 4. The money transfers through the ACH network: The customer’s bank verifies: account details, availability of funds, and authorization by the account holder. If approved, the ACH network initiates the electronic transfer of funds. This process usually takes 1-3 business days, depending on your ACH processor and the banks involved.

Step 5. Funds are deposited into your business bank account: Once the transfer clears, the payment lands in your account. You’ll see it show up as a deposit, minus any ACH processing fees. You can then access and use those funds however your business needs.

How many types of ACH payments are there?

In order to process ACH payments, funds are typically pulled or pushed from one bank account to another through the ACH network.

- ACH debit payment ("pull"): Your business pulls money directly from your customer's bank account (with their approval). For example: Collecting monthly subscription fees or bills from customers.

- ACH credit payment ("push"): Someone pushes funds from their bank directly into yours. For example: Payroll payments or direct deposits to employees.

Most of the time, businesses looking to receive payments will be looking for ACH debit transactions.

What are the advantages and disadvantages of online ACH payments?

Advantages: Businesses prefer ACH payments for larger purchases, where the processing fees might be higher. You can also use online ACH payments for recurring payments. Once you set up payments to be pulled from your customer bank accounts, you won't have to think about it again. This is one of the advantages of ACH payments vs. credit card payments since the payment details don't typically expire unless your customer's bank account is closed.

Disadvantages: An ACH transaction requires a little more administrative work upfront to obtain the bank account details, which makes it a little more impractical for one-time in-person payments. For example, paying with your transit number and account routing details for your morning coffee isn't exactly practical.

Why do businesses prefer ACH payments?

Businesses prefer ACH payments because of some impressive benefits of offering ACH.

- Lower processing fees compared to credit card payments

- Lower likelihood of fraud and chargebacks

- Convenient payment method for recurring payments

- Reduced failed payments

1. Lower processing fees

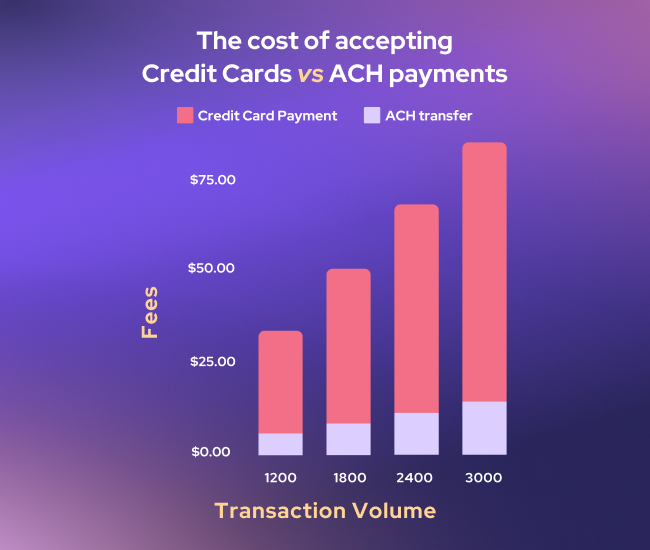

ACH payments typically range in cost from a lean 0.5%+ $0.25 to 1.0% + $0.75, depending on your payment processor. Compared to credit card payments, which cost around 2.5% or more per transaction, ACH payments are often less than half the cost.

2. Lower likelihood of fraud and chargebacks

Since ACH payments involve sharing intimate bank details, similar to a VOID cheque, they're not as vulnerable to theft as physical cards or breached data. There's no card information for thieves to swipe, and the data stays secure online. NACHA's security measures, like bank verification, provide extra safety for ACH payments.

When a credit card chargeback happens, you can try to dispute it. But if you lose, you'll be stuck paying fees of around $15, plus losing the original sale. This makes ACH network security a nice bonus as you don’t have to deal with chargeback.

Plus, it's easy to trace an ACH transaction, so you and your customer have peace of mind knowing the funds are secure, and your cash flow won't be interrupted.

3. Easier maintenance for recurring payments

With ACH payments, not only does it save you from tracking down your customer's new credit card details, but it helps prevent any service disruptions for them as well.

Do you know how annoying it is when your favorite streaming service suddenly stops working because your credit card expired? You have to track down your wallet, pull out your new card, and punch in the details using the remote and janky keyboard on the screen.

Think of it like setting up a direct deposit for your paycheck – once it's done, you're good to go without worrying about expiry dates. No more scrambling to update info, no more asking your customers to update their info. ACH payments keep your subscription service running smoothly.

4. Reduced failed payments

Even when customers have up-to-date credit card details, payments can still fail for many reasons. Maybe the card hits its spending limit, transaction limit, or credit ceiling. On the other hand, bank accounts usually have funds ready, making ACH payments less likely to fail.

Furthermore, since credit card transactions tend to be a little riskier than ACH payments, credit card networks, and financial institutions are more likely to flag a transaction for fraud and not authorize the payment. This issue occurs frequently especially when you suddenly process a larger transaction amount.

What types of businesses use online ACH payments?

ACH is widely used in industries that process large or recurring payments to avoid credit card fees. Here are some common industries that accept ACH payments with Helcim:

Tech and SaaS businesses have the highest ACH adoption, 9.99% of all transactions, likely due to recurring subscription models. Service-based industries (e.g., contractors, legal, and consulting firms) prefer ACH for high-value transactions.

How long does an ACH transfer take to be deposited?

You should budget for 3-5 days. Although accepting ACH payments are not quite as fast as credit cards, they have a higher rate of success and lower rates of fraud. Plus, they have lower payment processing fees.

Why is my ACH payment taking so long? ACH payments can be delayed due to bank processing times, weekends/holidays, or verification checks. If you are expecting a payment and it has been longer than five business days, contact the payer and ask them for an ACH trace I.D. lookup. You can pass this on to your payment provider to see if they can trace the ACH transaction for you to see what is happening within the ACH network.

Simply turn on ACH payments with Helcim and save

With Helcim, it's easy to accept ACH payments. You can collect ACH Payments using built-in tools free with your account.

Helcim will automatically generate payment agreements for customers to authorize, and you will receive the funds directly in your bank account within 3-4 business days. It's that easy!

P.S. You can also toggle on Helcim Fee Saver for tools like invoicing to prompt your customers to pay via ACH or accept a convenience fee for paying via credit card, saving you money on processing fees.

FAQs

What is required for ACH payment processing?

To process an ACH payment, you need the payer’s bank account number and routing number, along with their authorization to withdraw funds. This authorization can be given through an NACHA-compliant ACH authorization form.

What happens if an ACH transaction is not authorized?

Once you have authorization from your client or customers and you've sent their banking details to your payment processor or financial institution, the transaction will need to be verified through the ACH network. If the payment is not authorized, your payment processor will receive a decline code. This could be due to various reasons, although it is much less common than failed credit card transactions, including insufficient funds, suspected fraud, or the customer has reached out to cancel the transaction and revoke their authorization.

What is the best way to take ACH payments online?

The best way to take automated clearing house payments online is to use a payment processor that offers seamless integration tools, allowing you to accept ACH payments quickly and efficiently. With Helcim, you can easily toggle on ACH payments payment methods through our user-friendly dashboard to allow customers to pay with ACH using tools like invoicing, subscriptions, payment pages, and the virtual terminal.

How can someone pay me via ACH?

You can either have your business set up to receive direct payments (ACH credit transactions) or pull funds from customer's bank accounts (ACH debit) by having them provide their banking details. With Helcim, you can automate ACH transfers with tools like invoicing, recurring billing, and subscriptions or take one-time payments (great for larger B2B transactions) through tools like the Virtual Terminal.

Are online ACH payments the same thing as online bill payments?

ACH processing is a method of electronic payments that customers and businesses can use to pay their bills online. There are typically two methods available to customers to pay online or use for subscription services and products such as gym memberships, streaming services, and monthly subscription boxes: ACH bank transfers, which use your bank account details and pull funds directly from your checking or savings account, or credit card which is charged to your credit card balance.

{kind=link}