We've all been there. You send out an invoice, and you wait patiently for your money to come in. But then, a few days (or weeks) later, you get a notification that the ACH payment has been returned. What gives?

However don't worry, there are a few common reasons why this happens - and we'll go over them here (you can find a full list of ACH return codes linked in this article as well.) So next time it happens to you, you'll know what to do. P.S. We also throw in some helpful tips on how to avoid paying extra fees.

What is an ACH return?

An ACH return happens when your customer’s bank rejects the ACH payment you tried to pull from their account. When that happens, you will receive a return code that tells you why it failed, so you know what went wrong and what to do next.

What is the difference between ACH return and ACH dispute?

An ACH return occurs when a payment fails to go through. An ACH dispute, on the other hand, occurs after the payment goes through. The customer contacts their bank to report an unauthorized debit transaction they didn’t approve. In response, your bank may place a hold or issue an ACH reversal. Learn more about ACH disputes here.

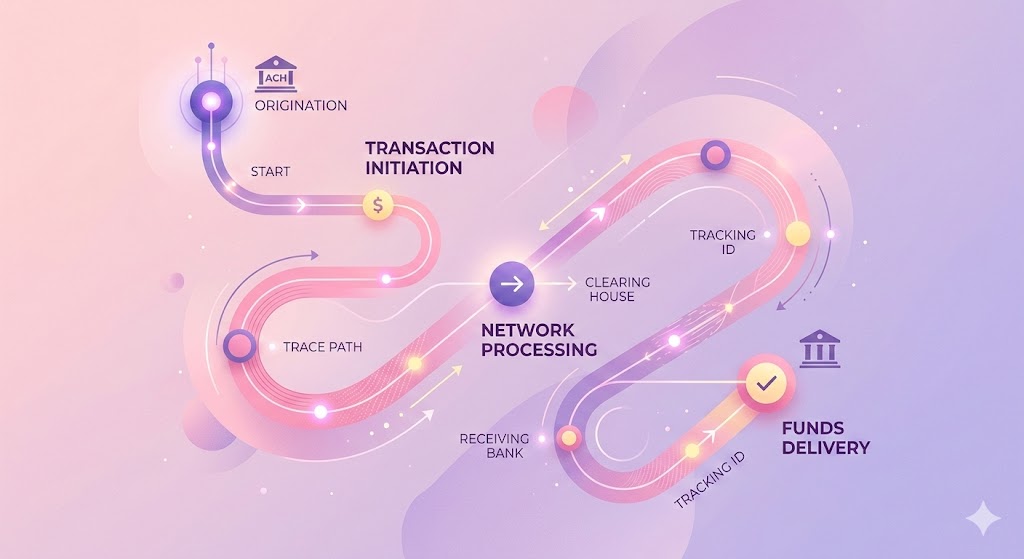

How does the ACH return work?

When you accept an ACH payment (for example: through a virtual terminal or invoice), the transaction still has to be approved by your customer’s bank. Behind the scenes, two banks help moving money in ACH network:

- The Originating Depository Financial Institution (ODFI) is your bank or your payment processor’s bank. It initiates the ACH transaction on your behalf.

- The Receiving Depository Financial Institution (RDFI) is your customer’s bank. It receives the request and decides whether to approve or reject the payment.

If something goes wrong, the RDFI rejects the payment and sends back an ACH return code to the ODFI. Your ACH processing company receives that code and passes it on to you. If you're using Helcim, you'll get a clear email or notification that includes:

- The return code

- An explanation of what went wrong

- What steps you can take to fix it

For example, if you get an R01 code, it means the consumer account didn’t have enough funds. Your transaction status will read something like: "This payment was declined due to insufficient funds. Please contact your customer or request a different payment method."

You’ll find the most common error codes below, or check out the full list of ACH return codes and their meanings here.

What are common ACH return codes?

Here are the most common ACH return codes, what they mean, and how often they show up:

- R01: Insufficient Funds appear 39% of the time

- R03: No Account or Unable to Locate Account appears 25% of the time

- R10: Customer Advises Not Authorized, Improper, or Ineligible appears 7% of the time

- R02: Account Closed appears 6% of the time

- R08: Payment Stopped appears 5% of the time

- R04: Invalid Account Number appears 4% of the time

- R16: Account Frozen/Entry returned per OFAC instruction appears 4% of the time

- R29: Corporate Customer Advises Not Authorized CCD appears 3% of the time

- R13: Invalid ACH Routing Number appears 3% of the time

- R20: Non-Transaction Account appears 1% of the time

U.S. merchants are likely to see around 37 common codes, while another 30 are more rare. In Canada, there are just 21.

With Helcim, you don’t need to memorize every code. When a payment is returned, you’ll get a clear error message and an email explaining what went wrong. We also act as the go-between with the customer’s bank to help you sort it out quickly.

If you run into a rare code or confusing message, we’re here to help. You shouldn’t have to waste time decoding bank language — your processor should make it easy.

What are the common reasons for an ACH return?

ACH payments are popular for their low cost. But just like credit card chargebacks, ACH returns are annoying and can disrupt your cash flow. The most common reasons for an ACH return include the following:

- Fraudulent transactions

- Insufficient funds in the customer’s account

- Invalid or mistyped account numbers or routing numbers

- Incorrect payee information, like a mismatched name

- Closed or non-existent accounts

- Authorization issues, such as the customer revoking permission

- Stop payment requests filed by the customer

- Uncollected funds or restrictions on the account

Every ACH payment must follow the NACHA operating rules (National Automated Clearing House Association), the group that oversees the ACH network. If something doesn’t look right, the ACH payment can get rejected and returned to protect merchants, payment providers, and consumers.

Although ACH transactions are considered both secure and safe, sometimes banks will flag ACH transactions as fraudulent. This is unsurprising considering ACH debits were the payment method impacted most in 2021, second only to checks, with a staggering 37 percent of all ACH transactions being fraudulent, according to a 2022 Payments Fraud and Control Report conducted by J.P Morgan.

How much is the ACH return fee?

Some payment processors may charge you an ACH return fee, $10 to $15. That’s on top of the regular processing fees, and it will show up on your monthly statement.

At Helcim, we charge $5 for each ACH return. But whether you pay the processing fee depends on when the payment is returned. For example, Helcim merchant charges a customer with a $100 purchase, and it has a $0.75 payment processing fee.

- If a $100 ACH payment is returned before settlement, your customer gets their money back, and you don’t pay anything, not even the $0.75 processing fee.

- If it’s refunded after settlement, your customer still gets the $100 back, but the $0.75 fee stays on your statement because the transaction was already processed.

Can you avoid ACH return fees?

Yes. If you cancel an ACH payment before the batch settles (usually within 1–2 business days), you can void the transaction without paying any fees, not even the processing fee. ACH payments take longer to process than credit cards or e-transfers, giving you a short window to act.

But once the payment settles, any cancellation is treated as a refund, and you’ll be charged the original processing fee, even if the full payment is returned to the customer. So if you catch an issue early, wrong account holder info, duplicate charge, etc. void it right away to avoid unnecessary fees.

What happens if I have too many ACH returns?

It is good to know that NACHA has a ACH return rate threshold on specific codes, such as 0.5% return rate for R05, R07, R10, R29, and R51. Violations of these limits may result in formal warnings or fines.

As a general rule, make sure that at least 85% of your bimonthly transactions are going through without return codes, and less than 1% of those are unauthorized.

Manage ACH returns effectively with Helcim

ACH returns can be frustrating, especially when they delay your payouts or leave you guessing about what went wrong. With Helcim, you get a simple explanation of the issue and what to do next.

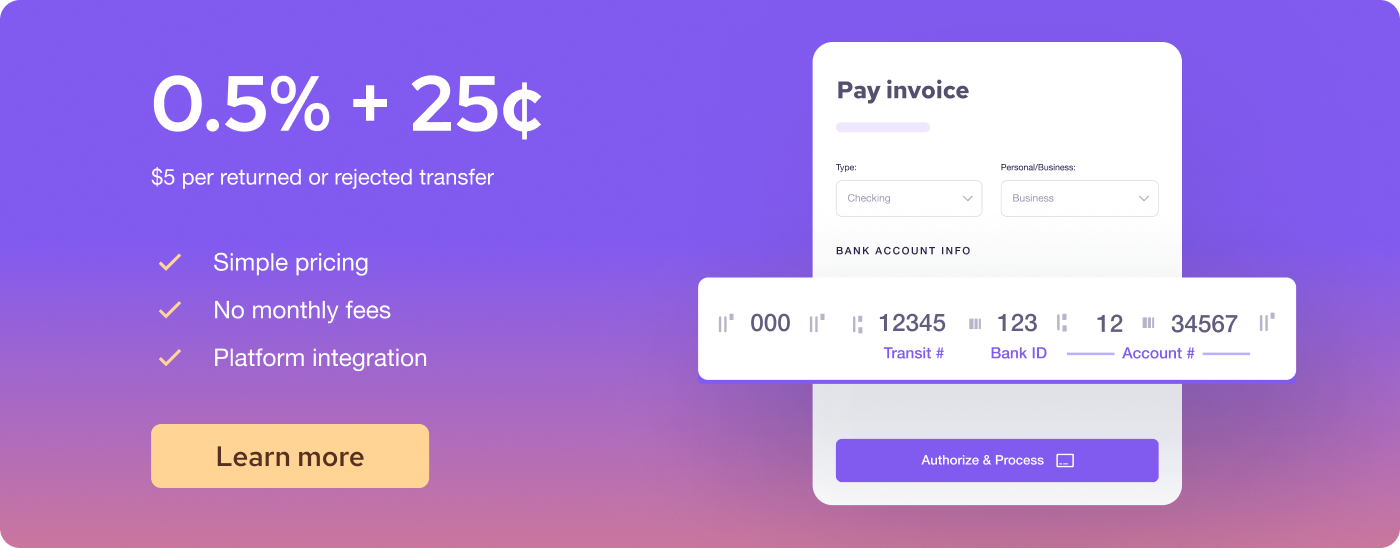

Sign up with Helcim to accept ACH payment at a low cost of 0.5% + 25¢ per transaction, capped at $6 for transactions below $25,000.

FAQ

Why am I being charged an ACH return fee?

Some payment processors charge a fee when a customer's bank rejects an ACH payment. This fee typically covers the cost of handling the failed transaction. It’s often added on top of your regular processing fees and shows up on your statement. Not all processors charge it — Helcim, for example, does not.

What are the risks of ACH returns?

ACH returns can delay your payouts, disrupt cash flow, and sometimes create extra work for your team. Frequent returns may also raise red flags with your processor or bank. If not handled properly, they can lead to lost revenue or strained customer relationships. That’s why it's important to catch and resolve them quickly.

Will an ACH go through with insufficient funds?

No — if your customer doesn’t have enough money in their account, the payment will be returned. This triggers a return code like R01: Insufficient Funds. You’ll be notified of the failure, and the customer will still owe the full amount. In most cases, you’ll need to request payment again or ask for an alternate method.

Who pays for the ACH return fees?

The merchant usually pays the ACH return fee, not the customer. It's charged by the processor and added to your monthly bill. However, some processors — like Helcim — don’t charge return fees at all. That’s something worth checking before choosing a provider.