Let’s be real—when was the last time someone got excited about ACH payments? It’s not exactly the stuff of dreams, but when it comes to getting paid (and keeping more of that hard-earned money), ACH payments are the unsung heroes. Sure, ACH transfers aren’t flashy, but they’re affordable and incredibly useful, especially if you’re running a small business.

If you’ve been shopping around for options for a while, this article might not have you jumping for joy (or maybe it does), but it will help you navigate the world of ACH providers and pick the best one for your business.

The 5 best ACH payment processing companies for US businesses

| ACH processing companies | Processing fees | Key Features | Ideal for |

|---|---|---|---|

| Helcim | 0.5% + 25¢ per transaction. Fee is capped at $6 per transaction | Recurring payments, Virtual terminal, Invoicing, SMS payments, Payment pages | Ideal for businesses that prefer low processing fees, no monthly fees, no contracts, and all the tools needed to collect ACH payments. |

| Stripe | 0.80% per transaction, Fee is capped at $5 per transaction | Invoicing, Payment links, Subscriptions | Ideal for businesses that want to integrate payments into their existing apps or systems. |

| Square | 1% per transaction with minimum fee of $1 | Square Invoicing, Square POS system | Ideal for omni-channel businesses or professionals who rely on invoicing. |

| GoCardless | Domestic transactions: 0.5% + 0.05 (capped at $5) to 0.75% + 0.05 (capped at $6.25), International transactions: 1.75% + $0.40 to 2% + $0.40 for international transactions | Recurring billing and subscription | Ideal for businesses that need recurring payments or a cross-border solution. |

| Rotessa | $17/month to $95/month depending on transaction counts 0.35¢/transaction for business process 250-1000 monthly transactions. Custom pricing for 1000+ monthly transactions | Recurring billing and subscription | Ideal for businesses that rely heavily on recurring ACH payments, or that process a steady volume of high-ticket transactions. |

1. Helcim

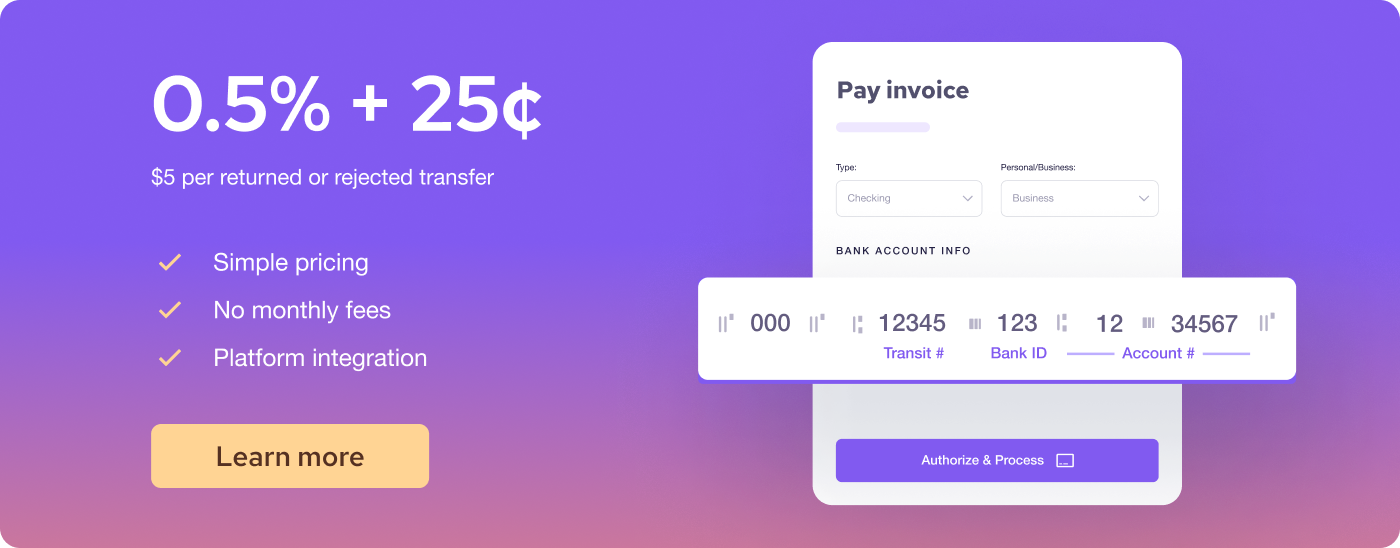

Helcim is a North American payments company offering ACH payments with no contracts, monthly fees, and affordable pricing. Helcim's ACH payment fee is 0.25% + 25¢ per transaction. The fee is capped at $6 per transaction for transactions below $25,000. Helcim also offers key features:

- Free-to-access payment tools: Recurring payments, virtual terminal (collect phone/mail orders, or collect overdue invoices faster), invoicing (one-time or recurring invoices), SMS payments, and payment pages.

- Customer portal: Easily view and manage your customer’s pre-authorized debit agreements.

- Integration: Integrates with Xero and QuickBooks Online.

- Processing time: ACH deposit times are settled within 3-4 business days.

Who is Helcim best for? Helcim is worth a serious look if you’re after transparent pricing, flexibility, and all-in-one convenience. With Helcim, you get both card and ACH payment options under one roof—no need to juggle multiple providers.

2. Stripe

Stripe is a major player in ACH payment processing and doesn’t require monthly fees or long-term contracts. It charges 0.80% per transaction, capped at $5. Stripe’s key features:

- Free-to-access payment tools: Invoicing, payment links, and subscriptions

- Integration: Advanced and customizable API for merchant developers

- Processing time: 3-4 business days. Faster 2-day settlement available for an additional 1.2% fee per transaction

Stripe is ideal for businesses that want to integrate payments into their existing apps or systems to help users get paid. Many payment apps use Stripe in the background, and platforms like Shopify integrate Stripe to let users collect payments online. If your business needs deep customization and you have developers on your team—or if fast access to funds is a priority—Stripe could be a great fit.

3. Square

Square’s been the go-to for micro and small businesses particularly retail shops and restaurants. The ACH feature on their Square Invoices is just another tool in their easy-to-use toolkit. If you’re already a Square fan, this is a great add-on. Square charges 1% per ACH transaction with minimum fee of $1 (capped at $10 for Invoice Plus users).

Key features:

- Free-to-access payment tools: Available on Square Invoicing and the Square POS system.

- Processing time: 3 to 5 business days. Faster 2-day settlement available for an additional 1.2% fee per transaction. Square offers next-business day deposit or Instant Transfer for 1.75% per transaction, available for transactions up to $10,000.

Why Square? It’s simple, straightforward, and a natural fit if you’re already in the Square ecosystem. You can easily extend your payment options by generating ACH invoices directly from your POS system—keeping everything under one roof without any extra hassle.

4. GoCardless

GoCardless is a UK-based fintech ACH payment processor specializing in recurring payments for subscriptions, memberships, or any other recurring billing needs. It has a tiered pricing plans

- Standard: 0.5% + 5¢ (capped at $5) for domestic, and 1.75% + $0.40 for international transactions

- Advanced: 0.75% + 5¢ (capped at $6.25) for domestic, and 2% + $0.40 for international transactions

Key features:

- Free-to-access payment tools: Recurring billing and subscription. Global payments capability across multiple countries.

- Integration: API integration with QuickBooks, Sage, and Xero.

- Processing time: 3-4 business days (2-day deposits included with the Advanced plan)

GoCardless is a great fit if your business runs on recurring payments and needs a cross-border solution. But be aware—international transactions can cost at least three times more than domestic ones. If you want advanced features like adding your business name to a customer’s bank statement or customizing the checkout experience, you’ll need to pay an extra $75 to $275 per month.

5. Rotessa

Like GoCardless, Rotessa specializes in recurring payments. Their platform is made to just process ACH payments for businesses with subscription models or regular billing cycles. Rotessa has volume-based tiered monthly rates:

- 1-10 Transactions: $17/month

- 11-50 Transactions: $39/month

- 51-100 Transactions: $65/month

- 101-250 Transactions: $95/month

- 250-1,000 Transactions: 35¢/transaction

- 1,000+ Transactions: Custom pricing

Key features:

- Free-to-access payment tools: Easy recurring billing with ACH only

- Integration: Integrates with Xero and QuickBooks Online

- Processing time: Deposit times are within 5 days of the process date

Why Rotessa? It’s ideal if your business relies heavily on recurring ACH payments, like memberships or subscription services, and only needs ACH. It’s also a smart choice for handling high-ticket transactions at a steady volume since their flat-rate pricing means you’re not paying a percentage of each transaction—keeping your costs predictable and under control.

How to choose the best ACH payment processor for you

Every ACH provider has its strengths and weaknesses. Some specialize in a specific payment need, while others offer a full suite of tools to support all kinds of businesses. To find the right one for you, start by asking yourself a few key questions:

- Will ACH processing fees impact my business’s profit?

- How do I want to collect ACH payments?

- How useful is ACH for my business?

- How quickly do I need to get paid?

- Will I need real human support?

1. Will ACH processing fees impact my business’s profit?

If your goal is to maximize profit, low ACH processing rates should be a priority. For example, Helcim charges just 0.25% + 25¢ per transaction, which is 10 times less than credit card processing fees. If you sell high-ticket products or services, the lower the fee, the higher your profit. Also, check whether a provider has contracts or hidden fees to avoid unpleasant surprises.

2. How do I want to collect ACH payments?

If you need multiple tools to collect ACH payments, Helcim offers everything from invoicing to virtual terminals. If you need only one specialized tool, like invoicing or subscriptions, Square, GoCardless, or Rotessa might be a better fit. Want a custom API integration to accept ACH payments directly from your app or system? Stripe is built for that.

3. How useful is ACH for my business?

ACH is an affordable payment method that works well in many situations. It’s especially popular among subscription-based and service-based businesses—like SaaS, law firms, consulting, and freelancers. But for fast-paced B2C environments like restaurants or coffee shops, ACH is less common than credit card transactions. It takes time to create NACHA authorization form and get a signature from your customers. Below are the top 10 industries that use ACH payments the most.

| Industry | Percentage of Transactions Paid with ACH (%) |

|---|---|

| Platforms Apps and SaaS | 8.91% |

| Organizations and Associations | 7.47% |

| Contractors Home Services | 6.14% |

| Professional Services | 4.53% |

| HotelsLodging | 4.49% |

| Financial Institution | 4.07% |

| Education | 3.73% |

| Transportation | 2.65% |

| Government | 1.69% |

| Wholesale | 1.63% |

4. How quickly do I need to get paid?

Patience is a virtue, but no one likes to wait too long for their money. Some providers are slow, while others offer faster deposits. Square and GoCardless, for example, have quicker funding options for faster cash flow with extra fees. Just make sure to check the fine print: faster deposits often mean extra fees.

5. Will I need real human support?

When things go wrong, you want more than a chatbot sending you in circles. Look for a provider with live support options. For example, Helcim offers phone, video, and email support so you can solve problems fast. Bonus points if the platform is easy to use without needing a tech degree.

ACH payments may not be flashy, but they’re a powerful tool for accepting payments efficiently and affordably. Whether you’re looking to streamline your recurring payments without handling credit card transactions, process large transactions, or just save on fees, choosing the right provider can make a world of difference. Take your time, evaluate your options, and pick the one that aligns best with your business needs.

Ready to start accepting ACH payments for your business?

Sign up with Helcim today, no monthly fees, no contracts, just affordable ACH payments and more at your fingertips. Or, get access to other helpful content such as authorization templates and materials to educate your customers about ACH with our complete guide below.

FAQs

What are the best ACH processing companies should small businesses use?

Small businesses should consider ACH providers like Helcim, Stripe, Square, GoCardless, or Rotessa based on their needs. Helcim is great for all-in-one tools and low fees. Stripe is ideal for businesses with developer resources, while GoCardless and Rotessa are strong choices for recurring billing. Compare fees, tools, and contract terms before choosing.

What are the two major ACH networks in the US?

The two major ACH (automated clearing house) networks in the U.S. are the Federal Reserve’s FedACH and The Clearing House’s EPN (Electronic Payments Network). Both handle the secure transfer of funds between customer's bank accounts to merchant accounts. FedACH is used by the Federal Reserve Banks, while EPN is privately operated. Together, they power most ACH transactions in the country.

Who processes ACH transactions?

ACH transactions are processed by banks or third-party payment processors (TPPPs) acting as intermediaries. These include companies like Helcim, Stripe, or GoCardless. They work with the ACH networks to initiate, receive, and settle payments. Businesses don’t deal with the networks directly—they rely on these processors to handle everything.