ACH transfers might sound like another financial jargon reserved for accountants, but they’re actually a powerful alternative to credit card payments for business transactions. From payroll to subscription billing, ACH payments offer businesses like yours a more cost-effective way to handle money transfers—faster, secure, and more efficient than checks or cash. But even this reliable system isn’t immune to occasional hiccups - enter ACH disputes.

In this guide, we’ll dive deep into ACH disputes—what they are, how they work, and what steps you can take to prevent and manage them effectively as a business owner. Whether you’re new to ACH or looking for an advanced playbook, this guide has you covered.

Nailing down the basics: What is ACH and how does it work?

ACH stands for Automated Clearing House, a U.S.-based electronic network that processes payments and money transfers between banks. Canada has a similar system called electronic funds transfer (EFT). Both operate quietly behind the scenes, handling billions of transactions annually.

ACH transactions occur in batches as banks communicate through the ACH network to process payments, either debiting or crediting accounts. These ACH transfers eliminate the need for physical checks or in-person bank visits. If an ACH transfer is deemed unauthorized or incorrect, it can be contested through the ACH network by following specific dispute procedures.

Types of ACH transactions

There are two primary types of ACH transactions: ACH credits and ACH debits. The key difference between them is how the money flows between accounts—whether it’s being sent or pulled.

- ACH credits: Money sent to an account (e.g., direct deposits or refunds).

- ACH debits: Money pulled from an account (e.g., utility bills or gym memberships). ACH transactions are commonly employed for recurring payments and subscription services, allowing merchants to manage automated billing while minimizing chargebacks and disputes.

For businesses, accepting ACH payments are common for recurring billing, vendor payments, and subscription services. With lower fees compared to credit cards and the ability to schedule payments seamlessly, ACH ensures businesses can manage cash flow efficiently while minimizing administrative overhead.

Benefits of using ACH payments

As we have mentioned earlier, Automated Clearing House (ACH) payments offer several advantages to business owners. From direct deposits to e-commerce transactions, ACH payments offer flexibility and convenience for a variety of business needs.

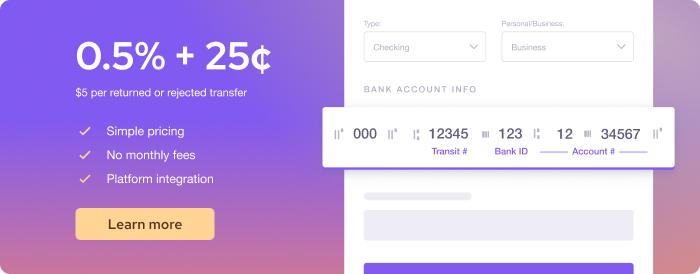

- Lower costs: Processing ACH payments is significantly cheaper than credit card transactions, with fees typically ranging from $0.20 to $1.50 per transaction or a small percentage of the payment, depending on your provider. Helcim charges 0.5% + 25c per ACH transaction and has a cap of $6 for transactions up to $25,000. This makes ACH an attractive option for businesses looking to reduce payment processing expenses especially for big ticket items.

- Recurring payment reliability: ACH payments have no expiration dates or dependency on factors like expiring credit cards, making them the ideal choice for subscriptions and long-term billing. This ensures uninterrupted service and fewer payment failures.

- Security and reliability: ACH transactions are processed through a highly secure network, reducing fraud risks compared to other payment methods. Built-in safeguards, like encryption and authorization requirements, provide peace of mind for both merchants and customers.

What is an ACH dispute?

Now that we’ve covered the basics of ACH payments, let’s talk about when things go sideways: ACH disputes. These occur when a customer essentially says, “I didn’t approve this transaction!” and reports it to their bank. This triggers your bank to put a hold on the payment that was headed to your account, creating a roadblock in your cash flow. While disputes are more common in credit card payments, they can just as easily happen with ACH transactions. When they do, they not only disrupt your cash flow but also require a well-documented and timely response to resolve effectively.

- If you lose an ACH dispute, the funds get pulled from your account and sent back to the customer. On top of that, you’ll probably face an ACH return fee from your payment provider. And here’s the kicker—losing too many disputes, whether ACH or credit card chargebacks, can ding your business’s reputation. Payment providers might start flagging your account, delaying deposits, or scrutinizing your transactions more closely, which no one wants.

- If you win, the money stays in your account, and the dispute gets resolved in your favor. Defending a dispute successfully not only saves you from losing cash but also shows payment providers you’ve got your act together, helping to keep things running smoothly in the future.

Types of ACH disputes

Before diving into resolution, it’s essential to identify the specific type of ACH dispute you’re dealing with. Different dispute types may require distinct approaches and specific supporting documents to resolve them effectively.

ACH disputes can be categorized into several types, each governed by the National Automated Clearinghouse Association (NACHA)’s detailed rules. Understanding these distinctions is crucial for merchants to navigate the process efficiently and provide the right evidence for a successful resolution.

- Unauthorized transactions: Payments made without the customer’s consent (learn how to prevent ACH frauds).

- Incorrect amounts: Overcharging or errors in the payment total.

- Duplicate transactions: The same payment is processed more than once.

- Non-receipt of goods or services: Payment was made, but nothing was delivered.

- Reversal errors: Mistakes during the reversal of a transaction.

- Canceled or revoked authorization: Payments processed after the customer canceled or withdrew their approval.

- Inaccurate account information: Errors caused by incorrect bank account details.

Invalid reasons for ACH disputes

It’s one thing to know the types of disputes out there but it’s equally important to know that not all disputes are valid under NACHA rules. Occasionally, customers may attempt to exploit the system by disputing legitimate transactions. Invalid reasons include:

- Buyer’s remorse: Regretting a purchase after the fact.

- Personal grievances: Disputes unrelated to the transaction itself.

- Delivery delays: Delays that don’t qualify as non-receipt.

- Avoiding payment: Filing a dispute to avoid paying for goods or services received.

- Forgetting a payment: Disputing a transaction due to memory lapses.

Recognizing these invalid reasons helps merchants address disputes efficiently and reduce unnecessary complications and refunds. Additionally, managing fraudulent ACH returns involves strategies such as engaging with customers, potentially hiring legal representation, and optimizing the order-to-cash process to minimize disputes and claims.

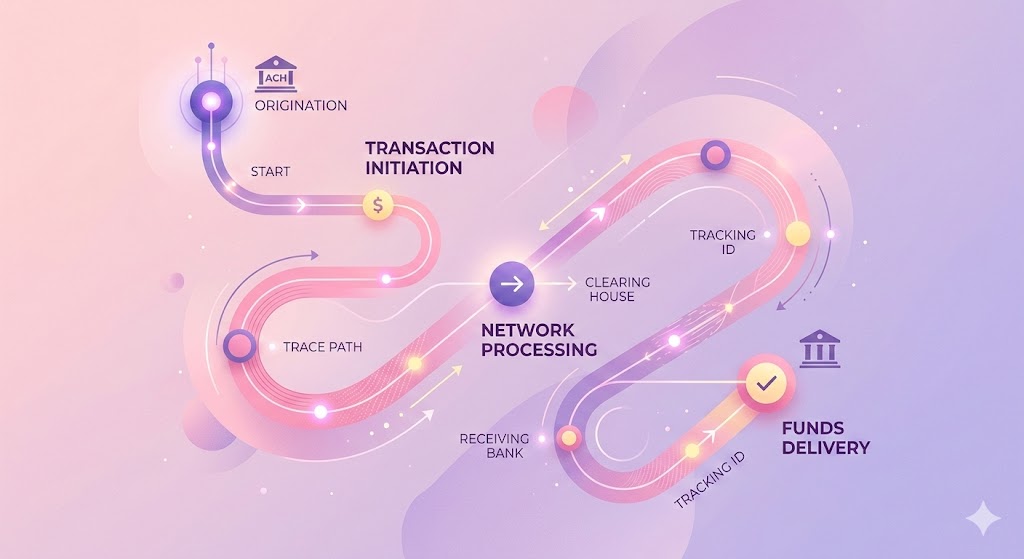

How does the ACH dispute process work?

Understanding the ACH dispute process is essential for resolving issues effectively. Here’s a breakdown of the key players and steps involved.

Key players

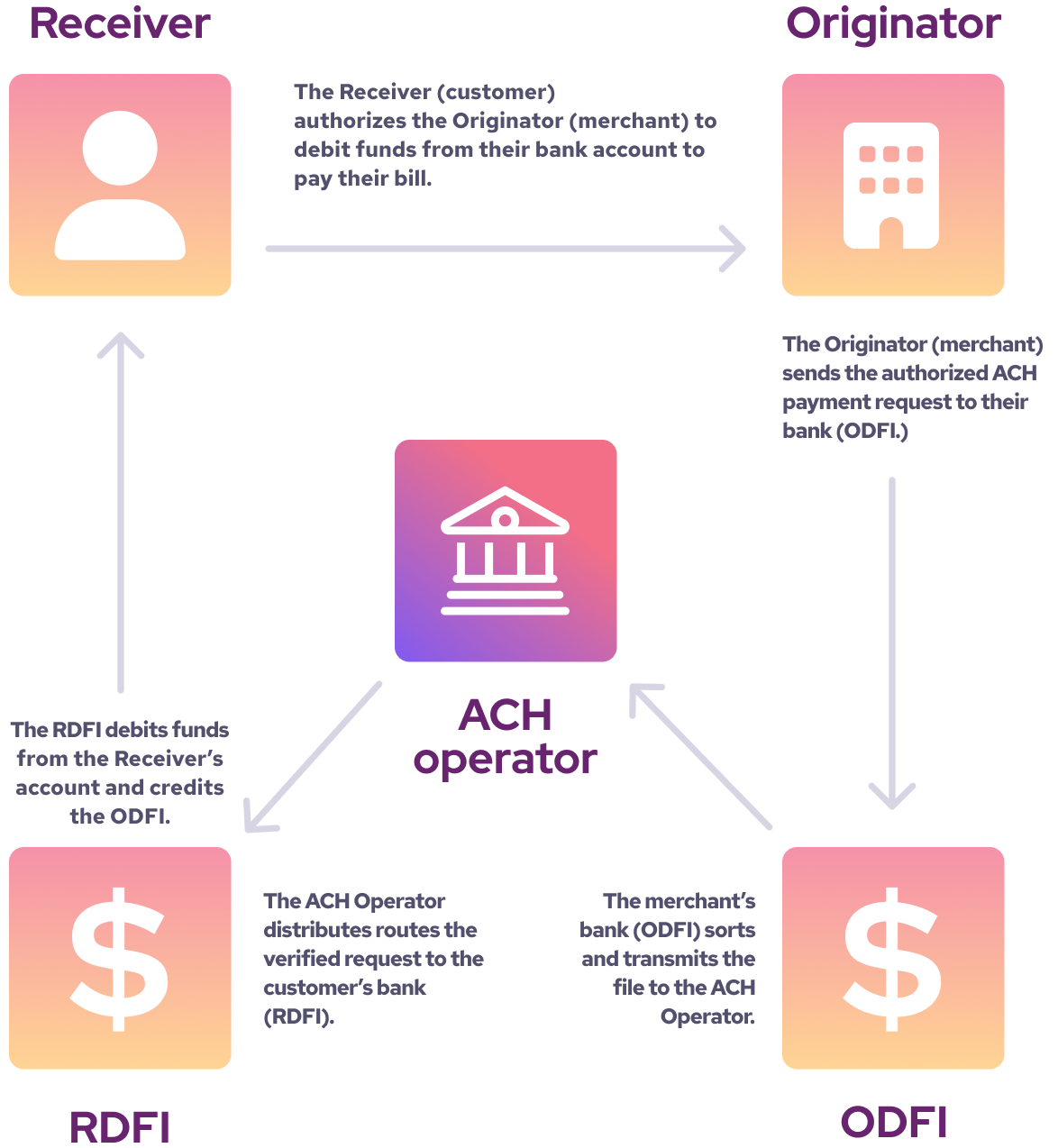

- Originating Depository Financial Institution (ODFI): Your bank or payment processor, requesting the payment.

- Receiving Depository Financial Institution (RDFI): Your customer’s bank where the fund requested will be taken from.

- NACHA: The governing body that oversees ACH operations and provides guidelines for dispute filing and resolution.

Steps in the dispute process

- Customer files a dispute: The process begins when a customer contacts their bank (RDFI) to dispute a transaction.

- RDFI notifies the ODFI: The customer’s bank informs your bank or payment processor about the dispute.

- Merchant provides evidence: As the merchant, you’ll need to submit supporting documentation, such as proof of authorization, delivery confirmation, or any other relevant evidence.

- Bank investigation: The RDFI reviews the case, evaluates the evidence, and determines the outcome based on NACHA guidelines.

- Resolution: If the dispute is upheld, the funds are returned to the customer, and you may incur an ACH return fee. If the dispute is resolved in the merchant's favor, the funds remain in your account, and the dispute is closed. The customer’s bank will notify them of the outcome.

Timeframes for ACH disputes

The most critical aspect of handling an ACH dispute is sticking to the timeline. Miss that golden window, and you’re essentially waving goodbye to your money while also risking a fund hold from your payment processor.

- For customers: Customers generally have 60 days from the transaction date to initiate a dispute.

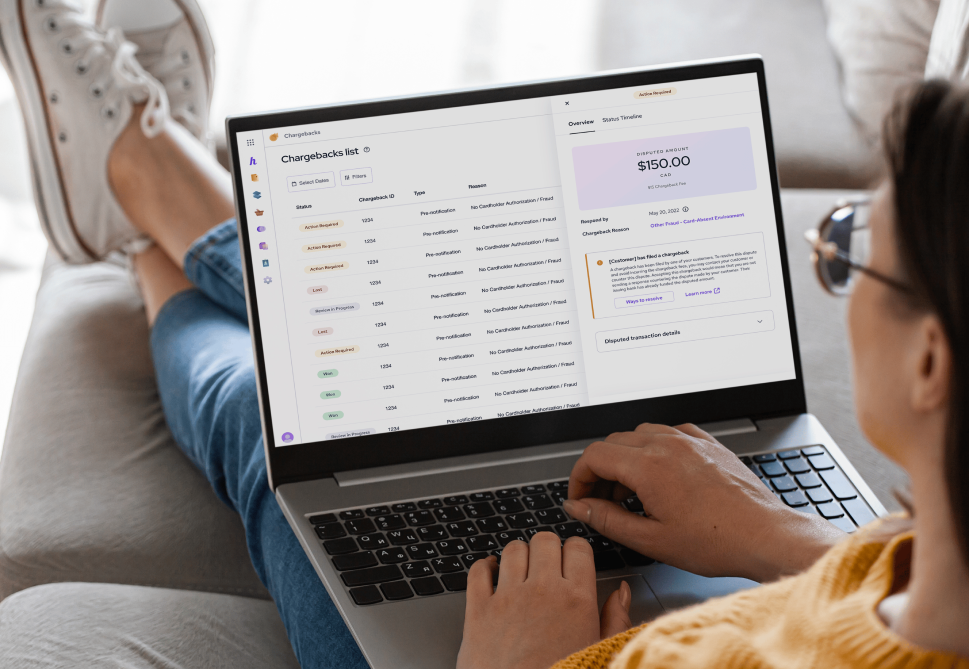

- For merchants: You typically have 10 business days to respond to a dispute notice with supporting evidence. Some payment providers, like Helcim, can have an intuitive chargeback handling process for ACH disputes that shows timelines and the required actions at each step.

How to determine if you're encountering an ACH dispute or something else

Your payment provider will usually let you know if a contested transaction is a credit card chargeback or an ACH dispute, but it’s always helpful to understand the differences yourself. Navigating payment reversals can get tricky, especially with terms like ACH disputes, ACH returns, and credit card chargebacks being tossed around. Here’s a clear breakdown to help you tell them apart:

ACH dispute vs. ACH returns

- ACH dispute: Initiated by the customer, typically due to unauthorized or erroneous transactions.

- ACH return: A reversal caused by issues like insufficient funds, duplicate payments, or incorrect account details.

ACH dispute vs. credit card chargebacks

ACH disputes:

- Governed by NACHA rules.

- Managed directly by banks (RDFI and ODFI).

- Less costly but offer fewer consumer protections.

- Handled by card networks like Visa and Mastercard.

- Provide stronger buyer protections but come with higher fees for merchants.

Preventing ACH payment disputes

Preventing disputes is always better than resolving them. By taking proactive steps, you can minimize the risk of disputes while maintaining smooth payment operations. Here’s how:

- Use reliable payment processors: Platforms like Helcim offer transparent pricing, robust tools for fraud detection, and built-in dispute management features to help you catch issues before they arise. With Helcim, you can also benefit from exceptional customer support, ensuring you’re never left to navigate disputes alone.

- Obtain explicit authorization or PAD agreement: Always require clear customer approval for ACH transactions, whether it’s a signed agreement or a digital consent form.

- Verify bank account information: Double-check routing and account numbers to ensure accuracy before processing payments. Small errors can lead to big problems.

- Communicate clearly: Notify customers of upcoming payments—especially recurring charges—to avoid surprises and ensure a smooth billing experience.

Looking for more tips on ACH payment best practices to prevent disputes? Download our comprehensive guide and user-friendly ACH templates below to simplify your process.

How to respond to an ACH dispute

When an ACH dispute arises, quick and decisive action can make all the difference. Here’s how to effectively handle the situation and protect your business:

- Review the dispute: Start by understanding the root cause of the customer’s challenge. Was it a misunderstanding, an error on your end, or a potential case of fraud? Carefully review the dispute details provided by your payment processor or bank to ensure you address the issue accurately.

- Gather evidence: Documentation is your best defense. Collect all relevant materials that validate the transaction, such as signed authorizations, invoices, proof of delivery, or communication records. For recurring payments, include signed agreements or any notification sent to the customer about the charges. Make sure your evidence is organized and directly addresses the claim.

- Submit your response: Provide the required documentation to the Originating Depository Financial Institution (ODFI) within the specified timeframe (typically 10 business days). Ensure that your response is complete and concise to avoid delays or follow-up requests. The faster you respond, the better your chances of resolving the dispute in your favor.

- Communicate proactively (if applicable): If the situation allows, consider reaching out to the customer directly to clarify the issue. This can sometimes lead to an amicable resolution without further escalation.

- Prevent future issues: Treat each dispute as a learning opportunity. Identify patterns or gaps in your processes that may have contributed to the dispute, and refine them to minimize the risk of future issues. This could include improving how you obtain customer authorizations for future pre-authorized transactions, enhancing communication about billing, or tightening internal review processes.

Final thoughts: Confidently managing ACH disputes

ACH payments are vital for running a modern business, but disputes can occasionally disrupt your operations. By understanding the process, implementing preventive measures, and responding promptly to disputes, you can protect your cash flow and maintain customer trust.

With the right strategies and tools, ACH disputes become manageable—a small bump in the road to smoother transactions.

Ready for a better ACH experience?

Want a payment provider that offers ACH payments with an intuitive chargeback management system? Sign up with Helcim for free!

With Helcim, you get:

- Lower rates for your ACH payments, helping you save on every transaction.

- An easy-to-use chargeback navigation platform to streamline the dispute process.

- A dedicated support team to guide you through these tricky situations so you're never left in the cold.

FAQs

Can a business dispute an ACH payment?

While most disputes are initiated by customers, businesses can challenge certain ACH transactions if they suspect fraud or errors in the payment process.

What happens if I miss the deadline to respond to an ACH dispute?

If you don’t respond within the required timeframe (typically 10 business days), the dispute may automatically resolve in favor of the customer, and the funds will be reversed.

Can ACH disputes be resolved without reversing the payment?

Yes, if the merchant provides sufficient evidence that the payment was authorized or valid, the dispute can be resolved without reversing the funds.

How can I track the status of an ACH dispute?

You can monitor the status of an ACH dispute through your bank or payment provider, which acts as the Originating Depository Financial Institution (ODFI) in the process.

What evidence is most effective in resolving an ACH dispute?

Signed authorization forms, proof of delivery, receipts, and agreements outlining the terms of the transaction are strong evidence to support your case.

Can disputes occur with recurring ACH payments?

Yes, customers can dispute recurring ACH payments if they claim the authorization was revoked or canceled, even if the merchant continued processing them.

Are there penalties for excessive ACH disputes?

Merchants with frequent disputes may face higher fees, stricter monitoring, or even suspension of their ACH processing privileges from their payment processor.

What happens if a dispute involves fraudulent activity?

If fraud is involved, the customer’s bank may expedite the reversal, and additional measures, such as law enforcement involvement, may be taken depending on the severity.

Can disputes be resolved amicably between the merchant and customer?

Yes, resolving disputes directly with the customer can save time and prevent escalations. Communicating proactively and offering refunds or solutions may prevent formal filings.

Does the same process apply to ACH disputes across all banks?

While the basic process is governed by NACHA rules, specific timelines and procedures may vary slightly between banks, so it’s essential to understand the policies of your payment processor and financial institution.