Back to Blog

Product Announcements

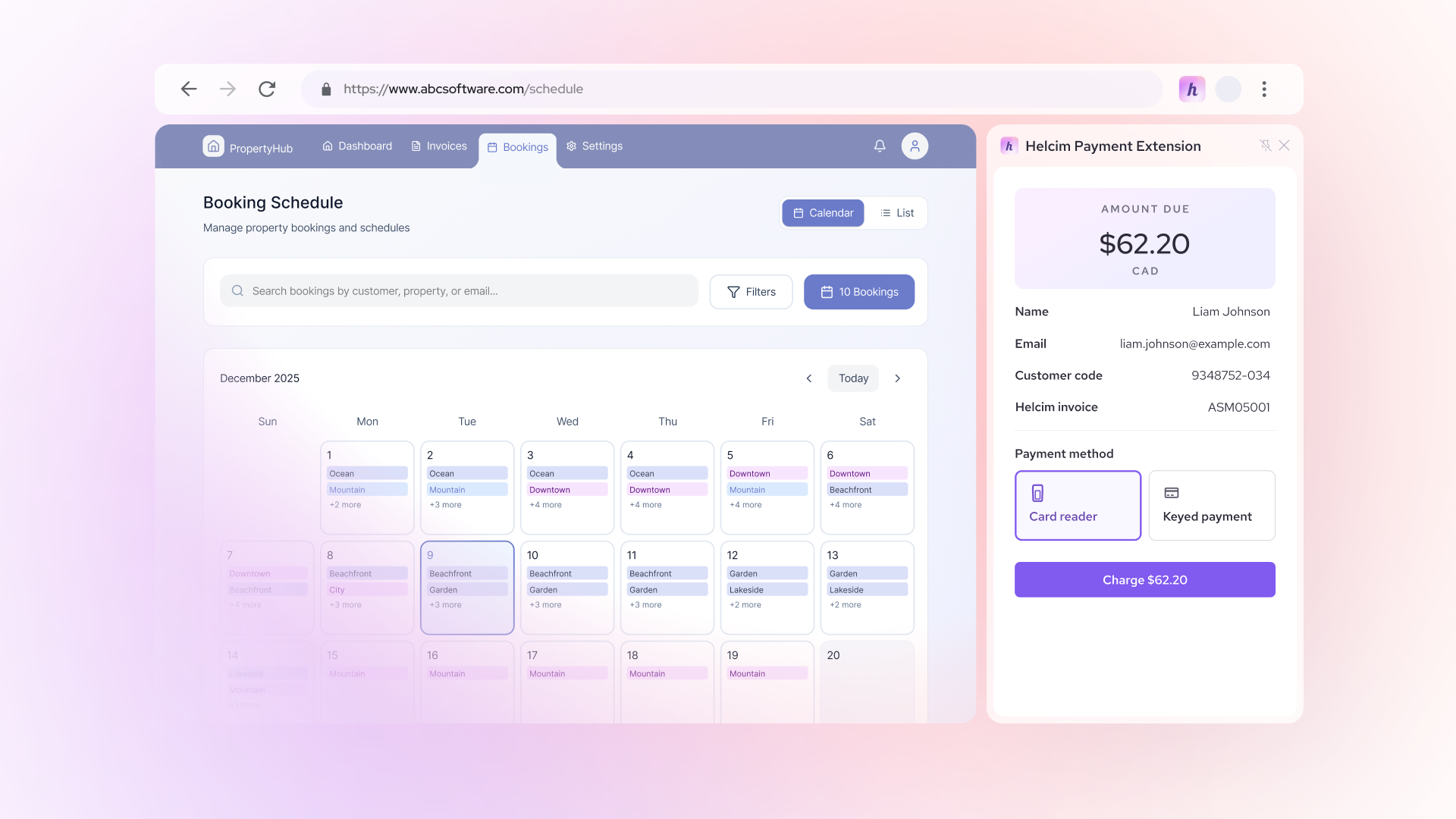

Meet the Payment Extension: Easy payment integration for the software you love

May Montenegro

Meet the new Helcim Smart Terminal

Nic Beique

Introducing Helcim Faster Deposits

Nic Beique

Helcim Bug Bounty Program Suspension Announcement

Thomas Llewellyn

Introducing Helcim Recurring Payments: Your payments on autopilot

Nic Beique

Introducing Tap to Pay on iPhone: Now available on the Helcim Point of Sale app

May Montenegro

Get ready for gross… deposits!

Nic Beique

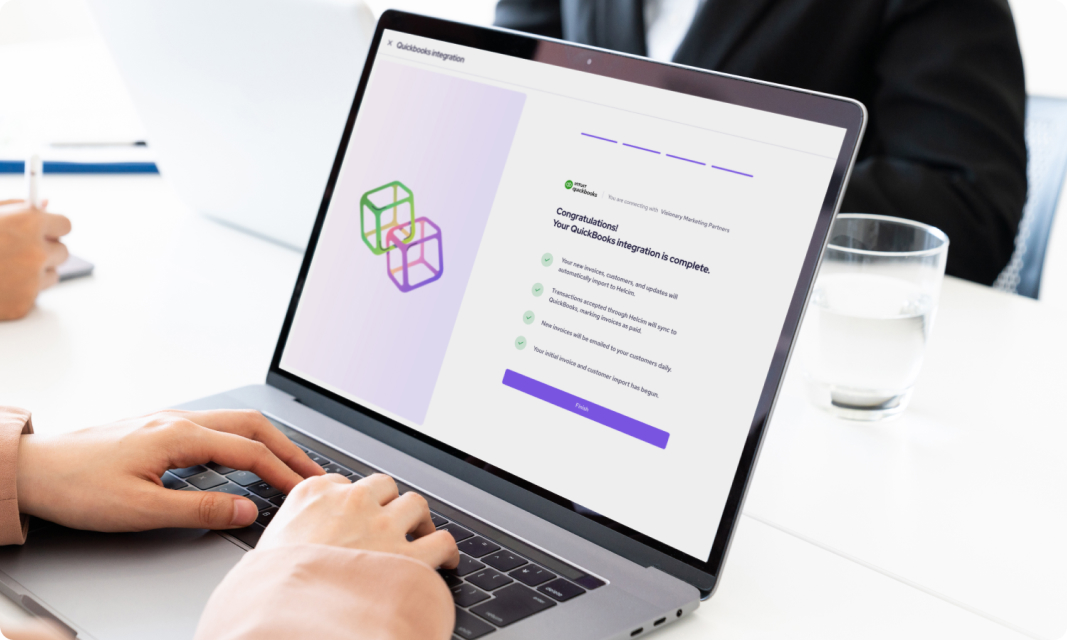

Introducing Helcim Automated Invoice Payments for QuickBooks Online

Nic Beique

Introducing Helcim’s Merchant Buyout Program

Nic Beique

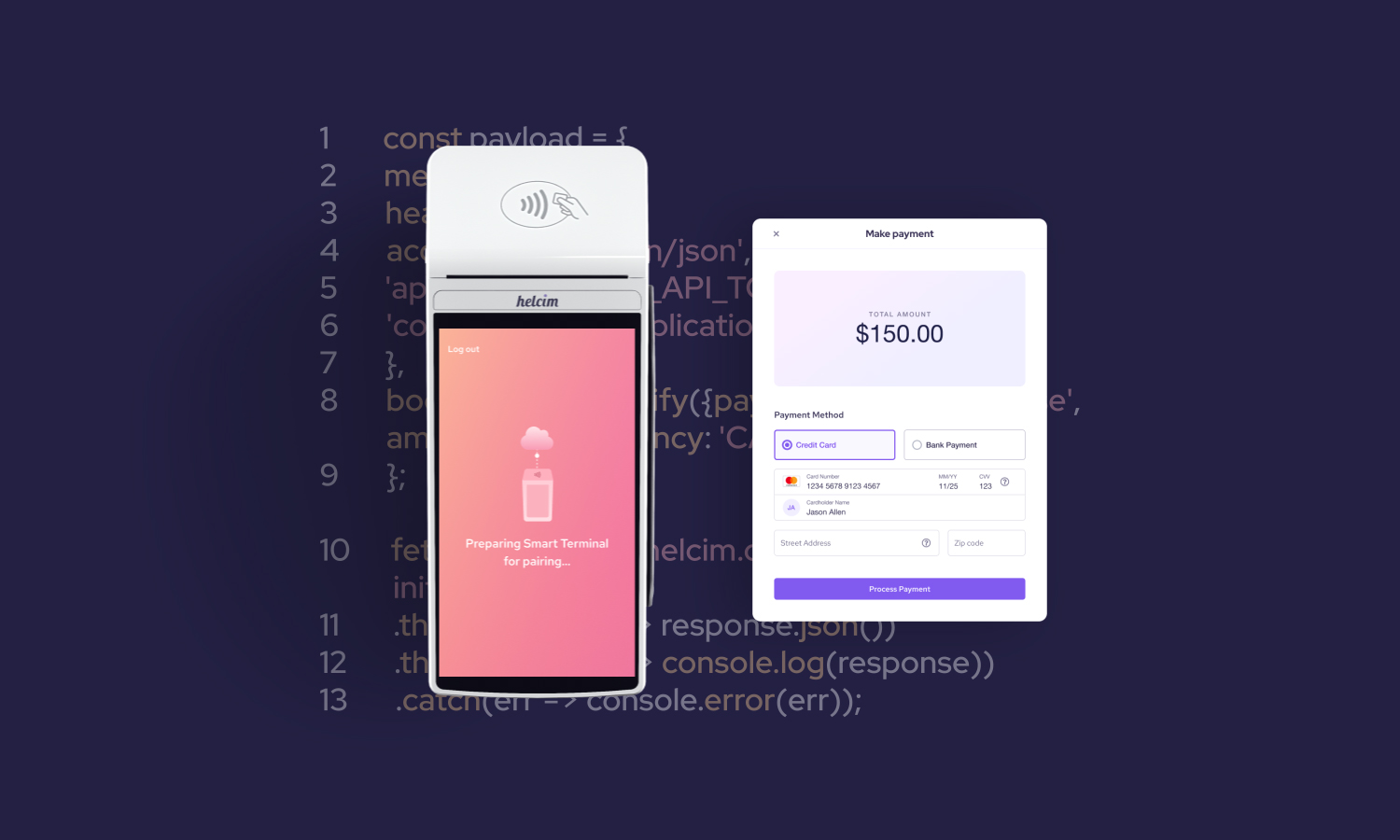

Introducing Helcim Integrated Payments for Developers and Platforms

Nic Beique

Creating Helcim's Online Checkout: A Product Manager's Tale

Ryleigh Stangness

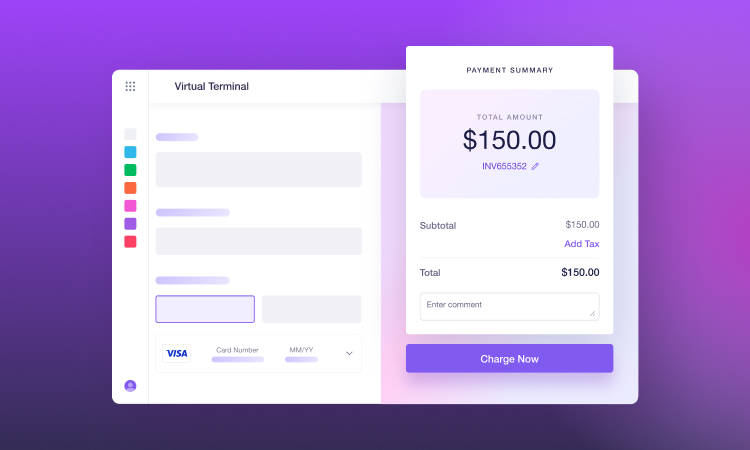

What's new for the Helcim Virtual Terminal?

Ryleigh Stangness

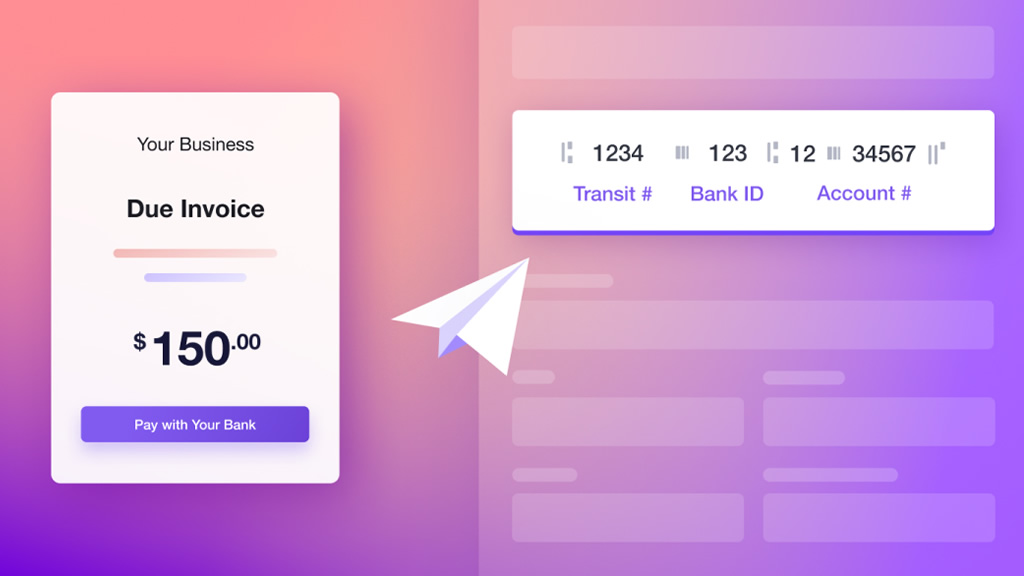

Welcome to Helcim ACH Payments

Danny Randell

Android Pay (Now Google Pay): What You Need To Know

Ryleigh Stangness

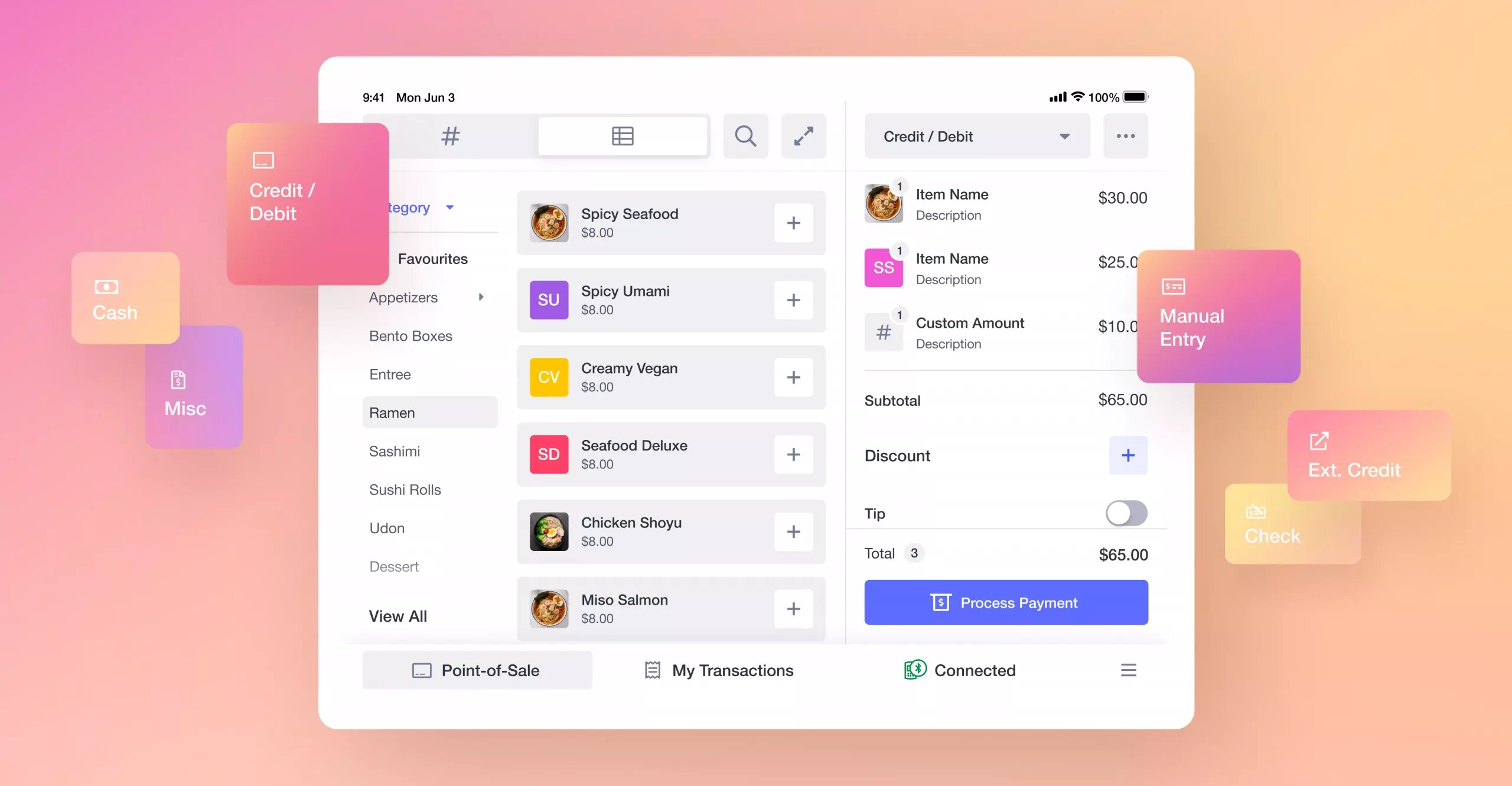

The All New Helcim POS

Danny Randell