Buy now, pay later services offer an alternative to financing purchases with a traditional credit card, but how different are they really? And is BNPL a good idea?

The debt structure of credit cards

You can tap your credit card at a dozen different places in a day, and do that all month long without having to actually pay a single penny to anyone. That's because everything you've "purchased" over the last month is on credit; meaning it's on loan to you from your bank.

Here's how credit card processing works: your bank has paid the businesses you've patronised out of their pocket and given you a credit, but they expect you to put those funds back into their pocket by the end of the month.

Now when your statement is due, all you need to do is take the amount you owe and forward it from your bank account to your credit card company or financial institution. Easy enough, right? The problem lies in when people use their credit card like a debit card, and treat their credit limit like additional funds in their bank account. Because if for some reason (like not having money in your actual bank account) you don't pay your statement in full at the end of each month, you incur what's known as interest on the amount owing.

Paying off Your credit card

Of course, credit cardholders can make what's known as a minimum payment each month to keep their credit score in good nick and the credit card companies happy, but the interest on the debt you now owe is cumulative"¦meaning that if you only pay the minimum payment every month it will take you months, or perhaps even years to pay off a single month's expenditures, and you'll end up paying hundreds of dollars in interest to your card issuer. Over time, this interest can cost you more than the original purchase price of the items you bought with your credit card if left unattended to.

The debt structure of BNPL services

Buy now, pay later services are structured a bit differently than traditional credit card offerings, and it's part of the reason why BNPL companies have been taking off recently. But how exactly are they different? You're still buying things on a sort of credit, right? Is there interest? How do these companies make money?

There are a host of questions that arise when people look at what BNPL services are doing in the payments space, but a quick look at their business model reveals that these guys noticed a gap in the payments market and they are currently filling it in a big way.

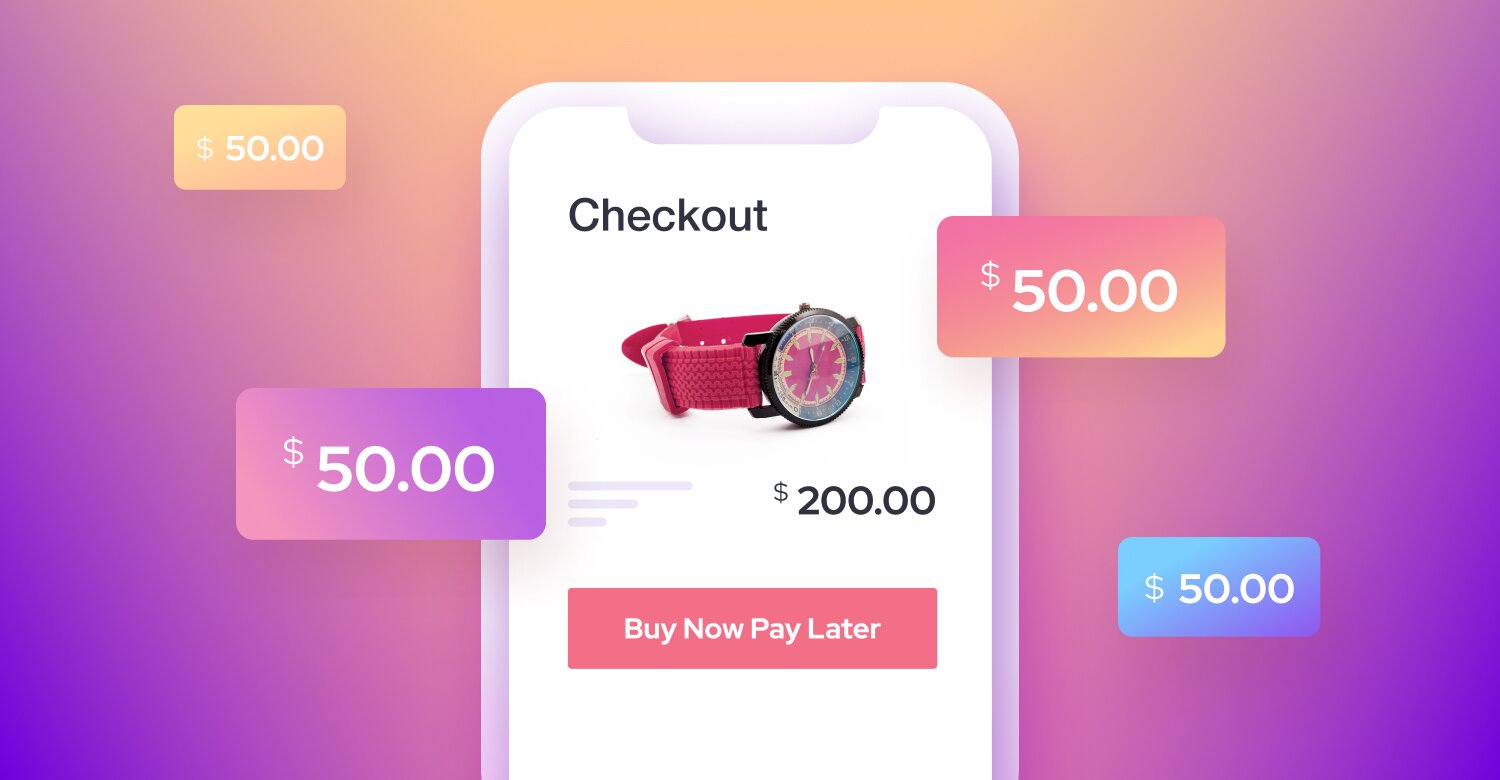

Buy now, pay later differs from company to company (much like credit cards do) but in general-unlike credit cards-BNPL services are financing services whereby users pay for individual items in installments. And usually, those installments don't cost you any more than if you had paid for the item all at once upfront. Usually.

Now if you don't meet your payments schedule as set out in the terms of your agreement with your BNPL provider, you may incur late fees, or eventually even interest, so it's not a freebie. But if you can stick to your payments schedule (often bi-weekly for six or eight weeks) you'll end up paying for a large purchase over time with no additional interest, and you'll have benefitted from additional cash flow over the length of your payment plan as opposed to if you had dropped a large sum of money on something upfront.

So what's the catch? Well the primary way BNPL services make money is through high processing fees. So if you're a business owner excited by the thought of selling more of your high-priced items in partnership with a BNPL provider, you may want to consider how this free service for customers is only made possible by merchants willing to opt-in for higher processing fees; which can sometimes be as high as 6% on a purchase (on top of your payment processor's fee).

Financing your purchases

Retailers have generally always been willing to accommodate consumers with financing and loans-for a price-oftentimes, it's anything to make a sale and get their products into consumers' hands. But while financing has its benefits (like ongoing cash flow, less of a bank account drain upfront, and the ability to purchase things that might otherwise be unaffordable), it also comes with its drawbacks; namely, paying interest, and having to make payments over a long period, rather than just paying for something once in full and being done with it.

While financing with a BNPL service won't come with interest if you pay in the specified grace period (the same goes for credit cards), you will need to concern yourself with the ongoing payment schedule, and be prepared for payments to keep being charged to your account until you've paid off your entire purchase. In many cases, if you miss a payment, you'll be barred from making future purchases until you're no longer in arrears.

How much debt is too much debt?

One of the arguments levelled against BNPL services is that they enable consumers who already misuse their credit cards and overspend to continue spending even more with the help of buy now, pay later; however, this doesn't seem to be the case. Most BNPL services require purchasers to undergo a soft credit check before they can use the service, and they seem to ensure customers have the funds necessary for the purchase they want to make.

That being said, BNPL isn't debt-proof-far from it-if you fail to repay a BNPL company on time, you could face late fees, interest fees, and eventually, have your information sent to a collections agency. Because while BNPL providers rarely report on-time payments to credit bureaus, late payments can get recorded and passed on (you'll need to check with whichever BNPL company you're considering signing up with).

If you want to know more about the individual buy now, pay later companies that are out there, check out this article.

So should I use buy now, pay later?

If you've got bad credit and are turning to a BNPL company to help you pay for things you otherwise couldn't afford, you may want to reconsider signing up with one. You can further damage your credit score and land yourself in a load of debt if you're not careful.

On the other hand, if you don't see any reason why you shouldn't be able to make your BNPL payments on time, and you are merely using it to soften the blow of a large purchase, then the service could be right for you.

Final thoughts

Ultimately, it doesn't look like BNPL is going to be ushering credit cards out the door, but rather, there is likely a place for both short term loan services in the market. It's important to remember that both tools are debt financing tools but with different applications; and when used responsibly, they can help with cash flow and big purchases.