-

Content

We’ve all experienced it one time or another: standing at the checkout, ready to pay, only to see those horrifying words on the card reader’s screen "credit card declined.” When your customers experience a declined credit card payment, it’s not just a potential missed sale, it’s an awkward moment that can catch both of you off guard.

As a business owner, you’ve probably experienced a failed transaction as a customer yourselves—so you can relate to how it feels from both sides of the counter. Approaching these unfortunate situations with empathy and professionalism will help keep your customers comfortable while protecting your business from missed sales. This guide will walk you through the common reasons for credit card declines, how to tell a customer without losing their trust, and ways you can keep the amount of credit card processing declines your business experiences to a minimum.

Common culprits of credit card declines

When a declined transaction occurs, it can feel like a mystery for everyone involved. And while the customer might suspect there’s something wrong with their credit limit or bank account, there are actually plenty of reasons that could explain a declined card. Here are a few culprits that come up more commonly.

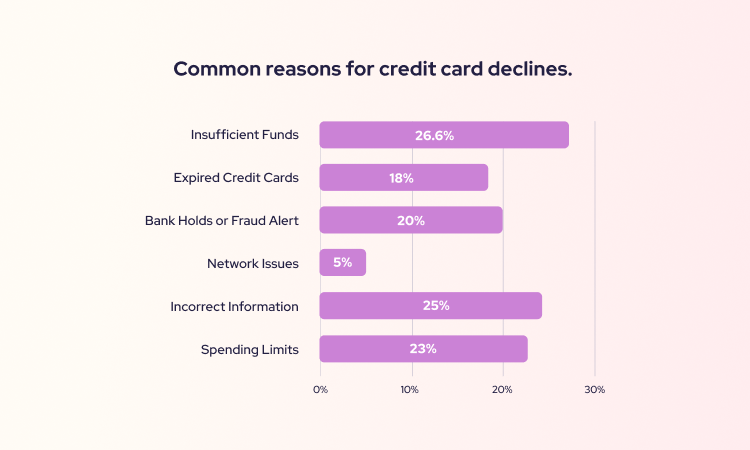

1. Insufficient funds

Sometimes, a customer simply doesn’t have a high enough credit limit to make the purchase. This means the available credit or funds in their account has reached the maximum set by their credit card issuer for that time period. This is one of the most common reasons for a decline message, and it can happen to anyone, especially those with low credit limits or unhealthy spending patterns.

2. Expired card

If the card has expired, it won’t go through, even if everything else is in good standing. Customers may not realize their card needs updating until they try to use it or have missed payments set up for automatic billing.

3. Bank holds or fraud alerts

If a customer card issuer detects unusual activity—like purchases in different locations or a large pending transaction—they might flag or even freeze the card to protect the account from potential fraud. These holds can be sudden, leaving customers caught off guard.

4. Network issues

Sometimes, the problem has nothing to do with the customer or their credit card company. Payment networks and credit card processing companies can experience downtimes or technical hiccups, which can result in temporary declines or missed payments.

5. Incorrect information

If a customer enters incorrect information, such as an invalid credit card number, CVV or expiration date, the credit card transaction won’t go through. This is especially common for an online purchase or mobile payment, where errors are easy to make.

6. Spending limits

Some credit card companies impose daily spending limits to prevent fraud. Even if the customer has funds available, hitting this limit can trigger a decline. Customers may be unaware of these limits until they reach them.

Each of these reasons has a different fix, but they all have one thing in common: they’re often unexpected. When declines happen, understanding the reason can help you guide your customer through the moment calmly and with a solution in mind. The key is knowing what might be causing the issue—and being prepared to handle it with empathy and professionalism.

How to tell a customer about a declined credit card (without losing the sale)

A declined credit card can catch a customer off guard, and it’s a moment that no one wants to deal with. As a business owner, handling it with understanding can make all the difference in keeping the sale and maintaining the customer’s trust.

Start by keeping your tone calm and neutral. A simple, friendly statement like,

“It looks like there was an issue with the card,”

helps convey that this is a common, fixable situation and reassures the customer that they’re not alone. Avoid phrases that could come across as judgmental or overly direct, as these can make the customer feel singled out. Instead, show that you’re on their side by framing it as a small, manageable issue you’re ready to help with.

If they seem flustered, gently offer a suggestion like,

“Sometimes banks flag purchases unexpectedly—do you have another card you’d like to try?”

This provides them an immediate option to resolve the issue without feeling pressured. If they need to step aside to contact their credit card company or check their bank account, reassure them by saying,

“Take your time; I’ll be here when you’re ready.”

This approach creates a sense of partnership, making it clear that their experience matters and you’re patient with the process.

And most importantly, stay positive and professional. Even if it’s an unexpected delay, keeping your attitude upbeat can help defuse any embarrassment the customer might feel and later on they’ll remember that, rather than the decline itself. With this gentle, professional approach, you can not only preserve the sale but also build a moment of trust with your customer that can keep them coming back.

What to check if a customer’s credit card declines

In addition to staying calm and empathic, here are a few quick actionable steps that can help you handle the situation smoothly and professionally, giving the customer a chance to resolve it without stress. Here’s a simple process to follow:

Step 1: Double check card details

Begin by verifying that the credit card information is entered correctly. Politely ask the customer to confirm key details like the card number, expiration date, and CVV code. Sometimes, a small typo is the culprit, and correcting it can resolve the issue right away. If the payment is online, think about integrating error prompts into your online checkout experience to help the customer troubleshoot the issue and continue with the purchase.

Step 2: Suggest they contact their bank

If the details are correct but the card is still declined, encourage the customer to check with their bank. You can say, “Sometimes banks flag purchases, especially larger ones, or those made in new locations.” This lets the customer know that declines aren’t uncommon and can often be fixed with a quick call to their bank.

Step 3: Offer an alternative payment method

If the issue isn’t resolved with the bank or the customer can’t contact them immediately, suggest they try a different card or different payment method. You might say, “If you have another card, we can use that, or I’d be happy to offer other payment methods.” Or if you have access to ACH transfers or sending an invoice for a later date payment that could be a way to move the sale forward with less stress.

Following these steps helps you handle credit card declines with empathy and efficiency, turning a potentially awkward moment into an opportunity for great customer service.

How to lower credit card decline rates in your business

While card declines are sometimes out of your control, there are proactive steps you can take to lower the chances of them happening. Reducing declines means smoother transactions for your customers and fewer lost sales for your business. Here are some effective strategies:

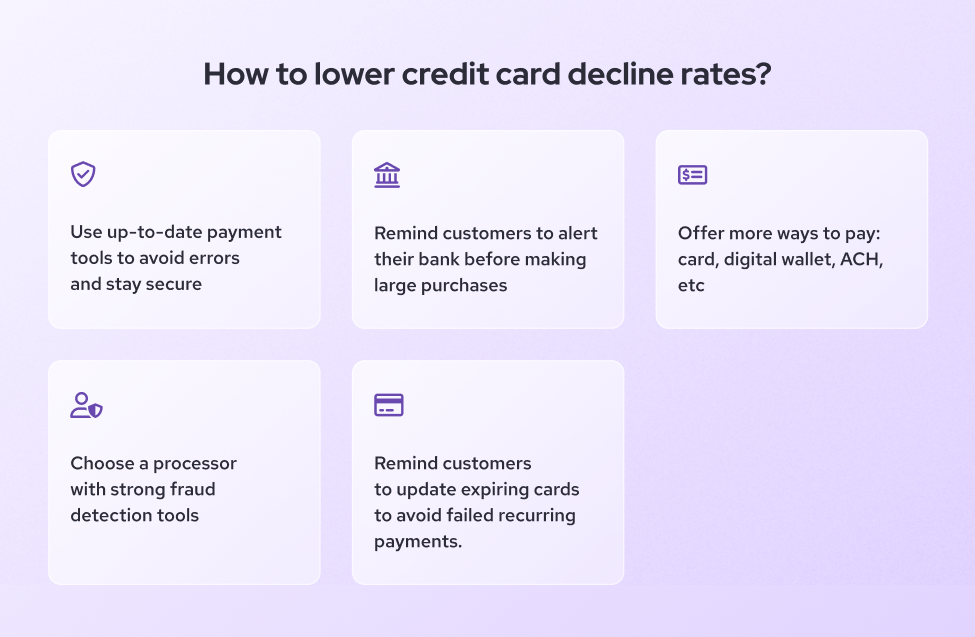

1. Keep your payment systems updated

Outdated payment terminals or online checkout software can increase the chances of transaction failing due to processing errors or security issues. Make sure your payment processing systems, both in-store and online, are up-to-date and compliant with industry standards. This ensures compatibility with the latest bank and credit card security protocols, which helps prevent unnecessary declines.

2. Encourage customers to notify their banks before large purchases

Many declines happen because banks flag larger or out-of-pattern purchases as potential fraud. To help reduce this, encourage customers to notify their bank ahead of making a large purchase with you. This can be especially helpful for businesses in industries where high-ticket sales are common. A friendly reminder can prevent declines and improve your customer’s experience.

3. Offer multiple payment options

Sometimes declines happen simply because of issues with a single payment network. By offering a variety of payment methods—such as credit cards, debit cards, digital wallets, and online ACH payments—you give customers more flexibility and reduce reliance on any one method which can help avoid missed payments. This not only lowers the risk of a failed transaction but also appeals to customers’ diverse payment preferences.

4. Work with a reliable payment processor

The quality of your payment processor plays a major role in transaction success rates. A reliable, secure processor with high authorization rates can help reduce declines, as they have the technology to handle complex transactions and detect suspected fraud without mistakenly blocking legitimate purchases. It’s worth exploring different processors to find one with a reputation for high transaction success rates and strong customer support.

5. Communicate with customers about card updates

If you run a business with automatic recurring payments or subscriptions, remind customers to update their card information when they receive a new card. Expired cards are a common reason for declined payments in subscription-based businesses. Sending a quick reminder before the renewal date or choosing a provider with built-in dunning management can save your customer from any hassle and ensure uninterrupted service.

By implementing these strategies, you can lower credit card decline rates, leading to a smoother checkout experience, happier customers, and stronger sales for your business. Taking these steps shows that you’re committed to providing a seamless payment experience—and that builds trust and loyalty with your customers.

FAQs

Can a declined credit card still go through?

Yes, sometimes declined credit card payments can still go through, depending on the reason for the decline. If the issue is temporary—like a technical glitch with the payment network or an insufficient balance that the customer quickly resolves—the card may work if you attempt the transaction again later. However, if the decline is due to factors like an expired card or a credit limit, the customer will need to address the issue first (e.g., by updating their card or contacting their bank) before trying again.

For best results, suggest that the customer try using a new card or contact their credit card company if the problem persists. This keeps the transaction moving and helps avoid further delays.

What to do if a credit card declines due to a large purchase?

A large purchase can sometimes trigger a decline, as banks may flag high-ticket transactions as potential fraud. If you suspect this is the cause, reassure the customer that this is common and encourage them to contact their bank to confirm the transaction. A simple call to their bank should allow them to authorize the purchase, which typically clears up the issue quickly.

When handling high-value transactions, you can also encourage customers to notify their bank in advance, especially if they’re making an unusually large or out-of-the-ordinary purchase. This can reduce the chances of a decline and help them enjoy a smoother checkout experience.

How do you know if a credit card decline is due to suspicious activity?

Banks and credit card issuers monitor for unusual or suspicious activity, and they’ll sometimes block transactions to protect against fraud. Signs that a decline may be due to suspicious activity include repeated declines across multiple attempts, declines in different locations, or a pattern of high-value purchases in a short period.

If you suspect that suspicious activity might be the cause, encourage the customer to contact their bank for verification. They may need to confirm their identity or authorize the transaction with their bank, which should clear the flag. Staying calm and supportive during this process shows your customer that you’re looking out for their security as well, which can help build trust.

Related Articles

-

Understanding Declines in Credit Card Processing

Nic Beique | September 20, 2021

-

What is an ACH transfer and how much does it cost?

Danny Randell | August 13, 2021

-

How credit card processing works: An ultimate guide

Danny Randell | March 3, 2021