-

Content

Last Updated on January 31, 2025 by May Montenegro

Paying bills? Getting paid? Covering your share of that way-too-fancy charcuterie board? Electronic Funds Transfer (EFT) has you covered. It’s quick, digital, and—best of all—doesn’t involve awkward trips to the bank or pens on life support. In this article, we’re slicing through the jargon to show you what EFT is, how it works, and why it’s a game-changer for your business and your clients.

What is electronic funds transfer (EFT)?

No, we’re not talking about crypto or investments here. Electronic fund transfer or EFT is the modern way to move money between bank accounts—no cash, no checks, no hassle. Whether it’s paying your bills, getting your paycheck, or settling an invoice, electronic fund transfers make it all digital, quick, and efficient. It’s a broad term that includes a variety of electronic payment methods, such as direct deposits, wire transfers, and online bill payments.

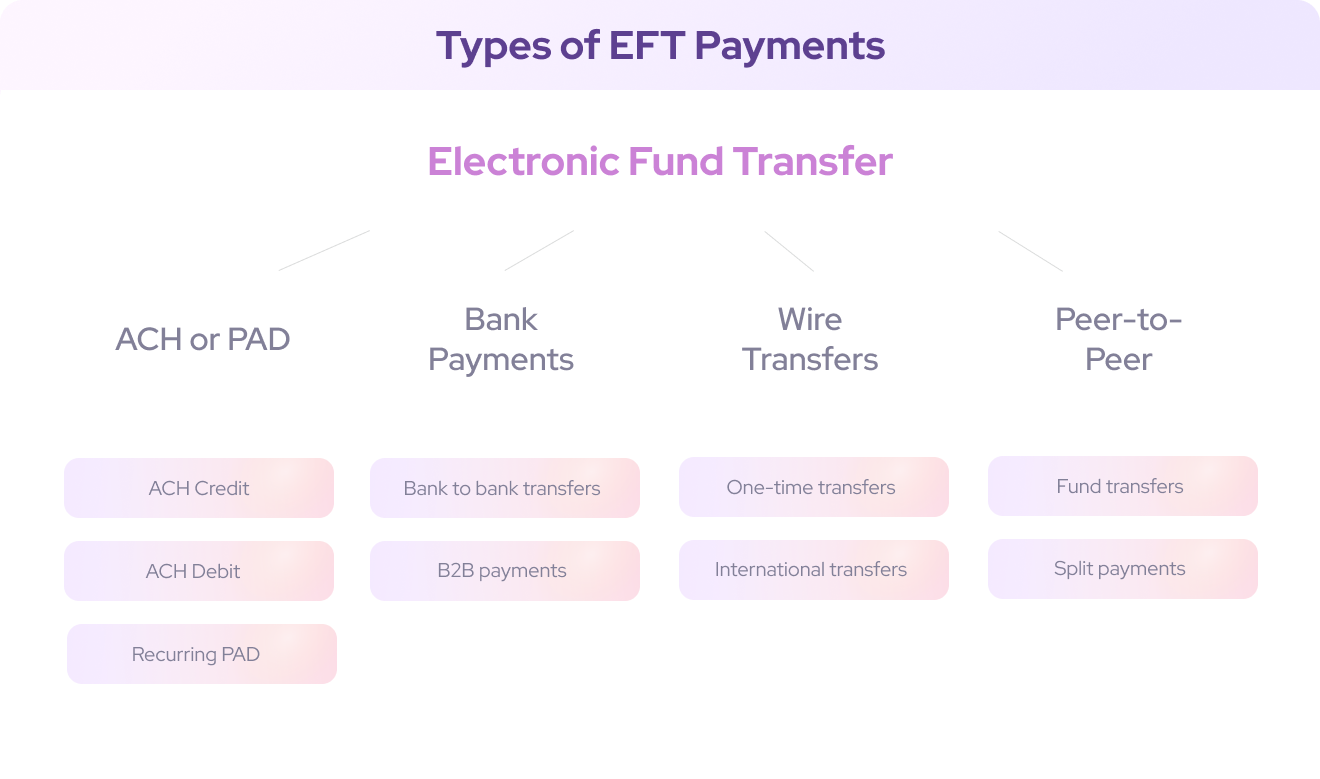

EFT, ACH , PAD, P2P—what’s with all the letters?

EFT often gets tangled up with terms like ACH, PAD, bank payments, wire transfers, and P2P payments. While they’re all part of the EFT family, each one serves a different purpose. Let’s break it down and show how they fit into the bigger picture of EFT payments:

ACH (Automated Clearing House) payments

ACH payments is a batch-based EFT system in the U.S., managed by the National Automated Clearing House Association (NACHA). It’s ideal for recurring payments like payroll, bill payments, and direct deposits. The ACH network connects various financial institutions and facilitates batch processing of transactions. ACH payments can work in two ways:

- ACH credit (push): You send money to another account, like paying a vendor or making a direct deposit.

- ACH debit (pull): Money is withdrawn from your account automatically, like when you pay a utility bill.

Examples of EFT's under ACH:

- Direct deposit (e.g., payroll or government payments)

- Online bill payments made through your bank

- E-commerce payments where funds are debited from your bank account

Want to know more about ACH payments? Download our user-friendly guide on navigating ACH payments for your business complete with templates and NACHA-compliant PAD agreement forms.

PAD (Pre-authorized debit)

Pre-authorized debit is typically a recurring EFT payment where businesses pull funds directly from a customer’s bank account with their consent. It’s perfect for subscriptions, memberships, or utility bills. Customers authorize payments upfront, so it’s predictable and hassle-free.

Examples of EFT's under PAD:

- Gym memberships

- Rent

- Recurring utility payments or phone bills

- Monthly subscription services (e.g., software or streaming)

Bank payments

This is a catch-all term for direct transfers made between bank accounts, often through online banking. Bank payments can use ACH, PAD, or even other methods like real-time rails depending on the setup. To process transactions such as eChecks and ACH payments, users must provide various details including the bank account number, which is crucial for ensuring secure and efficient electronic fund transfers.

Examples of EFT's under bank payments:

- One-off bank-to-bank transfers.

- Transfers initiated through banking apps or portals.

- Business-to-business (B2B) payments directly between accounts.

Wire transfers

Wire transfers are the go-to for fast, high-value transactions, especially internationally. They’re often same-day but come with higher fees compared to ACH or PAD. Wire transfers are secure but best suited for one-time payments.

Examples of EFT's under wire transfers:

- Paying a freelancer or contractor (learn more about best 5 invoicing softwares for freelancers here).

- Sending a large sum to close a real estate deal.

- International payments requiring immediate processing.

P2P (Peer-to-peer) payments

P2P payments or electronic transfers are designed for quick, everyday transactions between individuals. Think splitting a dinner bill or paying your friend back for concert tickets. These payments often run on EFT systems but are optimized for personal use.

Examples of EFT's under P2P:

- Payments via Venmo, PayPal, or Zelle.

- Transferring money to friends or family.

- Splitting bills or casual expenses.

Why EFT payments are great (and not so great)

Now that you understand what an EFT is, let’s talk about why EFT's are a game-changer for businesses and customers alike.

What’s to love about EFT's?

- Convenience: No cash? No problem. EFT's make transferring and receiving money a lot easier. Electronic payments are faster, safer, and more reliable alternatives to traditional payment methods like cash or checks.

- Security: Say goodbye to the risks of lost checks or stolen cash—EFT's are digital, secure, and a reliable way to handle payments. They’re a safer option when accepting funds directly from your customers’ bank accounts compared to credit cards, which can be more prone to fraud and chargebacks. While ACH payments can also face chargebacks, they’re governed by organizations like NACHA, which provide an added layer of oversight and security to screen and manage transactions.

- Cost savings: EFT's typically have lower fees than card transactions.

- Speed: Who wants to wait for a check in the mail? EFT's are faster and have way less hassle.

- Eco-friendly: Less paperwork means fewer trees sacrificed for billing and receipts!

What’s the catch?

- Processing delays: Some EFT's, like ACH payments, take a few days to clear.

- Setup requirements: You’ll need to gather bank details, which can feel like an extra step at first especially for your clients.

- Limited perks: EFT's don’t come with flashy benefits like cashback or travel rewards that credit cards offer for your customers.

- Error risks: Get those account numbers right—mistakes can mean delays or payments sent to the wrong place, especially between different banks. Errors are less likely when transactions occur within the same financial institution.

How long does an electronic funds transfer take?

As a business owner, understanding funding times is crucial—after all, cash flow is the lifeline of your business. If you’re considering EFT's, it’s important to know that processing times can vary depending on the method and your payment provider funding type:

- Instant: Some bank payments or wire transfers (think CashApp, PayPal, or Venmo) can be immediate but often come with higher fees.

- Same-day: Available for certain ACH and wire transfers—though it might also cost extra.

- 1-2 business days: Standard for most ACH payments.

- 3-6 business days: Common for PAD and recurring payments, especially for new setups.

Pro tip: Weekends, holidays, and banking hours can affect processing times, so plan ahead!

Top 5 EFT payment providers

If you’re thinking about using EFT payments for your business (smart move, by the way), here are some top-notch options to consider:

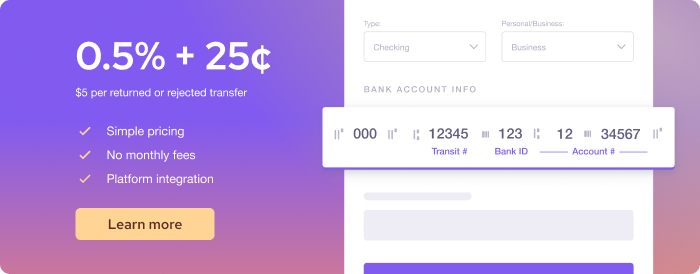

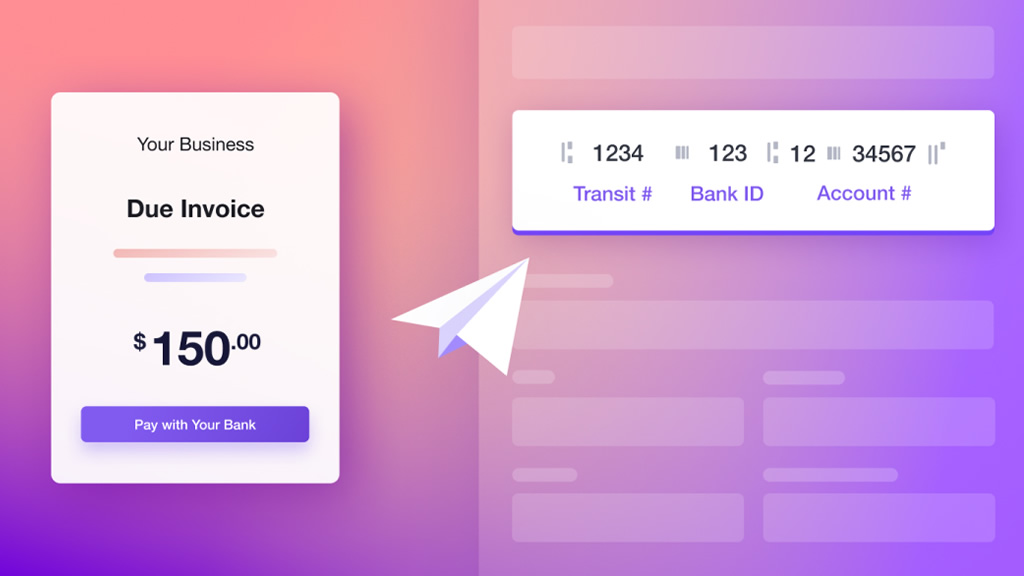

Helcim

Helcim makes accepting EFT payments easy and affordable whether it’s a one-time payment or a recurring charge, through your website or directly on your invoices.

Fees:

- 0.5% + $0.25 per transaction

- Capped at $6 per transaction for payments up to $25,000.

Rotessa

Rotessa focuses on recurring PAD payments however they operate and charge on a tiered pricing.

Fees:

- Plans starting at $17/month for 1-10 transactions

- $94/month for 101 - 250 transactions

- $0.35 per transaction for higher volumes

GoCardless

GoCardless handles recurring and international EFT's

Fees:

- 0.75% + $0.40 per transaction (capped at $3 per transaction)

- Can add customizable invoices for $75/month.

Wave

Wave offers PAD payments alongside its accounting tools.

Fees:

- 1% per transaction (minimum $1)

- No monthly fees

QuickBooks

QuickBooks integrates PAD with accounting and invoicing tools.

Fees:

- 1% (capped at $10)

- Requires QuickBooks Online subscription (starting at $25/month)

Final thoughts

EFT's—whether it’s pre-authorized debits, ACH, or wire transfers—are changing the game for business payments. They’re more affordable, relatively safer, and ditch the hassle of old-school paper processes. With solutions like Helcim’s ACH payments, you can cut costs while delivering a smooth, stress-free experience your customers will appreciate.

Ready to simplify your payments?

Get started with Helcim today—no commitments, just better payments.

FAQs

Can electronic funds transfer (EFT) be reversed?

Yes, EFT's can be reversed, but it depends on the type of payment and the reason for the reversal. For example, ACH payments can be reversed if there’s an error, such as duplicate payments or incorrect amounts, or if the transaction was unauthorized. However, reversals usually have a time limit, so it’s important to act quickly.

Is there a limit to the amount I can send via EFT?

The limit for EFT transactions depends on the payment method and the financial institution. For instance: ACH transfers often have daily or transaction-specific limits, typically ranging from $10,000 to $25,000. Check with your bank or provider for specific limits. Wire transfers usually allow larger amounts, though they may come with higher fees.

What information do I need to initiate an EFT?

To initiate an EFT, you’ll typically need:

- The recipient’s full name

- Bank name and branch

- Account number

- Transit/routing number (or equivalent, like IBAN or SWIFT for international transfers)

- Financial institutions play a crucial role in processing and regulating EFT transactions, ensuring compliance with the Electronic Funds Transfer Act (EFTA).

- Accurate details are crucial to avoid delays or misdirected payments.

How are international EFT's different from domestic ones?

International EFT's often use different networks, such as SWIFT or IBAN, to facilitate transactions across borders. These payments may:

- Take longer to process

- Incur higher fees due to currency conversion and international bank charges.

- Require additional details, like the recipient’s address and a SWIFT/BIC code.

Can I set up recurring EFT payments?

Yes, recurring EFT payments are a common use case for pre-authorized debits (PAD) or ACH payments. These are ideal for subscriptions, membership fees, or ongoing service contracts. Customers or businesses set up a schedule for the payments, which are then processed automatically.

Are EFT payments taxable?

The payment itself isn’t taxable, but the transaction may relate to taxable income or expenses. For example: If you’re receiving funds as payment for goods or services, you must report it as income. Similarly, businesses can track EFT's for deductible expenses. Always consult with a tax professional to ensure compliance with local tax laws.

Related Articles

-

How to create a NACHA-compliant ACH authorization form

May Montenegro | August 20, 2024

-

Welcome to Helcim ACH Payments

Danny Randell | March 15, 2022