Passing on credit card fees to customers has become a hot topic for many small businesses looking to offset their processing costs.

In fact, nearly one in five (19%) of small businesses are considering this strategy.

While it may be a great opportunity for your business to improve cash flow, it's important to take a close look at customer impact and best practices before implementing any changes.

In this blog, we'll dive into the psychology behind pricing and explore the impact of passing on fees to your customers. We'll also discuss the pros and cons of this strategy and provide some best practices to help you decide what's right for your business.

Public sentiment around passing on fees

It's no secret that public sentiment surrounding surchargingand other similar practices is mixed. Some customers view making a purchase from a business as a privilege for which the payment processing costs should be covered by the business itself.

Frustration over passing on credit card fees to consumers may be compounded by the growing prevalence of tipping culture in North America, which is causing frustration among consumers in the face of inflation and continued economic turmoil.

While many customers are accustomed to tipping in certain industries and services, such as restaurants or esthetic services, there is increasing controversy surrounding tip options at checkout for everyday services and businesses. Adding another expense to a customer's bill can be controversial, and many customers would prefer to have the tip worked into the pricing so they know exactly what they're paying upfront. When taxes and GST are also factored in, the total can quickly add up and irritate customers.

Despite these concerns, some customers don't mind paying extra fees or using an alternative payment method. This suggests that there may be a market of willing customers who are open to offsetting your processing costs.

While passing on processing costs to your customers may be a subtle way to offset overhead costs, it's important to consider best practices on a case-by-case basis. Some companies have experienced backlash from consumers for implementing surcharges, while others have decided not to implement them out of concern for consumer interest and affordability.

Benefits of passing on credit card fees to customers

Passing on processing fees can decrease your costs to accept payments while incentivizing customers to use other payment methods that are less costly to your business such as ACH, but there are also benefits to specific industries which we have listed below:

B2B and Wholesalers: Industries like wholesalers who collect payment primarily through cheques will be able to speed up their accounts receivables and offset the costs of bounced cheques by encouraging other faster payment methods with less NSF .

Legal and Financial services: Professionals such as accountants and lawyers who often receive cheques can offer a faster payment method through alternative payment methods like ACH bank transfers and recurring invoicing while offsetting their payment processing fees and administrative costs.

Medical and Wellness: Estheticians, plastic surgeons, dermatologists and medical practices that are not covered by insurance can now offer more ways for their clients to pay without having to pay exorbitant fees instead of cash and cheques.

High cost necessity products or services: Customers may be willing to pay a fee for the ability to pay via credit card for higher ticket items they have to pay for on routine such as child care in exchange for the rewards or cash back options offered by the credit card brand. However, offering another convenient payment method such as automated ACH bank to bank transfers as an alternative without a levied fee can incentivize them to use a payment method with a lower processing fee for you which has little impact on them aside from the one-time setup to get their bank details.

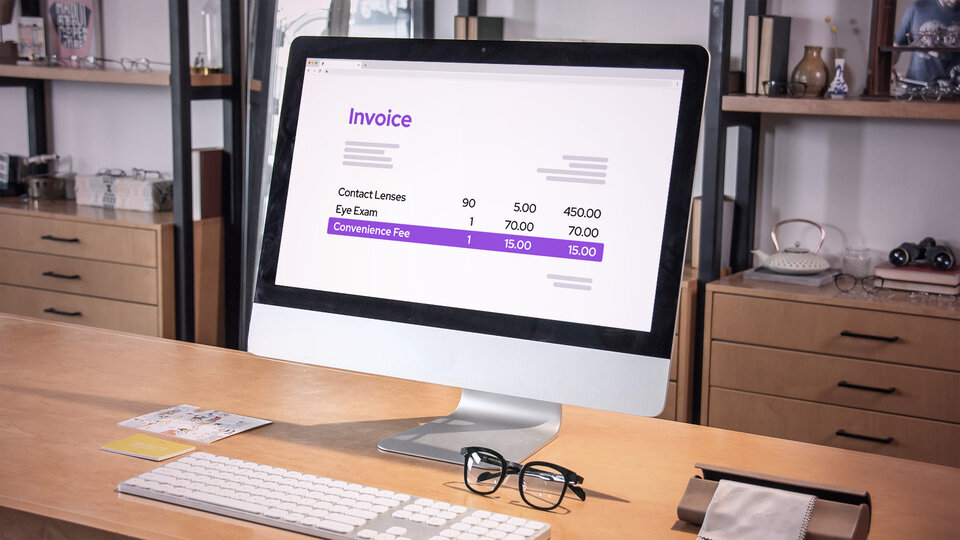

The impact of passing on credit card fees to your overall checkout experience

As we discussed earlier, for some cardholders an unexpected extra fee on top of the total can throw them off, but depending on the industry and frequency of the cost others may not mind.

Accepting credit cards brings many benefits. Your business permits your customers more flexibility in their payment options while opening yourself up to more transactions.

Passing on the fees associated with accepting credit card payments (or some of it) onto your customers can help cut your processing costs and other administrative losses,however; it is important to consider how to and whether you can preserve your customer loyalty and checkout experience while doing so.

Here are a few other things you may want to consider that may help you decide whether it is right for you:

- What does your checkout experience look like?

- What sort of transactions do most of your payments fall under? Can you easily implement a fee for these types of transactions?

- What are other businesses in your industry doing?

- Have you taken an honest assessment of your costs vs. the benefit of passing on these fees?

Transparency is key: How to keep your customers on board

As a savvy business owner, you know that pricing strategies can make or break your bottom line. That's why it's crucial to consider every factor, including how you handle payment processing costs. But did you know that how you communicate these costs to your customers can make all the difference in their perception of your business?

By being transparent and upfront about the reasoning behind passing on these costs, you can build trust and loyalty with your customers. And offering alternative payment methods like ACH bank-to-bank transfers on online payments or ways to save on fees shows that you value their business and want to make their experience as smooth as possible.

With effective communication and transparency, you can confidently navigate the sensitivities of pricing and boost your bottom line.

Striking a balance

Striking a balance between passing processing fees onto customers or absorbing them as a cost of doing business can be a complex decision for merchants. Both options have pros and cons, and ultimately, the right decision depends on individual circumstances.

With the idea of credit card surcharges and convenience fees becoming a buzzword in the business world, many Canadian merchants are grappling with this decision. It's important to consider what other businesses are doing, best practices, and whether passing on these costs aligns with your company values.

But by being transparent and upfront about the reasoning behind any decision, you can build trust and loyalty with your customers and ultimately boost your bottom line.

How to offset credit card processing fees: 3 Alternatives

Here are a few other ways merchants can make up the difference if you decide it might not be best for your customer experience and a fit for your business.

Adjust your pricing

If a merchant chooses not to pass on their processing costs, they could still reflect this cost in their product or service prices which many are already doing to cover the cost of business.

To do this, businesses need to assess their current costs honestly- the in’s and out’s- and determine the best way to recoup or cut costs amidst a recession.

Lower your processing costs with your payment processor

While your payment processor may offer tools that enable you to seamlessly pass on your fees, there are also other ways to save even more just by taking a second look at your processing costs. Thus, you can continue to cut processing costs without any added costs.

Here are some guiding questions:

What sort of pricing model are you processing with?

Have you considered switching to interchange plus pricing as a means to cut down on processing costs and take advantage of the savings from lower interchange rates?

Have you read your merchant statement lately?

Merchant statements can be one of the ways payment processors intentionally hide fees or overwhelm you in an attempt to make you apathetic about your charges. You could be getting swindled on extra fees- here’s our guide to finding hidden fees and understanding where and what to look out for on your bill.

Are you taking advantage of lower rates?

Familiarize yourself with changes to interchange rates, or better yet, find a processor who informs you about those changes and how to take advantage of them. For example, using a recurring billing tool to get lower tokenized interchange rates on your transactions is a great way to cut down those processing costs.

Offer a discount instead

In Canada and the U.S., many merchants have worked out a loophole to fees and have been doing so for some time. Many merchants will offer a discount to reduce the would-be fee from the total as an incentive to pay with another method, such as cash or debit.

Instead of imposing an extra charge which may not be the right route for everyone to be received poorly, merchants have already been accommodating for their costs of business through a friendlier discount equivalent to the cost of the fees, for using another method, such as cash.

Final Thoughts

In conclusion, passing on payment processing fees to customers can be a tricky decision for businesses. While it can help offset costs, it may also cause customer dissatisfaction and even push them away.

Thus, before implementing this strategy, businesses must consider various factors such as the industry they belong to, the impact on checkout experience, and the preferences of their customers.

Moreover, transparent communication with customers about the reasoning behind passing on these costs can help build trust and loyalty.

Ultimately, businesses must strike a balance between passing on the fees and absorbing them as a cost of doing business to maintain customer satisfaction and loyalty while also achieving their financial goals.