Ever felt like your money’s in limbo? Like it’s there, but you can’t quite touch it yet? Welcome to the world of credit card pre-authorizations, or as the cool kids (okay, mostly us payments people) call it: "pre-auths". Often overlooked, yet, an incredibly handy tool in your merchant toolbox. It’s like reserving a table at a busy restaurant—except, instead of a table, it’s your customer’s funds. And trust me, this might be the only hold on money you’re glad exists. Here's why. In this article, we’ll break down when, why, and how to use pre-auths like a pro, making credit card processing smoother for your business.

So, what's a credit card pre-authorization?

A pre-authorization is like saying, “Hey, I’m not charging your customer’s credit card just yet, but I want to make sure you can actually pay when the time comes.” It puts a hold on your customer’s funds, freezing them for later without immediately pulling them out of their account, and reduces their customer's credit limit. This is super useful when you’re not sure of the final amount you’ll charge (think hotels, restaurants, or car rentals), or you want to ensure you get paid before delivering a product or service. This ensures there are sufficient funds available for the transaction when it is finalized.

Here’s how it works:

- You place an authorization hold on a set amount of money from the customer’s credit card.

- Your credit card processor verifies that the funds are available and holds them until you decide to charge.

- The customer’s available balance drops by the hold amount, but no actual charge hits their statement until you capture it.

Think of it like a security deposit for your business—you’re not pulling the money out just yet, but you know it’s there, ready to be collected when needed.

The nuts and bolts: capture and purchase

Once you're ready to get paid, it's time for the capture—the step where you actually take the money. The cool thing is, the amount you capture can be different from the original pre-auth (as long as it's lower, you're all set). If it's higher, the customer might have to reauthorize it, which could slow things down.

- Capture: This is where you say, "Alright, the job's done, now let’s charge $X." The system uses the approval code from the pre-auth to complete the transaction. The final amount can be less than the pre-auth, and any leftover funds go back to the customer.

- Purchase (auth+capture): If you're running a straightforward business where the amount is always known upfront—like a retail store or café—you might just stick with a purchase. It combines the pre-auth and capture into one single move. Easy peasy.

Real-life example: Hotels and gas stations

Here’s a scenario you might’ve seen firsthand: You check into a hotel, and they put a hold on your card for $200, just to cover incidental charges (snacks, room service, or that random mini-bar bottle of water you might accidentally drink). They’re not charging you yet, but they’re making sure they can. When you check out, they adjust that hold based on your actual spending and release any leftover amount. The transaction date plays a crucial role in determining how long the hold will last, affecting when the funds are made available again to the customer. Gas stations do something similar: they’ll pre-auth your card for, say, $100 to make sure you have enough to fill up, but you’ll only get charged for what you actually pump.

What’s in it for merchants?

So, why bother with all this pre-auth stuff when you could just swipe and charge? Well, here’s why it might be your new best friend:

- Better cash flow control: Pre-auths help ensure you get paid while giving you the flexibility to adjust final charges. It’s a safe middle ground, especially when the exact price isn’t locked in at the time of service.

- Fee avoidance: Refunds come with fees, and no one likes paying extra when they don’t have to. Pre-auths let you cancel holds without dinging your bottom line. Plus, processors like Helcim automates pre-auth reversals after 7 days, so you’re not stuck dealing with old transactions that never went through. Additionally, pre-auths can help reduce refund fees by preventing unnecessary transactions when items are out of stock or cancellations occur.

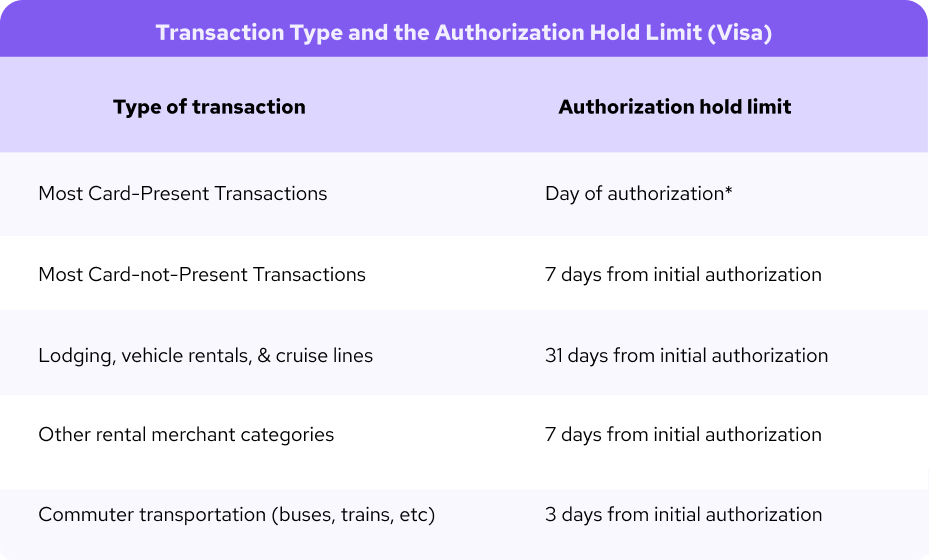

- Happier customers: You’re not hitting their card with extra charges they weren’t expecting. They’ll only see the final transaction, which reduces confusion and keeps things clean on their end. The duration of pre-auths can also vary based on the merchant classification code (MCC) and the type of transaction as seen below, which is important for managing longer pre-authorization periods.

What about debit card pre-authorization?

It’s not all about credit cards—debit cards can also be pre-authorized too. When assessing a customer’s financial background, it’s important to consider all sources of personal income, including salary, investments, and separate maintenance income. The same rules apply: the money is held, not spent, but in this case, it’s your customer’s actual bank account balance being affected. This is great for businesses that cater to a lot of debit card users because you still get the safety of holding funds without immediately draining their account.

Simplifying pre–authorization for your business

Pre-auths might seem tricky, but with Helcim, it’s easy. To streamline the process, businesses can collect essential customer information such as employment status and mailing address to tailor credit card offers and ensure accurate processing. Our system lets you seamlessly manage pre-authorizations online through the Virtual Terminal or in-person with our Point of Sale app so you never have to worry about missed payments or refund headaches. Need to reverse a pre-auth? We’ve got that covered too, with automated reversals after 7 days if they’re not captured. This way, you and your customers can rest assured that their pre-authorized transactions are being taken care of and you can be confident you're adhering to the card brand rules.

Ready to take control of your payments?

If pre-authorizations sound like a game-changer for your business, Helcim can help. We offer transparent pricing, no contracts, and the tools to help you manage everything from pre-auths to purchases—all with the ease you deserve. Get started today for free here.

Frequently asked questions:

What happens if the amount exceeds the balance of the customer’s card on hold?

If the final amount exceeds the available funds on the customer’s card that were pre-authorized, the transaction may be declined. You will need to get a new authorization for the updated amount.

What happens if I forget to capture the card after a pre-authorization?

If you don’t capture the funds within the pre-authorization window (typically 7 days), the hold will expire, and the funds will be released back to the customer’s card. You would need to re-authorize the payment if you still wish to capture the funds.

What happens if the actual amount is higher than the pre-authorized amount?

If the actual amount is higher than what was initially pre-authorized, you’ll need to request a new authorization for the higher amount. The customer’s card may decline the new amount if their available balance isn't sufficient.

How long does a pre-authorization hold?

Pre-authorizations typically last up to 7 days before the hold is automatically released. Some card brands may allow a longer window, but it’s best to capture funds as soon as possible.