As a merchant, it can be important to understand the interchange rates associated with processing credit and debit card payments, especially if you are looking for ways to save on your processing fees with Interchange Plus pricing.

Interchange fees are set by the card networks (Visa, Mastercard, etc.) and are the fees that payment processors pay for each transaction. They may be passed onto you as a flat rate, as part of a tiered pricing model, or as the wholesale rate with a nominal charge on top, as in the case of Interchange Plus.

Recently, several changes have been made to these interchange rates that may affect your payment processing fees if you are a Helcim merchant. Understanding Interchange rates and changes can help you identify savings and how to curb higher interchange rates on your statement.

Here are the key takeaways, which we will cover in more depth later in this article:

Visa Interchange changes

Updates to International/Interregional Base fee Programs

- Elimination of older international fees.

- Introduction of new charge codes, names, and rates.

- Program rates changed by an average of 0.01%.

Consumer Infinite Product Price Adjustments

- Updates to consumer credit interchange fee programs.

- Fee increases by an average of 0.13% for specific consumer infinite card products.

**Expansion of Small Merchant Interchange Programs **

- Introducing additional interchange categories for Visa Infinite products.

- Rates range from 0% - 2.70%, with per-item fees from $0 - $0.10.

- Applicable to specific Merchant Category Codes.

- Rates apply to card-not-present and card-present transactions meeting custom payment service (CPS) qualifications.

**Digital Commerce Service Fee **

- Introducing a fee of 0.0075% for all card-not-present settled transactions.

- As a result of the new digital fee, Visa is discontinuing charges for Address Verification Service (AVS) and Card Verification Value 2 (CVV2) Verification.

Mastercard Interchange updates

New Pre Authorization Fee.

- Rates vary for card-present and card-not-present transactions.

Mastercard Authorization Optimizer Service Fee:

- Fee related to recurring card-not-present transactions with insufficient funds.

- Amount: $0.02. Primarily affecting merchants with a high volume of declined transactions on recurring card-not-present transactions.

New Visa Interchange rates for US merchants

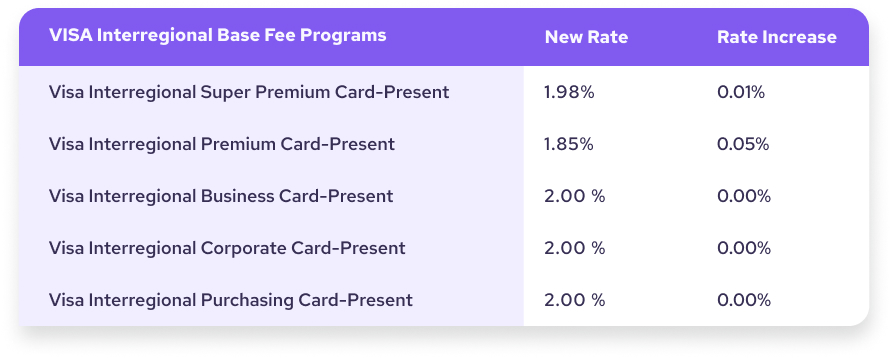

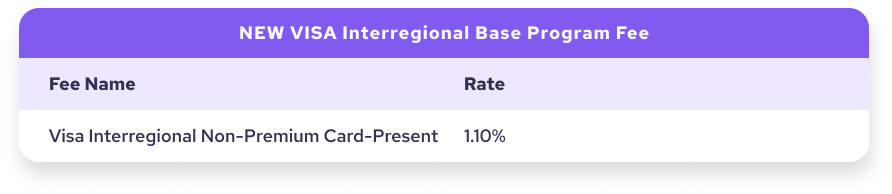

International / Interregional base fee programs

On October 13, 2023, Visa will update its interregional interchange program. There are two changes happening with this update: Visa is bidding adieu to some older international fees and rolling out a fresh batch of charge codes, names, and rates for this program. Program rates will be changing by an average of 0.01%.

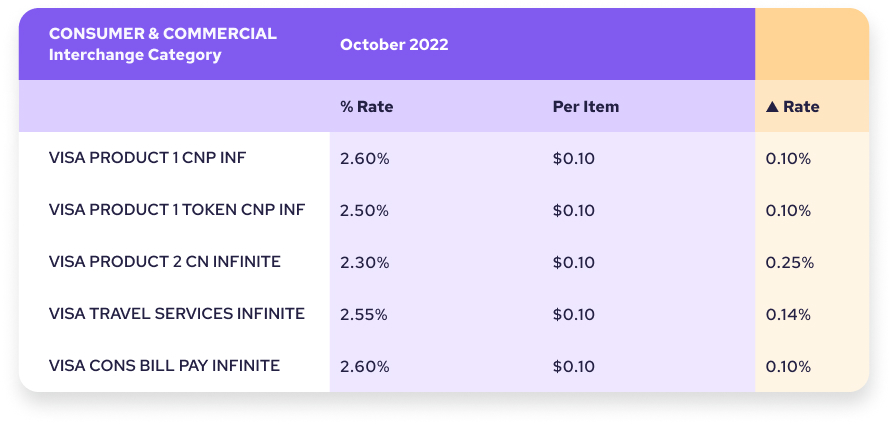

Consumer Infinite Product price changes

In addition, Visa will be updating its consumer credit interchange fee programs this month. These changes will apply to most premium consumer cards.

What’s changing?

Visa is increasing fees by an average of 0.13% for transactions made with certain consumer Infinite card products. See specific fees and changes below:

_P.S. Looking for a way to offset rising interchange fees on card-not-present transactions? _

Try the merchant fee saver when you send a Helcim invoice or integrate HelcimPay.js on your website. Customers can choose to pay the processing fees for a given transaction or pay another way with ACH bank transfers, which have a lower processing cost. Win-win.

Find out more about zero-fee credit card processing →

New small merchant Interchange programs for consumer credit transactions

Starting October 13, 2023, Visa is introducing additional interchange categories for the Visa Infinite product, bringing potential benefits to specific small merchant segments. The new percentage rate for these fees ranges from 0% - 2.70%, and the per-item fee ranges from $0 - $0.10.

Details on Transaction Qualifications

These segments include restaurants, taxi services, real estate, education, healthcare, advertising, insurance, services, telecommunications, and cable providers. These rates will apply to consumer credit transactions for card-not-present transactions and transactions that meet card-present (CP) custom payment service (CPS) qualification.

The specific details of CPS qualification criteria typically include factors related to the nature of the transaction, the security measures in place, and the technology used in the payment process. Some common elements that could be part of CPS qualification criteria might include:

-

Physical Card Presence: Transaction rates will vary depending on whether the payment card is physically used to tap, swipe, or insert at a point-of-sale (POS) terminal. Card-present transactions typically have lower rates of fraud, which means they will have lower interchange rates.

-

Secure Authentication: When secure methods of cardholder authentication, such as PIN entry or chip authentication, are used to ensure the card's validity, card brands usually offer lower rates.

-

EMV Compliance: EMV chip card technology enhances security in card-present transactions. Therefore, many card brands like Visa and Mastercard will not only charge higher rates for swiping, which is much less secure, but lower rates for EMV transactions or using chip-enabled terminals.

-

Transaction Integrity: Ensuring that the transaction data remains secure and is not susceptible to fraud or tampering. This could look like processing with a payment provider that ensures PCI compliance, for example. Another requirement for CPS on card-not-present transactions is AVS, which, if not enabled, can be a cause for many downgraded (higher) rates.

-

Merchant Category: Some CPS criteria might be tailored to specific types of merchants or industries, such as restaurants, taxi services, or retail businesses. High-risk industries tend to have higher interchange rates due to the nature of risk.

Overall, the CPS qualification criteria are designed to distinguish card-present transactions from card-not-present (CNP) transactions and help determine the appropriate interchange rates and fee structures for each type of transaction. Visa sets these criteria to maintain security, accuracy, and consistency in payment processing.

Digital commerce service fee being introduced in the US

In a sort of give-and-take fashion, Visa is making some strategic moves by introducing a new fee for card-not-present transactions while simultaneously easing the burden on businesses when it comes to anti-fraud services. Although the new fee is relatively small, it will be applied to all card-not-present transactions. These changes serve a dual purpose: mitigating the risk and losses associated with card-not-present transactions while promoting best practices in fraud prevention. These changes are not unlike what we’ve seen Mastercard implement already and mirror the industry movement towards mitigating risk by leveraging anti-fraud technology.

What’s changing?

Effective October 1, 2023, introduce a Digital Commerce Services fee of 0.0075% on all card-not-present (CNP) settled transactions, with a minimum of $0.0075 per transaction.

This new fee will be partially offset by Visa US no longer charging for the following services in the US on CNP transactions:

- Address Verification Service (AVS) ($0.001 per transaction)

- Card Verification Value 2 (CVV2) Verification ($0.0025 per transaction)

This fee is relatively small and is unlikely to significantly affect small merchants.

New Mastercard Interchange rates for Canadian merchants

Pre-authorization fee

Early this October, Mastercard also plans on charging a fee for pre-authorizations, specifically for approved credit card transactions. The impact of this fee will generally be minimal or even negligible for most merchants. It will primarily affect merchants who conduct high-value pre-authorizations.

Here are the rates:

- Card present = 0.0075% (min $0.01)

- Card not present = 0.0125% (min $0.01)

Note: These rates do not apply to debit transactions or the MCC 5542 (fuel).

Mastercard authorization optimizer service fee

Starting on October 9, 2023, Mastercard is introducing a novel fee related to recurring card-not-present transactions. Specifically, those declined due to insufficient funds. This new fee, known as the 'Authorization Optimizer Service Fee' (powered by AI), amounts to $0.02.

The idea behind the fee is that Mastercard will use its network visibility and artificial intelligence to provide you, the merchant, with advice codes that will inform you when it's a good idea to try the payment again to make sure it goes through.

This will have a very small impact on most merchants. Only merchants who complete a high-level of decline transactions on recurring card not present transactions may be impacted.

FAQs

What's Interchange?

Interchange is the fee collected by the credit card issuing bank on every transaction. This is the cost to the card brand networks and financial institutions in terms of cost and perceived and actual risk of fraud/ loss. These rates are set by card brands bi-annually and apply to all processors. Processors then decide which pricing model to charge to businesses for the convenience of accepting payments in order to cover their costs and margins.

Who pays the Interchange?

The credit card processors (like Helcim) are responsible for paying the bank the interchange after the transaction has been processed. Hence, the interchange fee will make up a component of your credit card processing fees. At Helcim, we pass on the wholesale interchange fee to you with a nominal set margin on top so you know exactly what you are paying for each transaction.

Are you curious about how much you could be paying with Interchange Plus pricing? Try our new rate calculator to calculate your processing fees or compare with your current provider.

How do US merchants benefit from rate changes?

This fall, many merchants may find the impact of interchange rate changes to be relatively minimal. By utilizing chip-enabled terminals and card-not-present best practices, you can effectively shield yourself from potentially higher fees while still capitalizing on other lowered interchange rates. It's important to note that these rates undergo adjustments every October and April, which means that if rates do happen to decrease, you, as a merchant, have a valuable opportunity to tap into these reduced rates by processing with Helcim.