-

Content

What are MOTO transactions?

Before online shopping carts, tap-to-pay, and QR codes, there was… the catalog.

That’s where MOTO payments or Mail order / Telephone order got their start—back in the early-to-mid 20th century, when shoppers would flip through a catalog like Sears, fill out an order form, and mail it in with a check or money order. The mail order form was the method used to submit payment information. Businesses then would process the order by hand and ship out the goods.

This system laid the groundwork for card-not-present transactions as we know them today. And while the tech has evolved, the core idea is still the same: letting your customers pay without being there in person. In MOTO payments, customers provide their credit card details by phone or mail, and the merchant manually enters these credit card details to process the payment.

Although MOTO payments are less common now, they’re still incredibly useful for businesses that take payments by phone or serve customers who aren’t always online.

Are MOTO payments still relevant today?

While MOTO transactions might feel like a relic of the past—especially in today’s world of e-commerce and mobile wallets—many businesses still rely on them every day. And yours might benefit too.

Think of service providers taking deposits over the phone, charities accepting remote donations, or even customers who just prefer not to pay online. MOTO offers a low-friction, familiar way for these types of businesses to get paid. MOTO payments also provide a personal touch through direct, human interaction, which can help build customer trust for businesses serving clients who prefer not to pay online.

While you might think that having your POS machine is enough, having multiple ways to accept payments might actually help your business get even more customers.

According to Visa, 59% of small businesses in the U.S. already accept digital payments—or plan to go entirely digital by 2024. While “digital payments” is a broad category, this shows that flexibility is top of mind—and for some businesses, that means being able to process payments over the phone (i.e., MOTO) when other methods don’t fit.

So, could you be overlooking a quiet but reliable tool—MOTO payments—that many businesses still use every day? Let’s break it down: what it is, how it works today, and how to make it yours with Helcim.

What MOTO means in credit card processing

A MOTO payment is, again, a type of card-not-present transaction, meaning the customer isn’t in front of you and there’s no physical card to tap, swipe, or insert. In these cases, the merchant collects customer payment information remotely, such as over the phone, mail, or fax.

Think:

- A dog groomer taking a deposit by phone, entering the customer's card details for a moto transaction.

- A dentist processing a payment after a follow-up call, using the customer's card information for a MOTO transaction.

- A travel agent finalizing a booking, securely handling the customer's card for a MOTO transaction.

This is still common in:

- Service-based businesses

- Appointment-based industries

- Cases where customers don’t use online checkouts

You don’t necessarily need any special hardware to accept MOTO payments—just a payment processor that supports them and a virtual terminal you can access through your browser.

How do MOTO transactions work?

So, how do MOTO payments actually happen behind the scenes? Don’t worry—it’s simpler than it sounds, and no one’s mailing in checks or flipping through catalogs anymore.

Here’s a quick rundown:

- Your customer calls in and gives you their credit card info.

- You key in the payment details into a payment tool (more on that below), making sure to securely handle customer data and sensitive payment information throughout the process.

- The payment is processed, and if all goes well, the funds land in your account like any other card transaction.

No card readers necessary, no storefront, no customer action after the call—just a straightforward way to get paid.

How do you accept MOTO transactions?

Let’s say you’re ready to start accepting MOTO payments. Great—now how do you actually do it? To process MOTO transactions, your business will first need to set up a merchant account.

A merchant account allows you to accept credit and debit card payments remotely and is essential for secure transaction processing through virtual terminals and payment processors. From here, you’ve got two main options, depending on the setup you prefer:

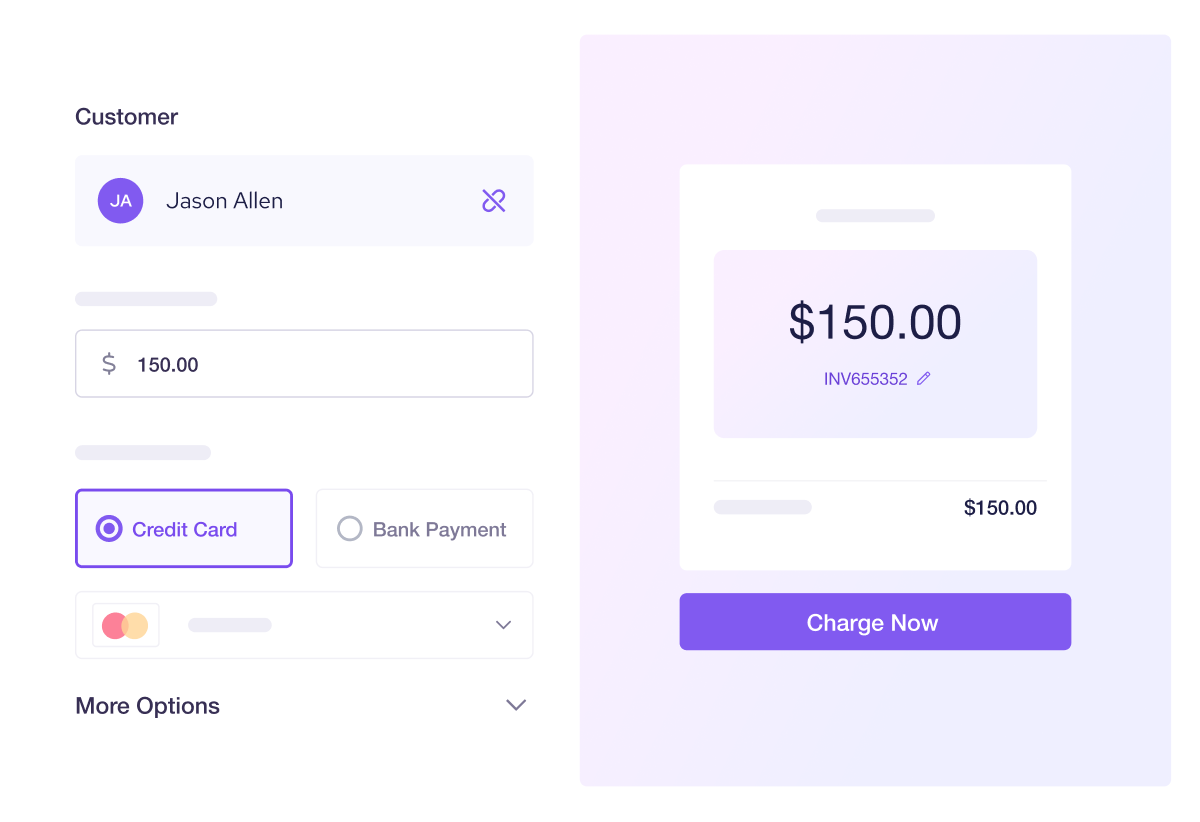

1. Virtual Terminal

A virtual terminal is a secure, browser-based interface where you manually enter card details to charge a customer. It’s usually included in your payment processor’s dashboard. Unlike a traditional payment terminal, a virtual terminal allows manual entry from any device.

Best for:

- Teams working remotely

- Admins collecting payments over the phone

- Businesses without a physical checkout setup

Many virtual terminals also include an address verification service (AVS) to help prevent card-not-present fraud by validating the shopper's address information against the card issuer's records. You’ll just need a device with internet access—no hardware required.

2. Point-of-Sale Terminals (via manual entry)

Many smart POS terminals also support manual card entry. Under payment methods available, you can select “manual entry” mode and enter the card number, expiration date, security code, billing address (including billing zip/postal code), and other required details right on the screen. A verification service such as address verification service (AVS) is often used to confirm the billing address and reduce card-present fraud.

Best for:

- On-the-go businesses that prefer using a terminal

- Teams that already use POS hardware and want to centralize payments

Heads up: some processors restrict MOTO by default because of fraud risks, so make sure it’s enabled for your account.

When are MOTO transactions useful?

They’re not for every business, but in the right scenarios, MOTO is a lifesaver.

You’ll find them useful when:

- A customer calls in to place an order or make a payment

- You’re processing phone orders where customers provide payment details over the phone

- You’re chasing unpaid invoices and want to collect over the phone

- Your customers prefer not to pay online

- You don’t have a storefront or physical checkout

This comes up often in industries like healthcare, professional services, trades, non-profits, and remote-first businesses. If you’re regularly on the phone with customers, it makes sense to have a payment method that keeps up.

What are the fees and pricing for MOTO transactions?

MOTO (Mail Order/Telephone Order) transactions typically incur higher processing fees than in-person sales because they are considered higher-risk for fraud and chargebacks. Helcim offers a competitive alternative for these payments.

For instance, the average rate for a $300 keyed-in or online transaction with a Visa is 2.27% + $0.25. For comparison, Stripe's standard plan charges a flat fee of 3.4% + $0.30 for the same transaction. Unlike a flat fee, Helcim's rate also automatically decreases as your processing volume grows, increasing your savings over time.

What to watch out for when using MOTO payments

As helpful as MOTO payments are, there are a few things to keep in mind.

1. Fraud risk is higher in MOTO (Mail Order / Telephone Order) payments

Because the card isn’t physically present, it is easier for bad actors to use stolen card information without detection. As a result, chargebacks can be more common. Using tools like AVS (Address Verification System) and CVV checks can help mitigate this. These are part of broader security protocols designed to address security concerns and protect against fraudulent actors and activity. While fraudulent orders are a common risk in MOTO payments, risk management solutions can help detect and prevent them.

2. Processing fees might be slightly higher.

Card-not-present transactions tend to come with a higher rate than in-person ones and this is again due to the fraud risks involved, so make sure you know your pricing structure.

3. PCI compliance still applies.

You’re still responsible for keeping cardholder data secure. That means: no sticky notes, no spreadsheets, and definitely no storing card details unless your system is certified to do so. It's important that the business has a secure payment process in place and that they adhere to PCI DSS and PCI DSS regulations to protect customer information and prevent data breaches.

How do you get MOTO payments for an affordable rate?

If you’re looking for a flexible and cost-effective way to process MOTO transactions, Helcim makes it easy.

With Helcim, you can:

- Use a Virtual Terminal right from your dashboard—no special software or hardware required

- Manually enter payments through your Helcim Smart Terminal, if you prefer a physical device

- Get access to transparent, interchange-plus pricing—so you’re not overpaying just because it’s a card-not-present transaction

- Stay PCI-compliant with built-in tools and support

Whether you’re accepting the occasional phone payment or using MOTO daily, Helcim gives you the tools to do it right—without surprise fees or clunky systems.

Start accepting MOTO transactions today

Whether you take payments occasionally over the phone or need a reliable way to bill remote customers, Helcim’s Virtual Terminal gives you the tools to do it securely—without extra costs or complicated setups.

- Accept credit card payments over the phone or by mail

- Use the Virtual Terminal from anywhere—no hardware needed

- Stay PCI compliant with built-in safeguards

- Get transparent, low-cost pricing with no monthly fees

Ready to try it out?

Create a free Helcim account here and start accepting MOTO payments in just a few clicks.

FAQs

Are MOTO payments secure?

Yes, as long as you're using a PCI-compliant processor and avoid storing card details manually. Security features like AVS and CVV verification add an extra layer of protection.

Can I use MOTO if I don’t have a physical terminal?

Absolutely. You can accept MOTO payments using just a virtual terminal through your browser—no hardware needed.

Is there a limit to how many MOTO payments I can accept?

Not usually, but some providers may flag unusual spikes in volume. If you expect a large number of manual payments, check with your processor.

How much does it cost to process MOTO payments?

It varies by provider, but card-not-present transactions often have a slightly higher rate due to the risks involved. To see how much it would cost to process MOTO payments with Helcim, check out our pricing here.

Related Articles

-

How credit card processing works: An ultimate guide

Danny Randell | March 3, 2021

-

Small Business Online Payments Guide

Ryleigh Stangness | August 2, 2020