B2B (business to business) payments are not too dissimilar from B2C (business to consumer) payments. Whether it's cash, credit cards, or electronic funds transfers, the main differences lay in who pays who and how. B2B credit card payments are just one branch of the credit card processing tree - let’s learn more about how they work.

Get introduced to B2B

Did you know: the global B2B market is predicted to create revenue of around $18 Trillion (USD) by the end of 2026. B2B payments are massive and are common in many industries, manufacturing, tech, and the wholesale industry being the top 3 biggest B2B industries.

If you are looking for quick and easy ways to take payments from other businesses, or streamline your payments, read on to see how you can manage outgoing and incoming B2B payments.

B2B payments vs. B2C payments

The main difference between B2B and B2C payments is the direction of payment. While both involve businesses receiving payments, B2B transactions are when a business pays another business, creating a business to business relationship. B2C, on the other hand, are transactions that take place between a business and individual consumers, creating a business to consumer relationship.

When businesses go about paying one another, it is usually different from the traditional "check-out" experience consumers are used to. Businesses often deal with large orders and don't typically visit the physical location or storefront (if there is one) of the business they are dealing with to make a payment.

Top 3 ways for businesses to pay each other

1. ACH

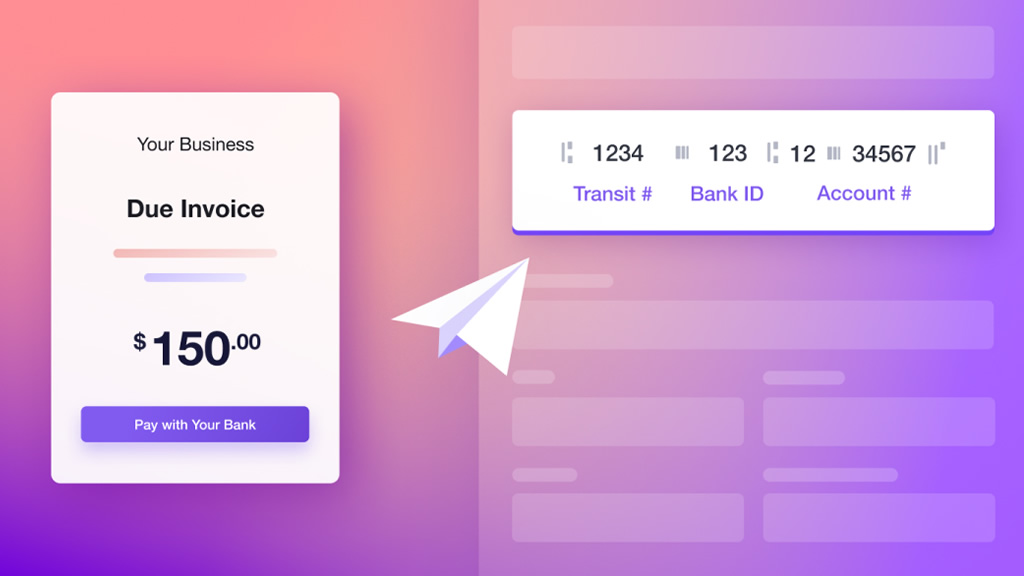

ACH stands for Automatic Clearing House and is the term used to describe the electronic transfer of funds in the United States, also known as Pre-Authorized Debit (PAD) in Canada. Online ACH transfers are bank-to-bank payments that use a business' or customer's financial institution information to directly pay a business for a product or service. The fees are lower than credit card processing fees, but ACH payments take longer to process, usually between 1-3 days.

ACH payments let you use your bank account to make payments instead of using a credit card. While many online payment platforms currently rely on credit cards for transactions, ACH is gaining momentum and is likely to become increasingly available for online payments in the near future, especially for B2B transactions.

2. Credit Cards

Accepting credit card payments are not just for individual consumers but are an incredibly powerful tool for many businesses in many industries. Making big purchases is easy with credit cards, as you don't need to deal with a large amount of cash or wait for a cheque or ACH payment to clear. A credit card transaction is instantaneous and can be done online through a payment gateway or processed over the phone.

3. Cheque

The good old-fashioned cheque is a tried and true payment method for businesses, and though the word on the street is that cheques are going away for good, many businesses still insist on using them, and they don't appear to be completely retired just yet. The downsides with cheques are rather obvious; they take a while to send and process, and you need to hope that when you give another business a cheque, they deposit it in a timely fashion; otherwise, you could end up with cash flow issues.

Even though cheques have been steadily declining, 33% of B2B payments in the US and Canada are still made via cheques.

Recurring billing For B2B payments

Recurring billing is very popular among business owners transacting with other businesses. An example of businesses needing recurring payments would be when wholesalers or contractors order supplies on a regular basis. Recurring billing can be done in different ways; in the past, it was not automated

Today however, recurring billing can be done electronically and via EFT (ACH/PAD) or credit card. All your business needs to set up a recurring billing cycle with another business is the purchasing business' credit card or banking information. If you use a payment processing software, once a billing date is agreed upon, you can simply set it and forget it.

Processing fees for B2B transactions

B2B transactions generally have lower credit card processing and interchange fees compared to B2C transactions. The Federal Reserve Payments Study on consumer and business payment choices concluded that an average B2B ACH debit transaction was $31,118, while a B2C transaction averaged $44. Understanding that B2B transactions are less frequent but involve significantly larger sums of money per average transaction than B2C transactions is crucial in understanding why credit card processing fees vary for both types of transactions. The more money a business processes, the more they need lower processing rates to be able to afford to take such a large sum of money.

With Helcim, the more you process, the more you save. We automatically lower your rates as your business processes more.

3 levels of credit card data processing

Did you know that credit card processing is made up of 3 layers of credit card data? While Level 1 is the basic payment processing, Level 2 and Level 3 are used for specific types of merchants, primarily for B2B sales.

Level 1

Level 1 processing is used by a vast majority of merchants that sell to consumers and is the most common type of credit card processing. Most small to medium-sized businesses (SMBs) fall within this level because card networks like Visa and Mastercard require merchants to process at least a million annual transactions to move to Level 2.

Level 1 requires the following data to be collected and submitted per transaction:

- Total purchase amount

- Purchase date

- Billing zip code

- Merchant's name

Level 2

By switching to Level 2 processing, merchants can see considerable discounts on interchange fees due to the higher quantity of sales they process annually. Even though merchants can continue processing as Level 1 even after surpassing a million transactions, there is reason to do so. In fact, merchants will be paying higher interchange fees with Level 1 compared to Level 2.

Level 2 transactions are eligible for businesses that process between 1 to 6 million transactions annually.

Level 2 requires the following data to be collected and submitted per transaction:

- Total purchase amount

- Purchase date

- Billing zip code

- Merchant's name

- Tax amount

- Merchant tax identification number (TIN)

- Invoice number

- Order number

- Customer code

Level 3

Level 3 requires the most data collection. However, eligibility for Level 3 is not contingent on the volume of transactions but rather on the ability to collect the additional data mentioned below. Processing Level 3 data can get interchange rates discounted even further, but the main key feature is reduced fraud risk and additional monitoring for safety, accountability, and compliance.

Level 3 requires the following data to be collected and submitted per transaction:

- Total purchase amount

- Purchase date

- Billing zip code

- Merchant's name

- Tax amount

- Merchant tax identification number (TIN)

- Invoice number

- Order number

- Customer code

- Product/SKU description

- Product code

- Unit price and unit of measure

- Unit quantity

- Discounts applied and line item total

- Debit/credit indicator

- Freight and/or shipping cost

- Duty and/or import taxes assessed

Final thoughts

Although not all that different from B2C payments, the tools and processes mentioned above will help your business take your payments with other businesses to the next level without having to worry about crazy high processing fees.