-

Content

Down payments do far more than get cash in the door. They cover your upfront costs, protect your time, and give you the confidence to commit resources without worrying about last-minute cancellations. But the benefits only come if you collect them the right way. Without clear terms, secure payment methods, and proper documentation, a deposit can turn into a dispute, or worse, a costly scam.

What is a down payment?

A down payment is an upfront portion of the total cost that your client pays before you deliver your products or services.

For merchants, a down payment confirms that the client is serious about the business, and it provides funds to cover the upfront costs of the projects, such as materials or labor. For clients, it can be looked at as a reservation fee or assurance that the merchant is committed to the project.

What are the differences between down payments, retainers, and advance deposits?

While many merchants use the terms down payment, deposit, and retainer interchangeably, these payment types actually serve different purposes. Below is the overall difference between down payments, retainer payments, and advanced deposits:

- Down payments are partial one time payments made toward the total cost of a product or project. They are commonly used for purchases like houses, cars, and other high-value items.

- Retainers are payments made to reserve a service provider’s time or availability. They are common in professional services like legal or consulting where service is required ongoing.

- Advance deposits are general upfront payments to secure a product, date, or service slot. They may or may not be deducted from the final amount. The advance deposits sometimes can be used as security deposits for home rental, hotel reservation, or vehicle rental.

Let’s compare each type of payment in detail below.

1. Down payment

A down payment is a partial, upfront payment made toward the total cost of a product or service. It represents the buyer’s commitment and gives the merchant the confidence and cash flow to begin sourcing materials, assigning labor, or reserving time.

The down payment is typically subtracted from the total amount when the product or service is delivered. For example, if a project costs $5,000 and the client pays a 30% down payment ($1,500), they’ll owe the remaining $3,500 when they receive the product.

Down payments are especially useful in milestone-based or one-time projects. They’re popular in industries like home renovations, custom goods, professional services, or any work that requires upfront investment from the seller.

2. Retainer

A retainer (also known as an advance fee deposit) is a payment made in advance to secure a service provider’s availability or ongoing support over time.

For example, a lawyer might charge a $3,000 retainer before taking on a new case. The funds are placed in a trust account and billed against as legal work is completed. If the case settles early and only $2,000 worth of services were used, the remaining $1,000 is refunded to the client — unless otherwise specified in the retainer agreement.

3. Advance deposit

An advance deposit refers to any money paid upfront to book appointments, reserve inventory, or secure time slots. Advance deposits aren’t always deducted from the final invoice.

For example, a wedding venue may require a $1,000 deposit to reserve a specific Saturday. Any additional services, such as food, beverages, or equipment rentals, are charged separately. Another common example is the security deposit collected at hotel check-in. This is typically an authorized payment hold that will be charged only if there’s damage during the stay.

If a deposit is non-refundable, merchants need to state that clearly in the invoice or contract. In both the U.S. and Canada, provincial or state laws often define what qualifies as a refundable or forfeitable deposit, especially for consumer purchases.

How much should a down payment be?

While there’s no universal rule, the down payment amount should be from 20% to 50% of the total project cost, depending on the industry, order size, and risk involved. For example:

- A down payment for a real estate purchase is 5% to 20% the real estate price

- A down payment for a contractor is from 10%-20% the project’s value

- A down payment for a car purchase is around 20% of the car’s price

The down payment will give you the peace of mind that the client is serious about the project, and all of the initial work you put in won’t be unpaid if they change their mind.

How to collect a down payment from a new client

To collect a down payment, you need to set expectations and create a clear, professional process that protects both you and your client.

- Discuss payment terms early

- Include the down payment in your written agreement

- Send a clear deposit invoice

- Offer convenient and secure payment methods

- Send a receipt and confirm project kickoff

1. Discuss payment terms early

Start the conversation about your down payment policy during the sales process, not after a proposal has been accepted. Surprising a client with a deposit request late in the process can make the clients feel hesitant and be a deal breaker.

Instead, explain upfront:

- Why you collect a deposit to cover upfront costs, reserve scheduling, and confirm commitment

- When it’s due (usually upon signing the contract).

- What the deposit amount is and whether it’s refundable.

This helps your client see it as a standard and fair part of doing business, which it is.

2. Include the down payment in your written agreement

Before any work begins, include the down payment amount and due date in your written agreement with the client. At a minimum, you should include:

- The total project price

- The deposit amount (flat fee or percentage)

- When it’s due, such as due upon contract signing

- What it covers (e.g. design phase, materials, scheduling)

- The refund policy, if any

3. Send a clear deposit invoice

Once the agreement is signed, you need to issue a deposit invoice to your client. This invoice should clearly indicate:

- That it’s a deposit or initial payment

- The amount due and the due date

- What the deposit applies to

- Remaining balance (if applicable)

- Your accepted payment methods

If you have a repeat client, you can use a Virtual Terminal to collect the payment on behalf of the client so that they don’t have to manually enter their payment details again. After the first transaction, the payment details are saved securely so that you can retrieve them and process repeating transactions faster.

4. Offer convenient and secure payment methods

The easier you make it, the more likely they are to pay on time. Make sure to work with a merchant service provider that provides multiple payment options, such as:

- Credit or debit cards: Convenient and widely accepted

- ACH or EFT bank transfers: Cost-effective for large amounts

- Interac e-Transfer (Canada): Fast and easy for domestic payments

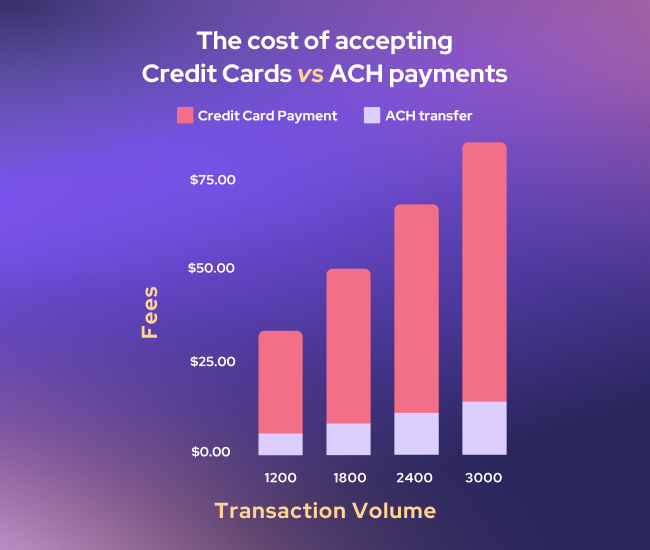

If the deposit amount is high, ACH (Automated Clearing House) is typically the most cost-effective method. For example, Helcim charges 0.5% + 25¢, capped at $6 for ACH transactions under $25,000, significantly lower than the 2.5% to 3.5% typically charged for credit cards.

5. Send a receipt and confirm project kickoff

Once the client submits the deposit, send a confirmation and thank-you message, for example: “Deposit received, thank you! We’ll now begin designing your project and will keep you updated on the next steps.”

This gives the client peace of mind that their payment was received and that the project is officially underway.

Best practices for collecting down payments from businesses

Collecting down payments correctly isn’t just about appearing professional; it’s also about protecting your time, managing risk, and keeping projects on track.

Having the best practices is even more important in B2B transactions because there is more money involved, more moving parts, more stakeholders, and longer timelines. A single missed payment or miscommunication can cost you weeks of lost time or leave you covering costs out of pocket. Below are best practices for collecting down payments.

1. Talk about the down payment early

Don’t wait too long to mention a down payment. Bring up the down payment early, ideally while discussing scope or pricing. Explain that the deposit secures their project timeline and allows you to commit resources to their work.

What could go wrong if you don’t talk about the down payment early? Imagine you’ve spent a week finalizing a proposal with a new client. They’re ready to move forward, until you mention the 40% deposit. Now they’re hesitating because the budget hasn’t been set for that early down payment yet. Then they need to “recheck the budget” or “run it by someone.” The momentum stalls, and you lose valuable time.

2. Put everything in writing, especially the payment terms

If you’ve worked with large corporations or handled structured deals before, you’ll know that putting everything in writing is standard practice. It’s common sense in those environments. But for solopreneurs, it’s understandable to want to move quickly and close the deal without too much friction. Still, you should never rely on verbal agreements when it comes to money.

A written agreement, even a short one, should clearly lay out the total price, the down payment amount, when it’s due, and what happens if the project is cancelled.

What could go wrong if you don’t put the down payment in writing? Let’s say a client pays a $1,500 down payment, but your email never mentioned whether it was refundable. A month later, they canceled and demanded their money back. Now you’re facing a standoff. Without clear documentation, you may be forced to refund the full amount, even if you have already spent hours on the project.

3. Explain what the deposit covers, not just how much it is

Most businesses want to understand what they’re paying for. That’s why it’s helpful to explain what the funds will go toward. Is it to cover design work? Secure materials? Lock in a project start date? Why do you need to do that? There may be multiple decision makers involved, so the more specific you can be, the easier it is for your client to justify the payment internally.

4. Choose a deposit amount that reflects your risk, not your gut feeling

There’s no magic number for a deposit. You can look at industry best practices to get a general idea of how much to charge, but that shouldn’t determine your pricing. The right amount depends on the size of the project, the timeline, the materials involved, and the level of risk you’re taking on to deliver the final product or service.

If the deposit is too small, you’re absorbing all the risk. If it’s too large without a clear rationale, clients may hesitate or feel uncomfortable.

5. Be crystal clear about your refund policy

Make your refund terms explicit, in your invoice, your agreement, and ideally in your verbal conversations as well. If the down payment is non-refundable, explain why. For example: “We reserve time and begin work immediately after receiving the funds, so the deposit cannot be refunded if the project is cancelled, as that time and effort have already been invested in the project.”

6. Don’t start working until receiving the down payment

It might seem like a small risk to begin “just a little” work while waiting for payment, but doing so puts your business in a vulnerable position if the client delays or walks away. For example, if a client wants to renovate their house but hasn’t paid a down payment yet, don’t start ordering materials or scheduling labor.

If they change their mind and cancel, you’re left covering the cost, and it could strain your relationship with suppliers. In some cases, you may have to absorb the loss entirely.

When should merchants collect a down payment?

You should collect down payments whenever you have to take significant upfront costs, high risks, or scheduling commitments before delivering the final products and receiving the final payments. Below are some common scenarios that you need to collect down payments:

- Custom or made-to-order products: If you’re creating something unique that can’t easily be resold, such as custom furniture, tailored clothing, or personalized art, a down payment is essential. It covers the upfront cost of materials, labor, and the risk you’re taking for that specific client. Without a down payment, you could lose money if the customer cancels, since the product is tailored specifically for them.

- Large projects or long-term services: In industries like construction, remodeling, or consulting, projects often take weeks or months to complete. In these cases, it’s best to collect a down payment upfront and then follow a structured milestone payment schedule as the project progresses.

- High-value goods or expensive orders: When the order value is significant, such as a bulk wholesale order or a high-ticket item that isn’t readily available, requiring a down payment is a smart move. It acts as a financial commitment from the buyer and reduces the risk that they’ll back out once the product is ready.

- Industries with scheduling demands or limited capacity: In fields like contracting, consulting, event venue rentals, or even healthcare and wellness services, you may only have a limited number of slots or resources available. A down payment helps secure the booking and protects you from no-shows or last-minute cancellations. For example, an event venue may require a down payment to reserve the space and begin planning logistics like decorations, food, and beverages. Similarly, an HVAC company might collect a down payment when a customer schedules an installation for the following month, ensuring the time and resources are properly allocated.

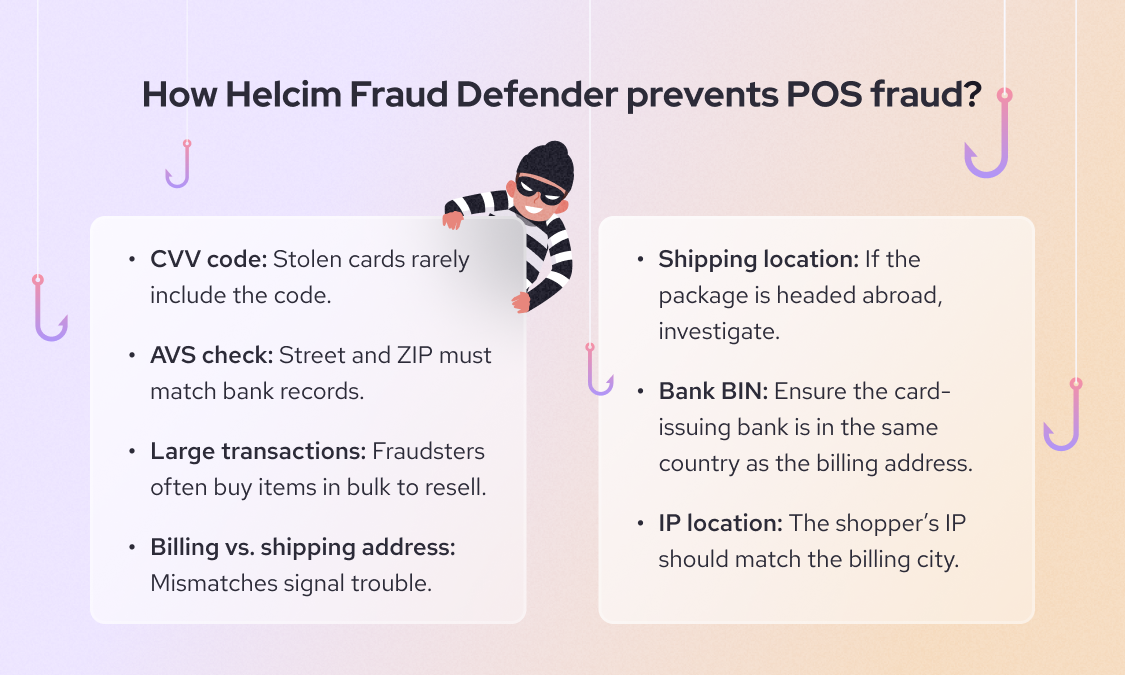

What are common down payment frauds and how to prevent them?

In B2B or high-ticket transactions, bad actors may act as potential clients, issue fake payments, or reverse legitimate ones. Whether you're selling services, high-value goods, or booking time in advance, here are common down payment frauds and how to protect yourself:

1. Avoid “overpayment” refund scams

A classic scam involves a “client” offering to pay more than the required down payment, then asking you to refund the difference. They’re not being generous; the initial payment is likely fake.

If they use a fraudulent check, it will bounce, meaning you’ll never receive the money. Worse, if you’ve already refunded the difference, you’re now out of pocket. Scammers may also use stolen credit cards. When the real cardholder notices the unauthorized charge and files a chargeback, the payment is reversed, and you're left with the loss.

If a client overpays you, never send a refund until you are absolutely certain that the original payment has cleared your bank. In some cases, especially with checks or ACH payments, this can take 30 to 45 days. In B2B transactions, ACH is the most common payment method, learn more on how to prevent ACH payments fraud here.

2. Watch for rushed or secretive behavior

Fraudsters often pressure you to act quickly, before you’ve had a chance to verify payment. For example, a scam buyer might urge you to start work or ship goods immediately after claiming they’ve sent the deposit. They may also say they’re in a hurry and can’t follow your usual procedures.

That’s a major red flag. If a customer pays by credit card, they typically have 30 to 45 days to file a chargeback and reverse the transaction. That’s why you should make sure your down payment terms are clearly written in the contract and signed by the client. This documentation helps your case if you need to dispute a chargeback later. Learn more about preventing online payment frauds here.

3. Identify suspicious transactions using fraud detection tools

Modern merchant service providers, like Helcim, offer built-in payment fraud detection tools that help flag unusual or high-risk transactions before they become a problem. These tools can alert you to mismatched billing details, unusual purchase patterns, IP address anomalies, or high-value payments from unfamiliar sources.

This extra layer of security gives you time to pause and verify the transaction, whether that means confirming the cardholder’s identity, calling the customer directly, or validating the legitimacy of a check. It’s a proactive way to catch fraud before it costs you money.

4. Avoid payment fraud using escrow for a large down payment

If the down payment is very large, or if you or the client wants extra security, consider using an escrow service. For example, for a huge project, the client could put the deposit in a third-party escrow that releases funds to you when certain conditions are met. This protects against fraud on both sides (the client knows you can’t run off with money, you know they genuinely funded the escrow).

This is more common in B2B or international deal payments. Once that goes fine, they can pay the rest of the deposit. Scammers are less likely to go through a multi-step process, whereas a real client might appreciate the flexibility.

What solution can you use to manage down payments from your customers?

The easiest way to collect and manage down payments is by using the right payment tools that make the process seamless for you and frictionless for your customers. Whether you’re collecting remotely, face-to-face, or over the phone payments, having flexible and secure payment options ensures you get paid on time and with fewer headaches.

Here are three key payment tools every merchant should consider for collecting down payments:

1. Invoicing software

Invoicing software lets you create and send digital invoices to your customers, usually by email or link, with clear details about what they owe, when it's due, and how they can pay. Helcim’s invoicing software lets you collect partial payments as a down payment by percentage or amount for the invoices. This makes your billing process more transparent and flexible. Explore the best invoicing software for small businesses here.

2. Virtual terminal

A virtual terminal is a secure online interface where you can manually enter a customer’s payment information to process an online payment without payment hardware.

Virtual terminals are ideal when you’re dealing with clients over the phone, by mail (MOTO payments), or in other non-face-to-face settings. Always ensure you have a signed contract before processing any transactions, so you can prove the legitimacy of the payment if a chargeback or refund request occurs.

3. Payment terminal (card reader)

A payment terminal (or card reader) is a physical device that allows you to accept credit and debit card payments in-person if you meet clients on-site, whether at your store, office, or a job location. A payment terminal makes it quick and easy to collect deposits face-to-face, with minimal friction. Modern card readers often support:

- Tap, chip, and PIN payments

- Digital wallets like Apple Pay and Google Pay

- Email or printed receipts

- Integrated invoicing and customer records

While payment terminals are convenient for in-person transactions, they may not be the best option for large down payments. High-value transactions often require additional verification steps or payment methods with lower processing fees, such as ACH or wire transfers. For this reason, payment terminals are more commonly used for smaller deposits or quick, on-the-spot payments.

FAQ

Can the customers use a credit card for a down payment on a car?

Yes, many dealerships allow customers to use a credit card for a car down payment, but there’s often a cap, usually between $3,000 to $5,000, to limit processing fees. The rest typically must be paid via bank draft, loan, or wire transfer. It’s best to confirm payment limits and policies with the dealership in advance. Keep in mind that using a credit card may increase your overall debt load and affect loan approval.

How do I handle a late down payment from a client?

If a client misses the deposit deadline, follow up with a polite reminder and re-send the invoice, emphasizing that work cannot begin until the payment is received. Delays may happen because there are many stakeholders involved in the process. If the delay continues, give them a firm deadline and consider offering an updated project timeline. In long-term delays, you may need to release the reserved schedule or cancel the agreement to avoid tying up your resources.

Can the customers lose a down payment?

Yes, customers can lose a down payment if the contract states it is non-refundable and work has already started or resources have been allocated. Courts typically enforce non-refundable clauses when they are clearly written, reasonable, and proportionate to the merchant’s losses. However, if the terms are vague or not disclosed, customers may be entitled to a full or partial refund. Always put refund policies in writing to protect both parties.

How to reduce risk when collecting down payments for high-value goods

To reduce risk, always use secure, traceable payment methods like ACH transfers or credit cards with fraud protection tools (e.g. 3D Secure, AVS). Require a signed agreement detailing what the down payment covers and when it’s due. Confirm that the payment has fully cleared before ordering materials or releasing goods. For especially large transactions, consider using escrow or third-party verification services for added protection.

Related Articles

-

Accept B2B payments: The ultimate guide

Robert Luong | March 3, 2025

-

How to collect an advance payment professionally?

Kaitie Weaver | February 21, 2025

-

ACH Payment vs Wire: Which one is better?

Ryleigh Stangness | October 11, 2023