Whether you're an established business owner or just starting out, finding the best ways to get paid can feel like searching for a needle in a haystack. But don't worry, we're here to be your guide!

We'll break down everything you need to know about B2B payments. We'll explore the different types of transactions, uncover hidden costs that could be eating into your profits, and how to get paid faster.

What are business to business (B2B) payments?

B2B payments, or business to business payments, are the transactions that happen between two businesses. They're not the same as B2C (business to consumer) payments. B2B payments are often larger in value compared to B2C payments and can be more complex as they may involve invoices, contracts and credit terms.

| Key difference | B2B payments | B2C payments |

|---|---|---|

| Typical transaction size | Larger—around $5,000 per transaction (often higher for enterprise). | Smaller—typically low to mid-hundreds. |

| Common payment methods | More complex: ACH/EFT, wires, checks; cards for some use cases. | Simpler: credit/debit cards, cash, wallets. |

| Relationship focus | Ongoing vendor–client relationships, contracts, negotiated terms. | Primarily transactional, one-off purchases. |

| Sales process | Longer and more complex (procurement, invoicing, approvals). | More straightforward and immediate checkout. |

In B2B sales, a typical example of a B2B payment is when a manufacturer pays a supplier for raw materials. Or it could be a retailer paying a wholesaler for inventory. B2C payments are more familiar to most of us. Think of buying groceries at the supermarket or purchasing a new pair of shoes online.

What are examples of B2B transactions?

Business to business transactions are the financial backbone of the business world. Without them, businesses can not receive the services and materials to produce goods and services to the end consumers. Let's take a closer look at how these transactions shape different industries:

Manufacturing: Imagine a car manufacturer needing tires for their latest model. They would purchase these tires from a specialized tire supplier to ensure the quality and safety of their vehicles.

Wholesale: Think of a clothing retailer stocking up on the latest fashion trends. They would source their inventory from a clothing wholesaler to ensure their shelves are filled with the new products for their customers.

Technology: Consider a software company developing an innovative application. They might rely on a cloud provider for hosting services to ensure that the users from around the world can access and use the software without interruption.

Healthcare: Imagine a hospital needing the equipment for diagnosis and treatment. They would buy this equipment from a medical supplier, ensuring they can provide the best possible care to their patients.

Professional Services: Think of a marketing agency creating a compelling campaign for a client. They might contact a freelance writer for specialized content creation to ensure their message resonates with the target audience.

What are B2B payment methods?

There are many ways for businesses to pay each other, the common B2B payment methods are:

- Debit cards

- Credit Cards

- ACH/EFT Transfers

- Wire Transfers

- Checks

Each payment method has its own advantages and disadvantages. Knowing the pros and cons can help your business decide the best B2B payment methods to use in different types of transactions.

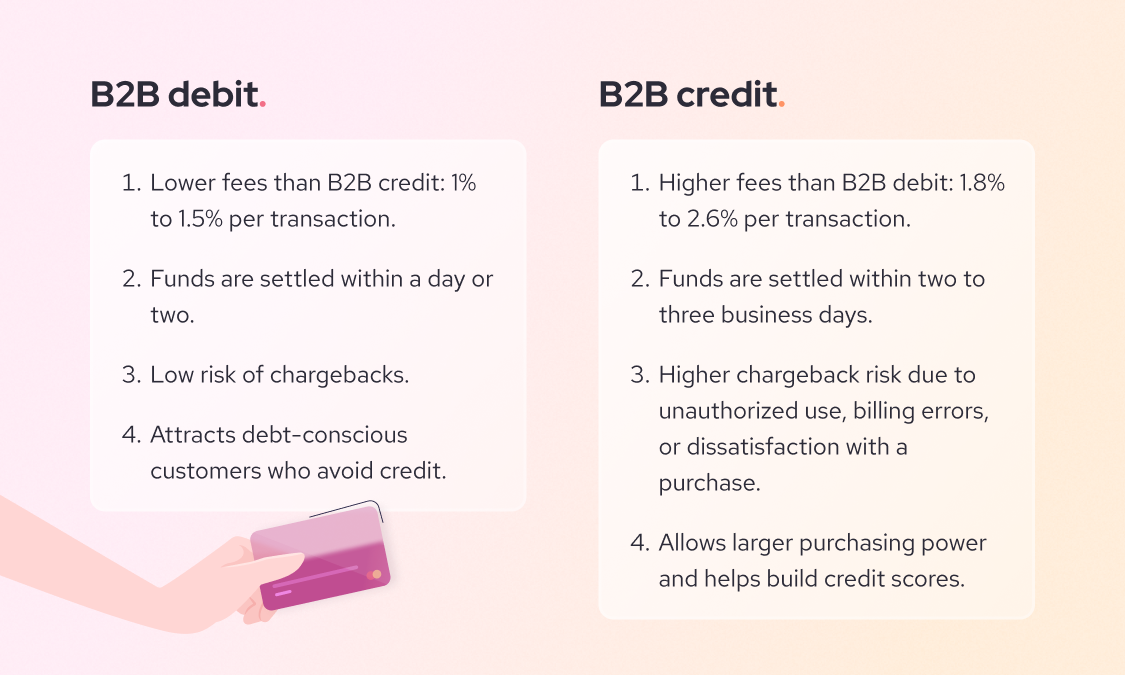

1. Debit cards

Debit cards offer a convenient way to pay directly from a business's bank account, without incurring debt.

If you spot the Visa or Mastercard logo on your debit card, then they are Visa Debit card or Mastercard Debit card. They work just like regular debit cards but they can also be processed through credit card networks. This means you can use them wherever credit cards are accepted.

However, the debit transactions processed via the credit card trail incur higher fees than traditional debit card transactions. Therefore, businesses should carefully evaluate whether the benefits of using a debit card outweigh the advantages offered by credit cards, such as credit score building, cash back, or rewards miles.

Besides, debit cards offer less protection against fraud compared to credit cards. If a fraudulent transaction occurs which is less likely than credit card, businesses may have a harder time recovering their funds.

2. Credit cards

Credit card transactions are popular choices for B2B payments because they are convenient and fast. With credit cards, businesses can make purchases online and in person. Unlike debit cards, where the money comes directly from the business's bank account, credit cards provide a line of credit that the business can use and pay back later.

Credit cards also offer some protection for buyers. If a client isn't happy with a product or service, or if there's been fraud, they can dispute the transaction and file a chargeback with their banks. This gives businesses some peace of mind when making purchases.

However, credit cards do have a downside: credit card processing fees. These fees can range from 2.5% to 3% of the transaction amount, which can eat into your profits.

Top processors with the lowest credit card processing fees for Canadian businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.39% (avg) + $0.25 | 1.76% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% + $0.30 to 3.3% + $0.15 | 2.5% |

| Stripe (flat-rate) | 2.90% + $0.30 + 0.5% for manually entered cards + 0.8% for international cards* + 2% if currency conversion is required | 2.7% + $0.05 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Top processors with the credit card processing fees for U.S. businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.49% (avg) + $0.25 | 1.93% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% to 3.30% + $0.30 | 2.60% + $0.15 |

| Stripe (flat-rate) | From 2.90% + $0.30 + 0.5% for manually entered cards + 1.5% for international cards + 1% if currency conversion is required | 2.70% + $0.50 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

The good news is that businesses can pass credit card fees to their clients by using surcharging or convenience fee programs like Helcim Fee Saver.

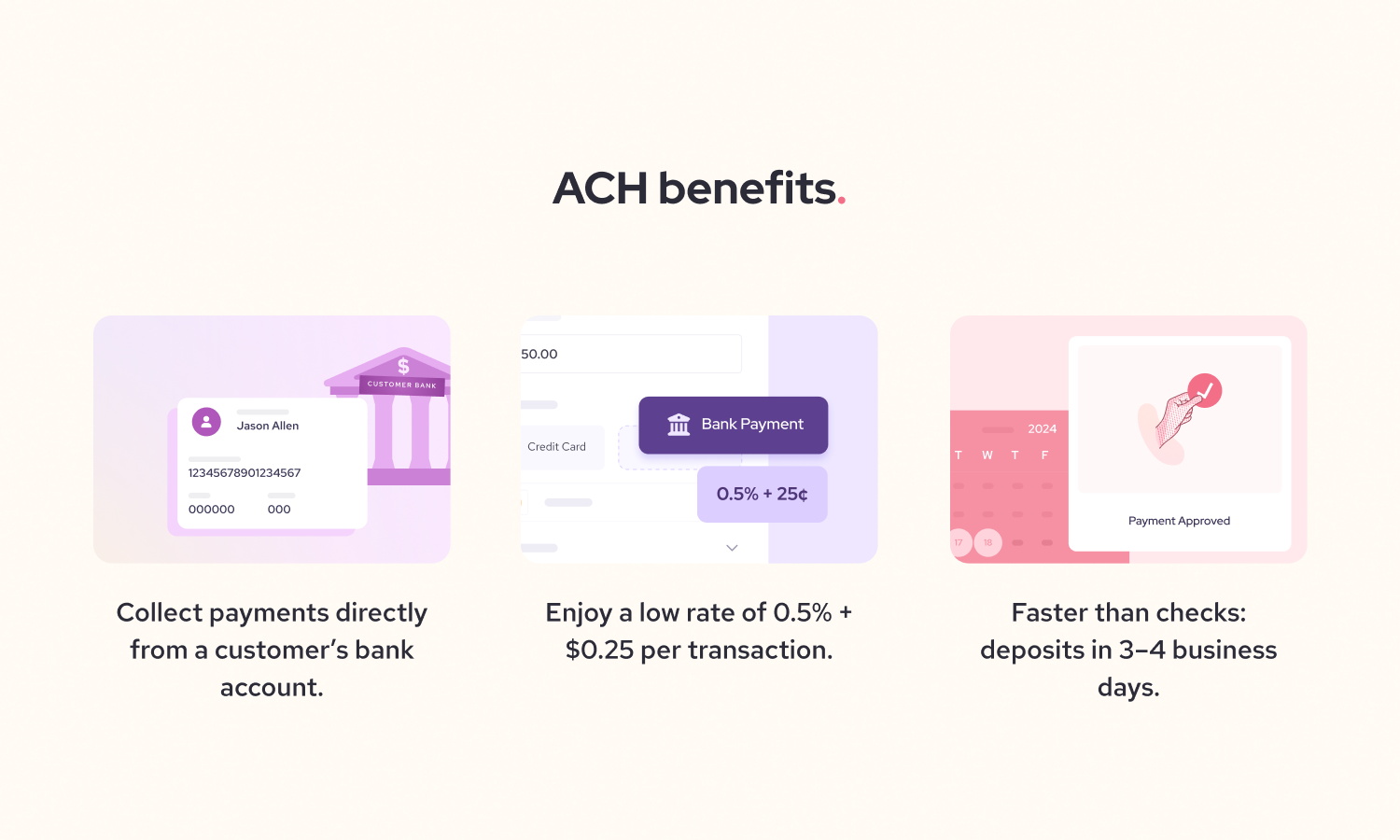

3. ACH/EFT transfers

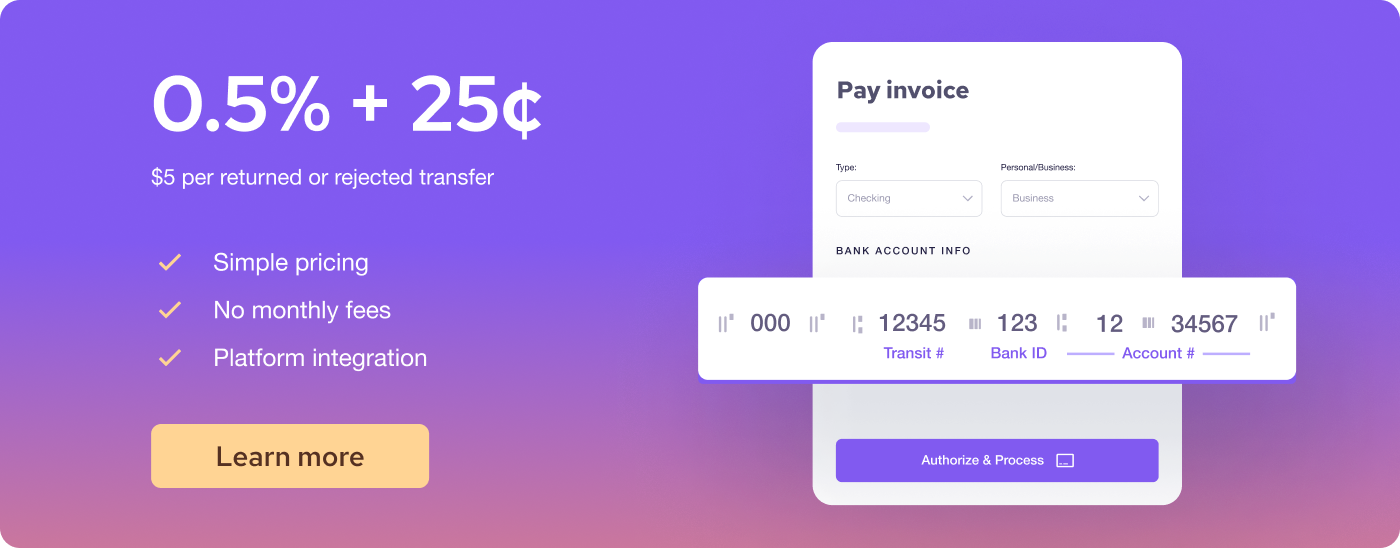

ACH (Automated Clearing House) transfers in the US and EFT (electronic funds transfers) in Canada are a popular choice for businesses looking to save. These electronic payment methods are much cheaper than credit cards, typically around 0.5% - 1% per transaction.

ACH/EFT payments are especially great for recurring invoices, subscriptions, and automated billing. They save time and reduce the risk of late payments. While ACH/EFT transfers can take a few business days to process, they're still faster than traditional checks.

4. Wire transfers

Wire transfers are like the express trains of the B2B payment world, known for their speed and security. Businesses use wire transfers when they need to send or receive money quickly and securely. They are also a reliable way to send money internationally, as transfers can be sent directly from one bank to another, often within the same day.

However, wire transfers can be expensive, with fees ranging from $10 to over $50, depending on the bank or financial institution. Additionally, wire transfers are typically irreversible, so it's important to double-check all the details before initiating a transfer.

5. Paper checks

Yes, some businesses still use checks! Businesses use checks when they need a familiar payment method, especially for smaller or less frequent transactions.

However, checks can take several days to clear, which can be a disadvantage for businesses that need to make or receive B2B payments quickly. Additionally, checks can be lost or stolen if the businesses don’t handle them carefully. There's also the risk of a check bouncing – if the payer doesn't have enough funds in their account, the check will be returned unpaid, and the payee may incur fees.

What are the most common B2B electronic payment methods?

Based on our data, credit cards are the most common B2B payment method.

- The B2B industry that uses credit cards the most is Laboratory Equipment Sales

- The B2B industry that uses debit cards the most is Appliance Wholesalers

- The B2B industry that uses ACH transfers the most is Accounting Auditing and Bookkeeping Services

Curious to see how your industry stacks up? Discover how often different B2B industries accept ACH transfers, credit cards and debit cards.

| Industry | ACH usage | Credit card usage | Debit card usage |

|---|---|---|---|

| Accounting, Auditing & Bookkeeping Services | 9.29% | 88.56% | 2.15% |

| Advertising Services | 0.45% | 99.49% | 0.05% |

| Appliance Wholesalers | 0.09% | 86.51% | 13.40% |

| Auditing Services | 0.00% | 78.89% | 21.11% |

| Building Contractors (Residential or Commercial) | 5.41% | 93.76% | 0.83% |

| Building Materials | 4.84% | 93.97% | 1.18% |

| Business Office Supplies | 0.10% | 99.70% | 0.20% |

| Construction Materials | 0.57% | 86.76% | 12.68% |

| Management Consultants | 8.42% | 91.53% | 0.06% |

| Marketing Consultants | 8.66% | 91.23% | 0.06% |

| Dental Equipment Sales | 0.21% | 92.97% | 6.82% |

| Retail Goods | 0.17% | 98.02% | 1.77% |

| Laboratory Equipment Sales | 0.14% | 99.86% | 0.00% |

| Legal Services & Attorneys | 1.15% | 97.38% | 1.46% |

Credit cards are the dominant payment method in most B2B transactions, frequently accounting for over 90% of payments. Industries like Advertising Services, Business Office Supplies, and Laboratory Equipment Sales overwhelmingly favor credit cards, with usage nearing 100% in some cases.

However, the use of ACH transfers, while generally low, shows some variability across industries. Accounting, Auditing, and Bookkeeping Services, along with Consulting Management and Marketing, demonstrate the highest adoption of ACH transfers, likely due to larger transaction values or recurring payments.

Besides, Appliance Wholesalers, Auditing Services, and Construction Materials saw the most debit card usage.

The data highlights the diverse payment preferences within the B2B landscape and the importance of offering multiple payment options to cater to specific industry needs.

How does B2B payment processing work?

B2B payments typically involve a series of steps that go beyond simply handing over a credit card or writing a check. Here's a general overview of how B2B payment processing works:

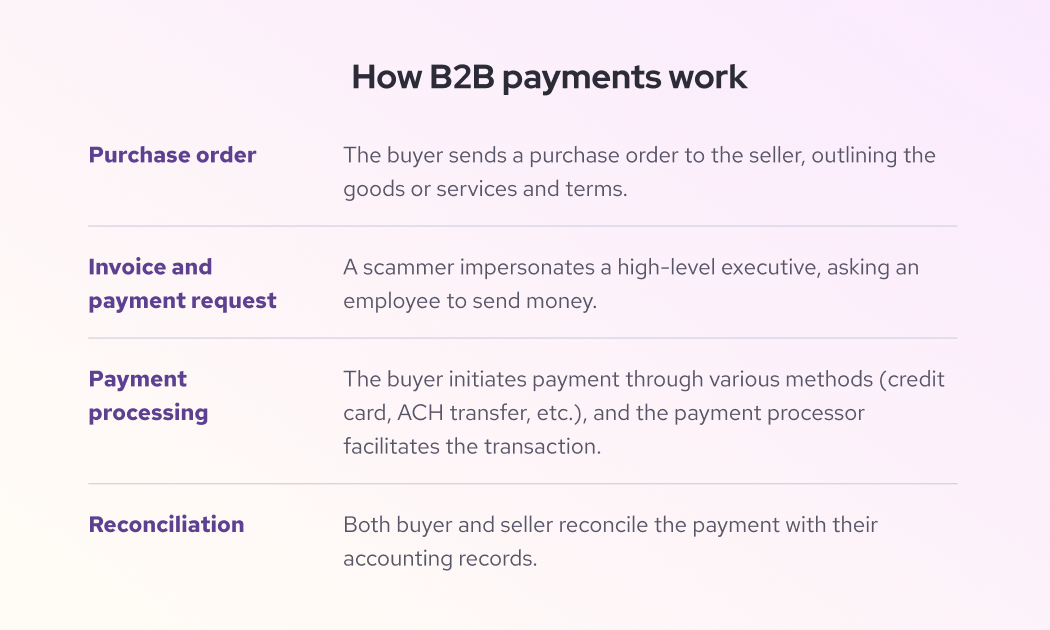

1. Purchase order

The process often begins with a purchase order from the buyer to the seller, outlining the goods or services being purchased and the agreed-upon terms.

For service-based businesses, such as law firms or agencies, a service agreement replaces the traditional purchase order. This contract outlines the scope of services, terms and conditions, and payment schedule, such as initial deposits, milestone payments, or recurring charges.

2. Send out a B2B payment request

Once the goods or services are delivered, the seller sends an invoice to the buyer, outlining the amount owed and the payment terms. For businesses with recurring services or goods, setting up recurring invoices can be a lifesaver. These invoices are automatically sent to clients on a regular schedule, like monthly or bi-weekly.

3. Process B2B payment

Once clients receive their invoice, they can proceed with their payments. Some businesses would have varying payment channels such as:

- Payment gateway: Some invoicing systems directly link to payment gateways. Clicking "pay" on the invoice redirects clients to a secure external payment page.

- Hosted checkout page: If your business has the branded checkout pages embedded on the websites,the invoices can direct your clients there to maintain brand consistency.

- Invoice with checkout: Modern invoicing software allows clients to pay directly within the invoice detail page.

Your clients can choose their preferred payment method, such as credit card, ACH transfer, or check. The payment processor receives the payment details and processes the transaction. Settlement can take 1-3 business days, depending on the method. Afterward, the payment is deposited into your business bank account.

Another handy tool is a virtual terminal. This allows businesses to retrieve saved payment information and bill clients directly on their behalf. Just remember to give them a heads-up before charging them to avoid any surprises.

Subscription-based businesses, like those offering SaaS products, can use recurring payments to automate billing. This means setting up automated charges based on the fixed amount clients subscribe to. With every payment cycle (usually monthly or bi-weekly), the payment processor automatically charges the set amount, saving clients from manual payments each time.

4. Reconciliation

Finally, both the buyer and seller reconcile the payment with their accounting records, ensuring everything matches up. The payment processor typically deposits the money into your account. There are two ways a payment provider can fund your account, either net deposits or gross deposits.

- Net deposits are the funds deposited into your bank account after deducting processing fees. For example, if you made $1,000 in credit card sales for the day, and your payment processor charges a 3% fee, you’d see $970 as your net deposit in your account.

- Gross deposits are the total amount deposited before deducting fees. For example, if you’ve made $1,000 in credit card sales, that full $1,000 appears as a gross deposit in your account. Then, a separate transaction charges the processing fees, which would be -$30 in this case.

It's important to know which type of deposit your payment processor uses for effective cash flow tracking.

How to accept B2B payments?

There are several tools that can help you accept B2B payments with ease and efficiency:

- Invoicing software

- Virtual terminals

- Payment gateways

- Point-of-sale (POS) systems

- Tap-to-Pay on iPhone

Why do these tools matter? Because without them, how will your clients actually pay you? You don't want to fumble around with outdated systems or tedious processes. You want to make it smooth and professional, just like the rest of your business.

Let’s explore how each tool works in more detail.

Invoicing software

Modern invoicing software helps businesses create and send professional invoices, track B2B payments, and collect their accounts receivable faster. It also simplifies the process of managing accounts payable, giving businesses a clear overview of their outgoing payments.

Imagine designing invoices that mirror your brand's personality, then effortlessly sending them via SMS or email. Your clients simply click "pay" and choose their preferred method, like credit card or ACH transfer.

Modern invoicing software also provides a dashboard to track all online payment—paid, due, or overdue. For overdue payments, you can use built-in email tools to send gentle reminders. If you have payment details on file, you can collect overdue invoices with a few clicks.

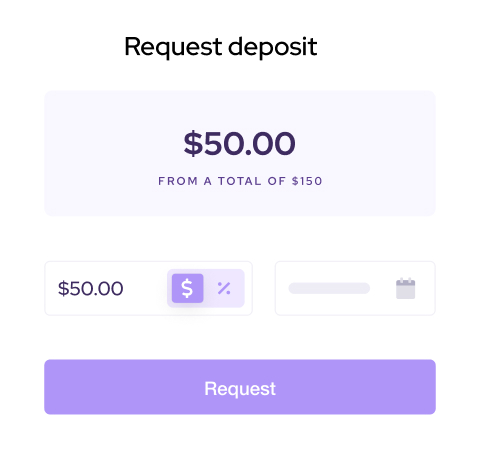

Need to accommodate clients who prefer making partial payments? No problem! Process partial payments for existing invoices with custom amounts or percentages. Offer flexibility and keep those transactions flowing smoothly.

Virtual terminals

Imagine having a superpower that lets you accept B2B payments anytime, anywhere, even without a physical card reader. That's the magic of virtual terminals! They allow businesses to accept online payments over the phone or by manually entering card details into a secure online system. With virtual terminals, businesses can process B2B payments from any internet-connected device, making them perfect for businesses that operate remotely.

For Helcim’s merchants, virtual terminals can retrieve invoice details and client information from built-in CRM tools to collect payments faster from repeat clients. By linking an invoice to a virtual terminal, businesses can process overdue, advance, or partial payments, offering greater flexibility for customers.

Hosted payment gateway

Want to add a checkout page to your website without writing a single line of code? A hosted payment gateway is your answer! This tool lets you create and customize a checkout page that integrates with your website, no programming required.

You can customize the information fields, the payment amount, and even the look and feel of the page to match your brand. You can choose which information fields to display or hide, such as billing and shipping details, and much more, depending on your business needs.

But what if you don't have a website? Simply turn your hosted payment page into a QR payment code or shareable payment link. Your clients can scan or click to visit the page and make their payments.

Hosted payment pages are perfect for collecting payments for consultation calls, deposits, or even one-time payment.

Point-of-sale (POS) systems

The point-of-sale (POS) system is like the control centers for processing in-person payments via credit cards, debit cards, and other mobile apps like (Google Pay or Apple Pay).

The POS system is made of software and hardware like barcode scanners, receipt printers, and customer displays. POS systems do more than just process transactions. They also offer a range of features to help you manage your business, such as:

- Inventory management: Track your stock levels, receive low stock alerts, and generate purchase orders.

- Employee management: Manage employee schedules, track sales performance, and control access to sensitive data.

- Customer relationship management (CRM): Build customer loyalty by tracking purchase history, offering personalized promotions, and providing excellent customer service.

- Reporting and analytics: Gain insights into your sales trends, track your inventory turnover, and monitor your employee performance. Learn more on how payment analytics improve your business performance in real-time here.

By syncing inventory and sales data across all sales channels, you can ensure that your in-person and online data are updated in real time.

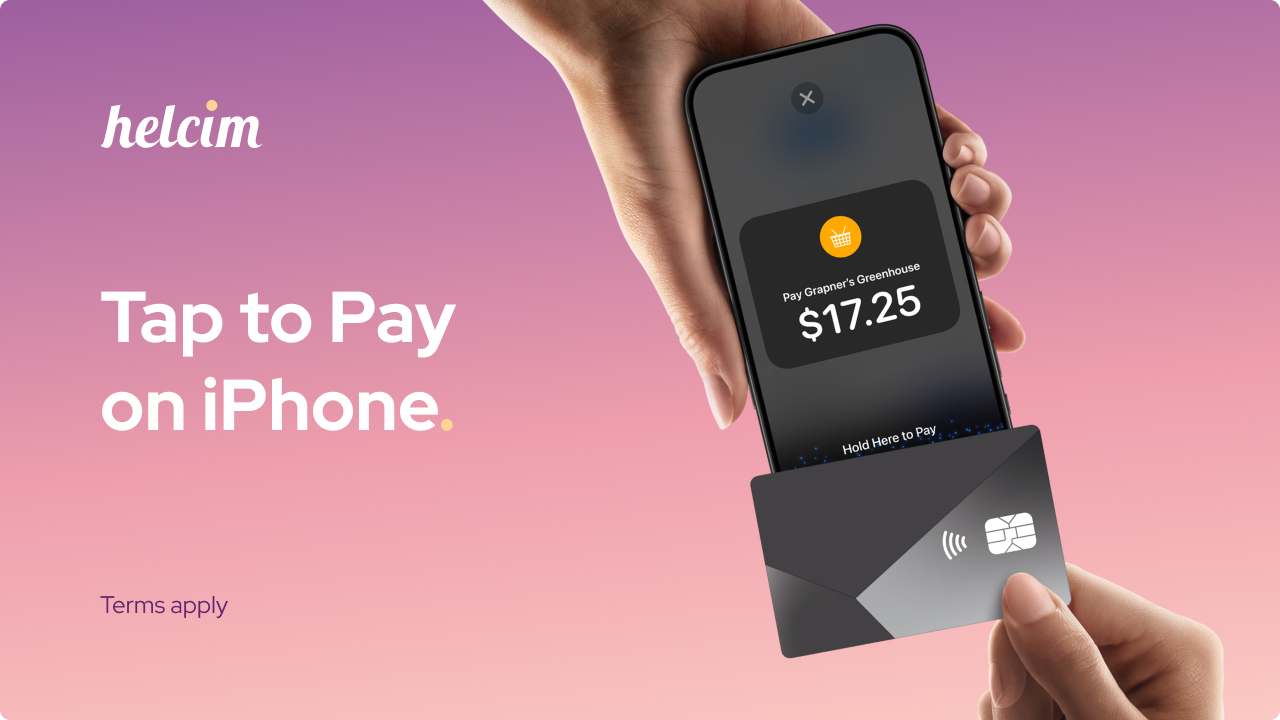

Tap-to-pay on iPhone

Imagine turning your iPhone into a portable payment terminal, ready to accept payments anytime, anywhere. That's the power of Tap to Pay on iPhone! If your business wants to accept payments without a card reader, Tap to Pay on iPhone is your solution.

All you need is a Helcim merchant account and the Helcim app on your iPhone. Turn on the tap-to-pay feature, and you're ready to accept payments from customers using contactless credit cards, debit cards, and even mobile wallets like Apple Pay and Google Pay. It's that simple!

Here are some examples of B2B businesses that could benefit from using tap-to-pay on iPhone:

- Delivery services: Wholesale business drivers can accept contactless payments upon delivery, right at the customer's doorstep.

- Sales representatives: After a successful client visit, sales representatives can collect payments directly through their iPhones, eliminating the need for extra paperwork or delays.

- Market vendors and food truck operators: Busy market days are no problem! Accept payments on the go, keeping lines moving and customers happy.

- Consultants and freelancers: Get paid on the spot when meeting with clients, simplifying your billing process and ensuring prompt payment.

How much does it cost to accept B2B payments?

We all want to get paid, but no one wants to break the bank doing it. Unfortunately, accepting B2B payments isn't always free. Here's a quick breakdown of the processing fees for different payment options:

- Debit card processing fees: 1% to 2.5% per transaction

- Credit card processing fees: 2% to 3% per transaction

- ACH processing fees: 0.5% + $0.25 (Helcim caps our fees at $6 for transactions under $25,000)

- Wire transfer processing fees: $10 to over $50 per transaction

- Check processing fees: $10 or more per check, depending on banks and the check amount

Why are credit card fees expensive?

Credit card fees are typically higher than debit card fees for two main reasons:

- Risk and reward: Credit card networks (like Visa, Mastercard, and American Express) and credit card issuers charge higher fees for credit card transactions due to the increased risk of chargebacks and fraud. These fees are passed along to merchants via credit card processors, but the processors themselves don't determine the fees.

- Rewards programs: Many credit cards offer perks like cashback or airline points. To fund these programs, credit card networks need to charge higher fees.

Want to keep more of your hard-earned money? Your business can reduce the credit card fees by:

- Working with payment processors that offer interchange plus pricing models, which offer the lowest credit card fees at the moment.

- Using a surcharging tool like Helcim Fee Saver to pass on the credit card fees to your customers, so you can keep more of your profit.

- Encourage your customers to use cost-effective payment options such as ACH transfers or debit cards.

What are hidden B2B payment fees?

Hidden B2B payment fees can be like those unexpected potholes on a smooth road, causing damage and frustration. Here are common hidden B2B payment fees to watch out for:

- Monthly minimum fees

- Early termination fees

- Subscription fees

- PCI compliance fees

- Initial setup fees & application fees

1. Monthly minimum fees

Some processors charge a minimum fee if you don't process a certain amount each month. These fees are common if you work with small payment processors who promise you a low rate which is too good to be true, such as below 1.5%. Make sure to check the contract to know what is the catch for these low processing fees.

2. Early termination fees

Having a contract with your payment processor is just how business is done? It’s not always the case! Some digital payment service providers try to trap you in contracts that can last three to five years. If things go south, you could be hit with cancellation fees anywhere from $250 to $5,000 or more. And if you're renting hardware, that's another termination fee on top of the processing contract cancellation fee. The bottom line? Read those contracts carefully! Understand the terms, length, and cancellation fees before you sign anything.

3. Subscription fees

Some payment processors charge an annual fee just for having an account, regardless of how much you use it. These fees can range from $30 to $50 or more per month.

While some subscription fees may cover valuable tools like specialized staff management tools, project management tools, or advanced reporting features, these features are not for everyone.

Before signing up with a payment processor, it's important to ask yourself if you will use all the features inside a plan or if there are any alternative processors that offer all of these for free.

4. PCI compliance fees

PCI compliance is a set of security standards designed to protect sensitive credit card information at every step of the payment process. Think of it as a fortress around your customers' data, keeping it safe from cyber threats.

Most payment processors, like Helcim, make PCI compliance easy. They provide a yearly self-assessment questionnaire (SAQ) that you complete to receive your PCI certificate. However, some processors might try to sneak in extra fees for PCI compliance, like quarterly or monthly charges. These are unnecessary as they just need to ensure you're completing your assessment.

5. Initial setup fees & application fees

Some payment processors charge a separate, non-refundable application fee, meaning you pay even if your application is declined. Even if your application is accepted, they will also charge an initial setup fee for your account. These fees can easily exceed $100 and are often hidden in the fine print of your contract.

How long do B2B payments take?

In the fast-paced world of business, time is money, and delayed payments can disrupt cash flow and hinder growth. So, how long do B2B payments actually take?

- Debit card settlement time: 24 hours

- Credit card settlement time: 1-3 business days

- ACH settlement time: 3-5 business days

- Wire transfer settlement time: 1-2 business days

- Paper check settlement time: 3-5 business days (or longer)

Of course, these are just estimates, and actual processing times can vary. One factor that can cause delays is when you suddenly process a large payment for the first time in a while. Some credit card processors might flag these transactions and temporarily hold your funds to verify their legitimacy.

Also, it's important to know that payments are processed in batches. Instead of transferring each payment into your bank account individually, payment companies group transactions together and deposit them in the next few business days.

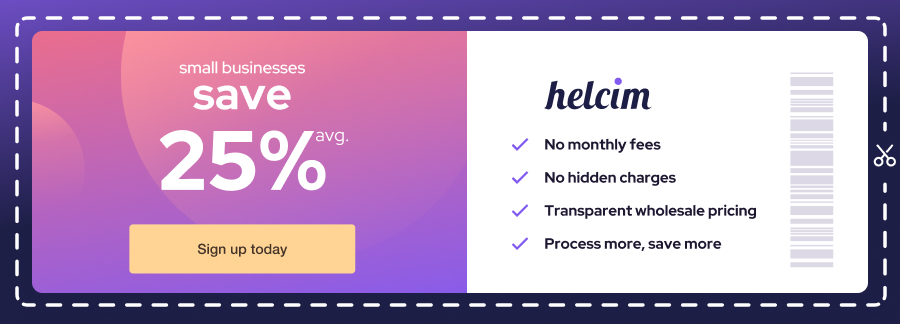

Accept B2B payments at low cost with Helcim

Ready to break free from those sky-high payment processing fees? Helcim is your escape route! With our Interchange Plus pricing model, you can save an average of 25% on credit card processing fees.

We offer a suite of tools designed to help businesses accept payments in person and online, with no monthly fees, contracts, or hidden fees.

- POS system: Set up a POS system to accept payments online and in person.

- Virtual Terminal: Collect payments from your computer, with no extra hardware.

- Invoicing: Design, send, and collect invoice payments.

- Recurring Payments: Automate your payment collection.

- Online Checkout: Build your online store and start selling online.

- Payment Pages: Add a checkout page to your website with no code required.

Sign up with Helcim today!

If you're stuck with your current payment provider, our Merchant Buyout program offers up to $500 in credits to cover your contract cancellation or equipment costs.

Plus, we'll guide you through the entire process, from handling cancellation paperwork to migrating your data to Helcim. Break up with your current provider for better service and lower fees.