Understanding the differences between POS debit and POS credit transactions is essential for both merchants and customers. Whether you're running a business or making a purchase, knowing how these transactions work can help you minimize fees, and reduce chargeback risks.

From how funds are processed to the fees involved, debit and credit transactions operate differently. This article will break down everything you need to know, including the types of transactions, limits, processing tools, and even alternatives like mobile wallets and online ACH bank transfers. By the end, you'll have a clear picture of how these payment methods fit into today’s fast-evolving marketplace.

What is a POS debit transaction?

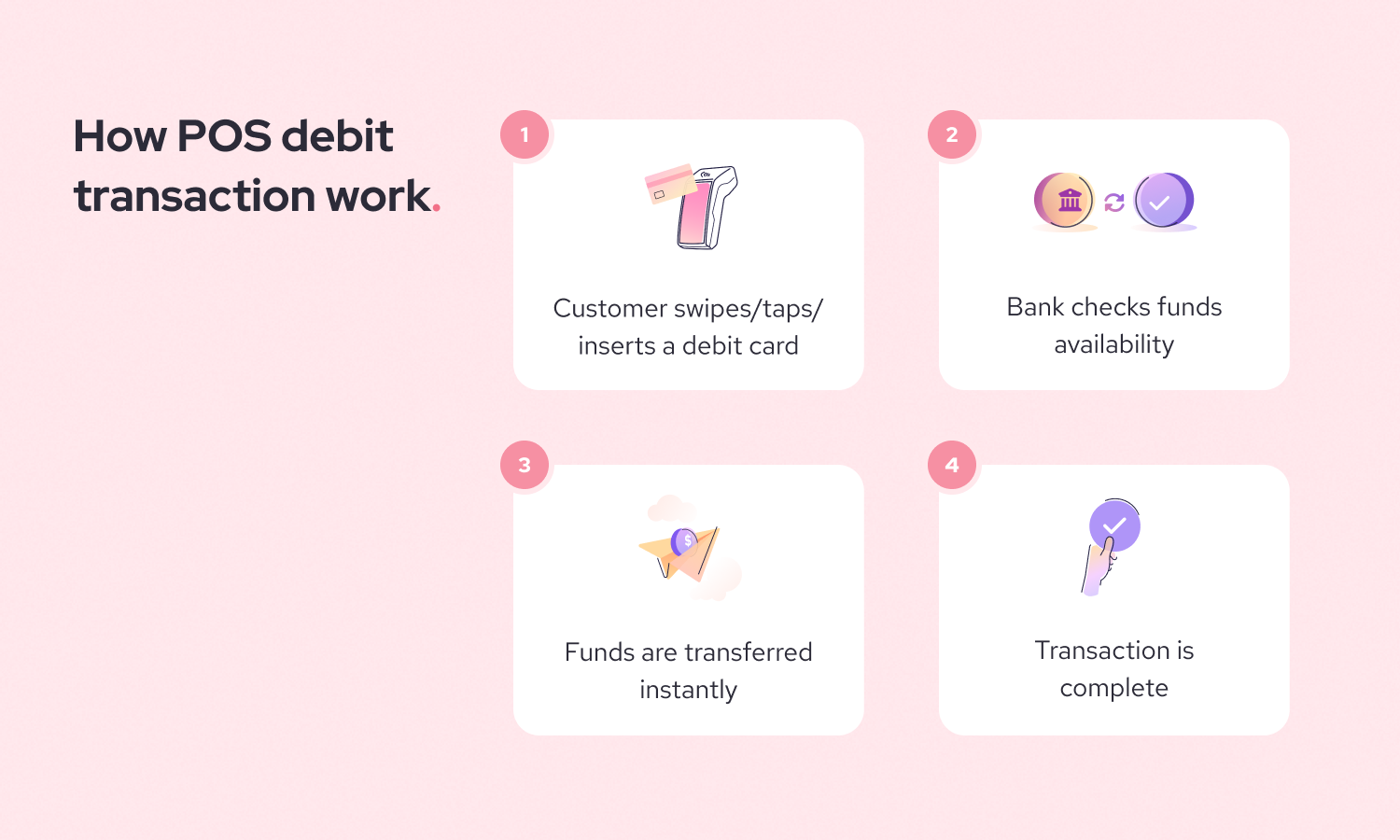

A POS (Point of Sale) debit transaction happens when someone uses their debit card to pay for something at a checkout counter or online. Think of it as an instant money transfer from the customer’s bank account to the merchant’s.

Here’s how it works: when you swipe, tap, or insert your debit card, the payment system sends a request to your bank to check if you have enough funds. If you do, the money is transferred right away, and the purchase is approved. As a result, the “POS debit” on your bank statement means your money was directly withdrawn from your bank account to complete a debit card purchase.

The key thing about POS debit transactions is that they’re direct and immediate. You can’t spend money you don’t have because it pulls directly from your bank account. This makes it a popular choice for everyday purchases like groceries, gas, or a coffee on the go.

What is a POS credit transaction?

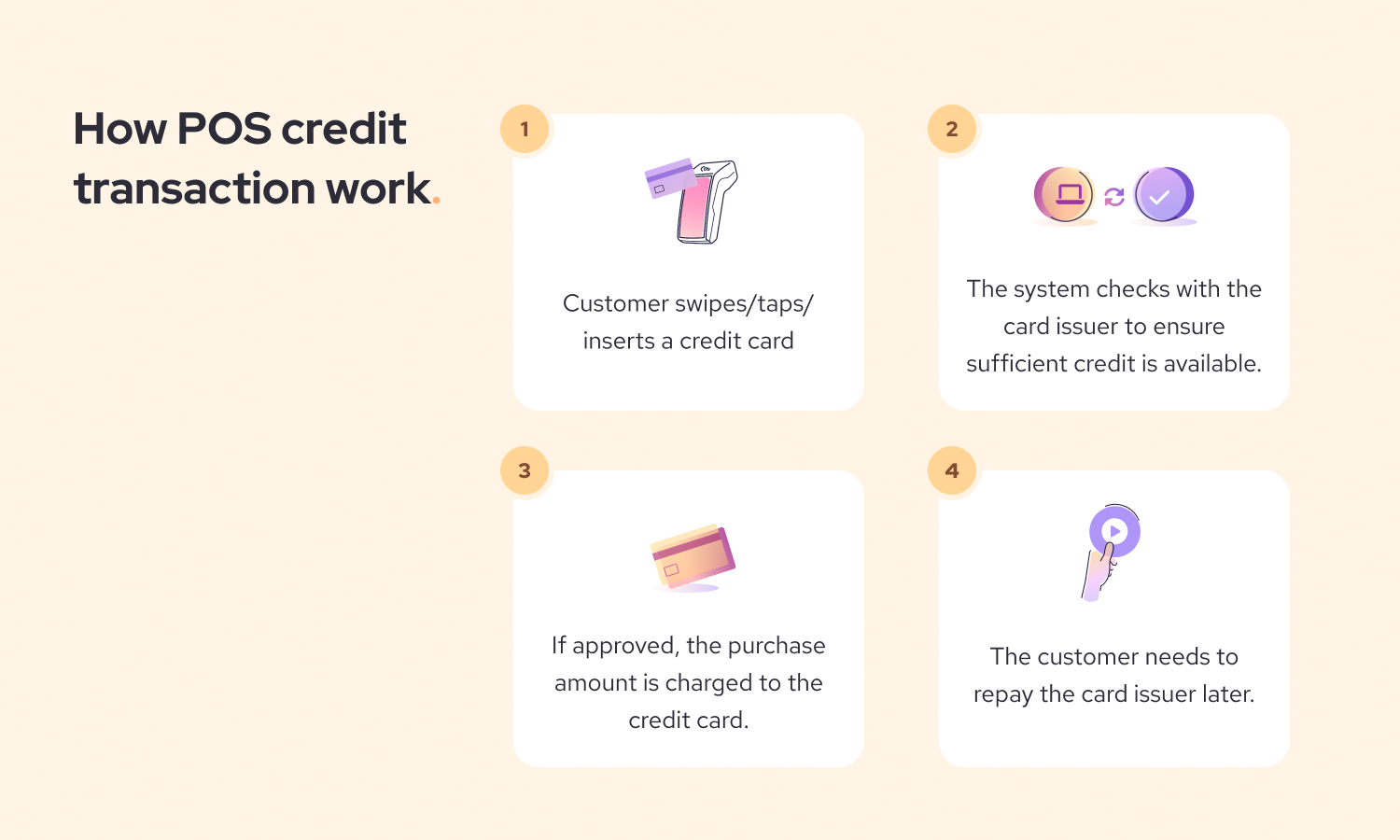

A POS (Point of Sale) credit transaction happens when someone uses their credit card to make a purchase. Instead of pulling money directly from a bank account, the transaction is processed on credit. This means the credit card issuer (the bank that issues the credit card) pays the merchant upfront, and the customer agrees to pay the card issuer back later, often at the end of the billing cycle.

Here’s how it works: when you use your credit card at checkout, the payment system checks with your card issuer to ensure you have enough credit available. If everything checks out, the purchase is approved, and the amount is added to your credit card balance. As a result, the “POS credit” on your bank statement means the purchase was charged to your credit card, and you’ll need to repay the credit card issuer.

One key feature of POS credit transactions is flexibility. They provide additional spending power, giving you breathing room for unexpected expenses or larger purchases. However, it’s important to remember that if you don’t pay off the balance by the due date, you might end up paying interest, which can be up to 25%, depending the type of credit card.

If your debit card has a Visa or Mastercard logo, it’s a Visa Debit or Mastercard Debit card. These cards function like regular debit cards, pulling funds directly from your bank account. However, unlike traditional debit cards, they can also be processed through credit card networks. As a result, you can use them anywhere credit cards are accepted—including online and for international purchases.

What is the difference between POS debit and POS credit transactions?

As a merchant, understanding the difference between POS debit and credit transactions is key to managing payments and costs. The main difference between POS debit and POS credit transactions are:

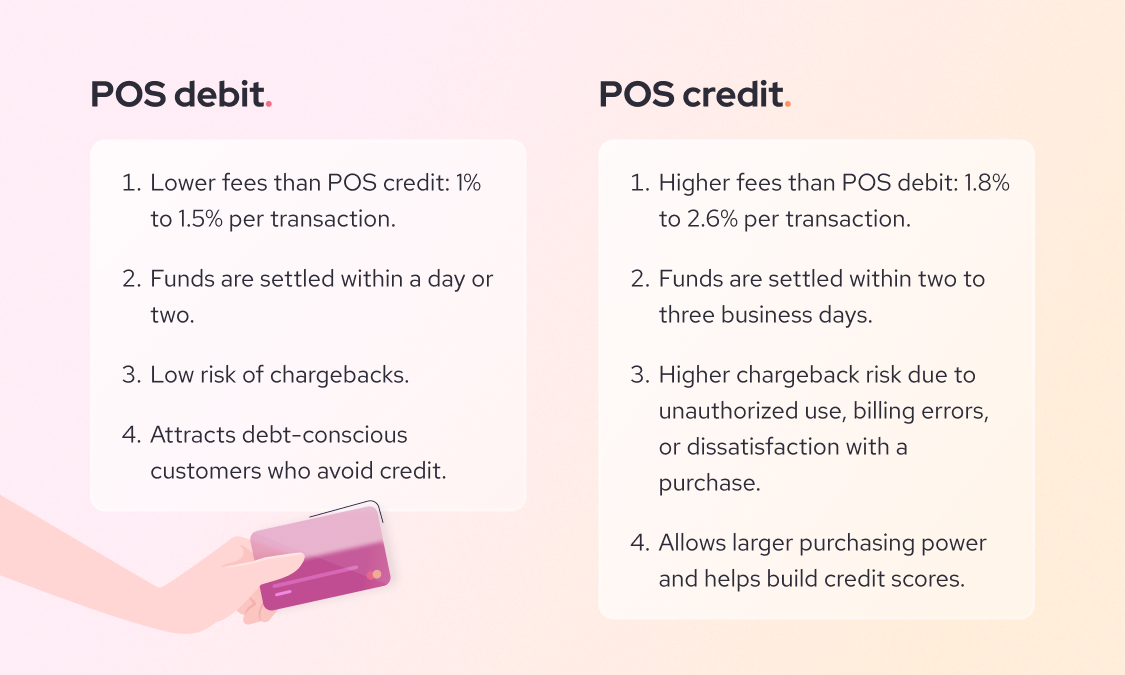

- Processing fees: POS credit transactions typically have higher processing fees than POS debit transactions.

- Settlement speed: POS debit transactions settle faster, often within a day or two, while POS credit transactions may take longer.

- Chargeback risk: POS credit transactions come with a higher risk of chargebacks, as customers have more dispute rights.

- Customer preference: Many customers prefer credit cards for their perks, such as rewards, cashback, and the flexibility to pay later.

1. Payment processing fees

POS debit: Payments are processed directly from the customer’s bank account to yours. The debit processing fees are low because they don’t involve credit risk. The debit transaction fees are around 1% to 1.5% for merchants.

POS credit: Payments are routed through the credit card issuer, which pays you upfront. However, the credit card processing fees are high due to the added risk for the issuer. This risk includes customers failing to repay their debt, disputes over charges, fraudulent transactions from stolen cards, and the potential for chargebacks. Because of the higher risks, the POS credit transaction fees are 1.8% to 2.6% on average for merchants.

2. Speed of settlement

POS debit: Funds are typically settled faster, often within a day or two. This quick processing time is because POS debit transactions do not require credit risk evaluation or the additional layers involved in credit card processing.

POS credit: Settlement might take a bit longer because they involve more steps. After a credit card is used, the payment must go through the card network, be authorized by the card issuer, and finally be cleared for settlement by the payment processor. Depending on your payment processor’s schedule, this can take two to three business days or more.

3. Risk and chargebacks

POS debit: Lower risk of chargebacks since the customer must have the funds available. However, disputes can still occur.

POS credit: Higher chargeback risk because credit card customers have more dispute rights, which could lead to additional administrative costs. Customers can file a chargeback for reasons such as unauthorized use, billing errors, or dissatisfaction with a purchase. To recover the funds, the merchants to provide evidence to dispute the chargeback claims. If the merchant's counter fails, they lose both the money from the transaction and the fees tied to the chargeback.

4. Customer preferences

POS debit: Often preferred for smaller, everyday purchases. Accepting debit cards can attract cost-conscious customers who avoid credit.

POS credit: Allows customers flexibility and larger purchasing power, making it a must for big-ticket items.

By accepting both POS debit and credit transactions, you can cater to a broader range of customers while balancing costs and risks in your payment strategy.

What are the different types of POS debit and POS credit transactions?

As a merchant, it’s helpful to understand the different types of POS debit and credit transactions available to ensure you’re offering customers the best options. There are seven different types of POS debit and credit transactions:

- PIN-based debit transactions

- Signature-based debit purchases

- PIN-based credit transactions

- Contactless credit payment

- Installment payments (credit option)

- Signature-based credit card transactions

- Credit card hold transaction

1. Types of POS debit transactions

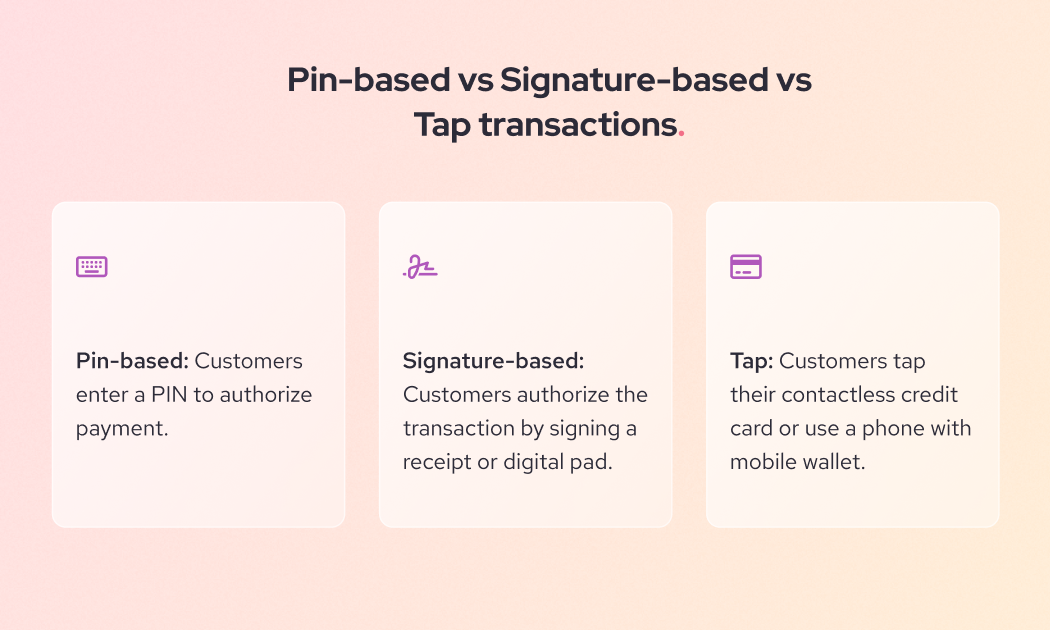

PIN-based debit transactions: This is the classic debit card transaction where customers enter a personal identification number (PIN) to authorize the payment. The funds are immediately withdrawn from their bank account. It’s secure, quick, and often has lower fees for the merchant.

Signature debit purchases: In this case, customers authorize the transaction by signing instead of entering a PIN. The funds are still pulled from their bank account, but because it’s processed through the credit card network, fees may be slightly higher than PIN-based debit.

2. Types of POS credit transactions

PIN-based credit transactions: Like PIN debit transactions, these transactions require customers to enter a PIN to authorize the payment. The key difference is that the transaction is charged to the customer's line of credit rather than directly debiting their bank account.

Contactless credit payment: With the rise of tap-to-pay technology, customers can use their contactless credit cards or mobile payments (like Apple Pay or Google Pay) for a fast, secure payment. It’s essentially the same as a regular credit card transaction but quicker and more convenient for both the customer and merchant.

Installment payments (credit option): Some credit card processors offer the option to split payments into installments. This type of credit transaction gives customers the ability to pay for larger purchases over time, often with low or no interest. It’s an appealing option for big-ticket items and can drive higher sales.

Signature-based credit card transactions: In a signature-based credit card transaction, the customer authorizes the payment by signing a receipt or digital pad instead of entering a PIN. These transactions are routed through their respective card networks and are less secure compared to chip or PIN-based methods, as signatures can be forged.

Credit card hold transaction: A credit card hold transaction is when a merchant temporarily reserves a certain amount of money on your credit card to make sure you have enough funds for a purchase. For example, when booking a hotel room, the hotel may place a hold on your credit card for the estimated cost of $600 to cover potential room service or other charges. If you check out without any additional costs, they will charge $500, and the remaining $100 hold will be released, usually within a few days.

By understanding these different types, you can make informed decisions about which options to offer your customers and how to optimize your payment processing.

What is the POS limit for debit cards and credit cards?

When customers use their cards, there are limits that can affect their ability to complete a purchase. As a merchant, it’s important to understand these limits and how they might impact transactions.

1. limits for debit cards:

Daily spending limits: Most banks set a daily limit on debit card transactions to protect against fraud. These limits typically range from $500 to $5,000, depending on the customer’s account and bank policies.

Insufficient funds: Debit cards pull directly from the customer’s bank account, so the transaction is limited to the available balance. If the account doesn’t have enough funds, the payment will be declined.

2. limits for credit cards

Credit limit: Credit cards are governed by the customer’s credit limit, which is the maximum amount they can charge on the card. This varies by card issuer and customer creditworthiness. For example, a customer with a $5,000 credit limit can’t make a $6,000 purchase because the purchase exceeds their credit limit.

Transaction-specific limits: Some credit card issuers may impose per-transaction limits for security reasons, especially on unusually large purchases. Besides, many banking apps allow customers to enable or disable international transactions as a security feature. If a merchant sells products internationally, customers with this setting enabled may unknowingly block their own purchases, leading to declined transactions.

Pre-authorization holds: For certain businesses (like hotels or car rentals), credit card issuers may place a temporary hold on the card for a specified amount. This reduces the customer’s available credit until the hold is lifted. Learn more about credit card pre-authorization payment here.

Why does POS limit matter for merchants?

Knowing these limits can help you manage customer expectations and avoid frustration at checkout. For example, if a customer’s debit card is declined due to insufficient funds or a spending cap, offering alternative payment methods like splitting the payment or using a credit card can save the sale.

What are the alternatives for POS debit and POS credit transactions?

While POS debit and credit transactions are common, offering alternative payment methods makes your business more versatile and appealing to a broader audience. The popular alternatives for POS debit and POS credit transactions are:

- ACH payments (direct bank transfers)

- Cash payments

- Checks

- Gift cards and store credit

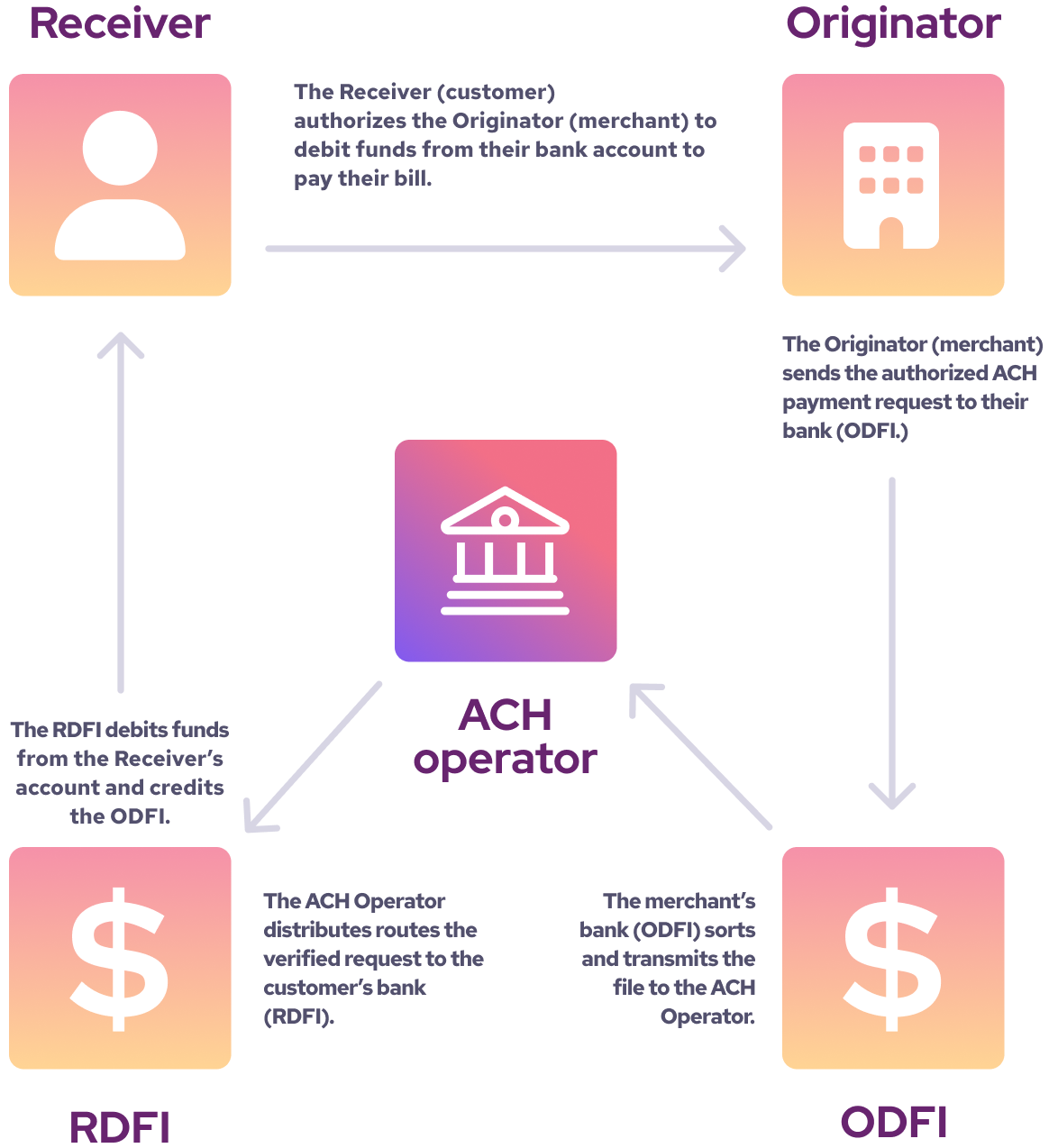

1. ACH payments (direct bank transfers)

ACH (Automated Clearing House) payments allow customers to transfer funds directly from their bank account to yours. This option is great for high-value transactions as it often comes with lower processing fees compared to cards.

2. Cash payments

If you want to process in-person payments, cash remains a reliable alternative. While it eliminates processing fees, it does require secure handling and can be less convenient for customers.

3. Checks

Although less common these days, accepting checks can still be useful for certain industries or high-value purchases. However, they involve additional risks, like potential check bounce fees.

4. Gift cards and store credit

Offering your own branded gift cards or store credit gives customers another payment option. These are especially effective for promoting customer loyalty and repeat business. By diversifying your payment options, you can better accommodate different customer preferences and reduce the risk of lost sales due to limited payment methods.

How to process POS debit and POS credit transactions?

Processing POS debit and credit transactions may seem technical, but it boils down to having the right tools and setup. Here’s how it works:

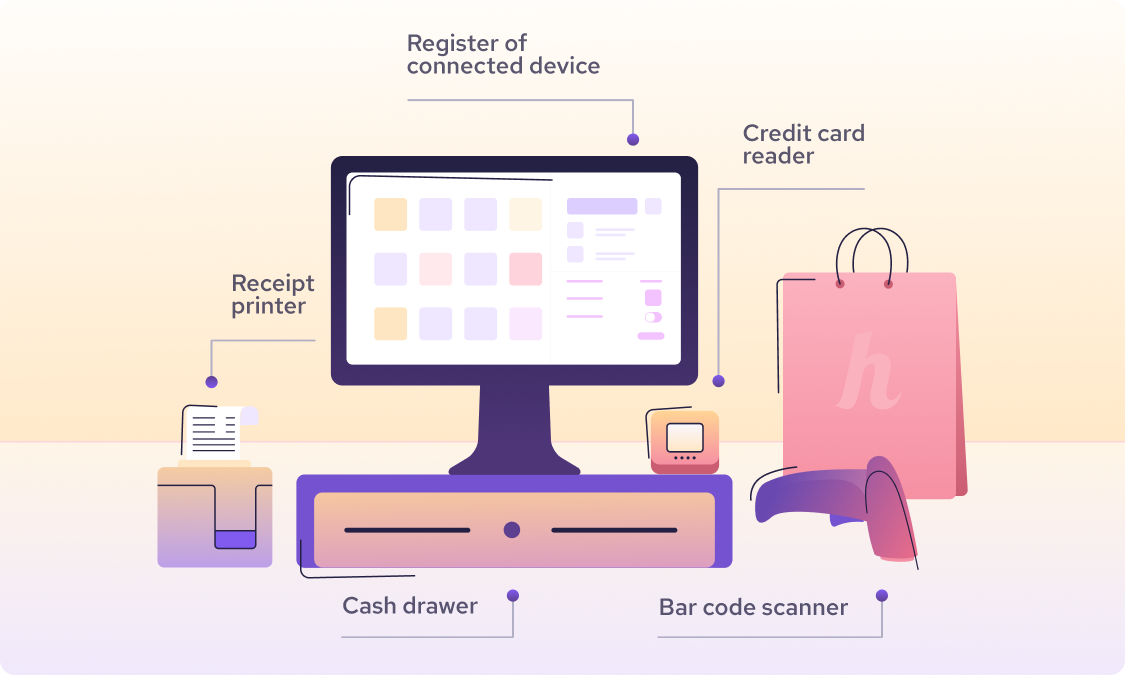

1. Set up a POS system

A reliable POS (Point of Sale) system is the backbone of processing both debit and credit transactions. Modern POS systems often include:

- Card readers compatible with chip, swipe, tap, and mobile wallets.

- Software that integrates with payment processors to handle the transaction.

For merchants running brick-and-mortar stores, a POS system equipped with essential hardware like a POS terminal, cash register, cash drawer, barcode scanner, and screen is crucial for processing POS debit and credit transactions seamlessly.

For online businesses, an online POS system with features such as invoicing, a virtual terminal, SMS payments, and recurring payment options is vital. These tools provide customers with flexible and convenient ways to pay for products or services.

2. Processing POS debit and credit transactions

PIN-based debit and credit transactions: For PIN transactions, your POS system must include a keypad for customers to securely enter their PIN. The system then verifies the funds or credits with the customer’s bank and completes the transaction.

Signature-based debit and credit transactions: Here, customers sign to approve the transaction. These payments are processed through credit card networks, so fees might be slightly higher than PIN-based debit.

3. Ensure PCI compliance

Security is crucial for processing payments. Make sure your system is PCI DSS (Payment Card Industry Data Security Standard) compliant to protect customer data. This includes encryption, secure storage, and regular software updates. While many payment processors charge annual PCI compliance fees, often ranging from $50 to $200 to cover certification costs, Helcim includes PCI compliance at no extra cost, making it easier and more affordable to keep your business secure.

4. Train your staff

Equip your team with knowledge about how the POS system works. They should know how to handle common issues, like declined cards, and assist customers with using the system efficiently.

By investing in user-friendly tools and ensuring compliance, you can offer seamless debit and credit transactions that enhance the customer experience.

FAQs

1. What does POS debit mean on the customer's bank statement?

A POS debit on the customer's bank statement indicates a transaction made using your debit card at a point of sale terminal. It shows that money was withdrawn directly from your bank account to pay for a purchase or service.

2. What is debit purchase vs credit purchase?

A debit purchase involves using a debit card to pay for goods or services, where the funds are directly withdrawn from the customer’s bank account. In contrast, a credit purchase uses a credit card, allowing the customer to borrow funds from their credit card issuer to complete the transaction. When these transactions are conducted online, they are referred to as online debit purchases or online credit purchases.

3. What are alternative POS debit descriptions in a bank statement?

POS debit transactions might appear with different descriptions, depending on the bank or merchant. Common variations include:

- "Point of Sale Debit"

- "POS Purchase"

- "POS Withdrawal"

- "Debit Card Purchase"

- "POS Transaction with Merchant Name"

4. What is a POS debit charge?

A POS debit charge is the amount deducted from your bank account for a transaction made using your debit card. This charge reflects the exact purchase amount and typically does not include extra fees unless it's part of the merchant's policy.

5. What does POS debit recurring mean?

A POS debit recurring refers to an automatic payment set up using your debit card. This is common for subscriptions, memberships, or regular bills where the amount is automatically debited from your account at regular intervals.

6. What does POS pending mean?

POS pending indicates that a debit or credit card transaction has been authorized but not yet fully processed. During this time, the amount is on hold in your account but hasn’t officially been deducted (debit) or added (credit). Once the transaction is cleared, the pending status will disappear, and the charge will finalize.

7. What is a POS withdrawal?

A POS withdrawal occurs when money is withdrawn directly from your bank account using a debit card at a point-of-sale terminal. For example, when you choose "cash back" at a store after a purchase, the extra amount withdrawn is considered a POS withdrawal.

8. What is the limit of a POS transaction?

The limit of a POS transaction varies depending on the type of card and the issuing bank:

- Debit cards: Daily spending limits usually range between $500 and $5,000, depending on the account and bank settings.

- Credit cards: The limit is based on the cardholder’s credit limit, which can vary widely. Additionally, some banks set transaction-specific limits for security reasons.