When your customers pay with a debit card, there's a lot more going on behind the scenes than just a quick tap, swipe, or insert. In this article, we'll walk you through what debit card processing fees are, how they are compared against credit card fees, and the different ways debit transactions are processed.

What are debit card processing fees?

Debit card processing fees are what your business pays whenever customers use a debit card to make a purchase.

These fees apply to in-person transactions, like when a customer swipes, taps, or inserts their card into a card payment machine. You also pay these fees for online sales when customers enter their debit card information at checkout.

If your business takes payments over the phone through a virtual terminal, you'll pay debit card fees when you manually enter the customer’s card details or use stored card information to complete the transaction.

How much is a debit card transaction cost?

Debit card transaction cost fluctuates with each debit card transaction and are made up of three main components:

- Debit interchange fees are paid to the customer’s bank to authorize the transaction and maintain the cardholder’s account. They fluctuate based on the type of debit card used and whether the debit transaction is processed in person or online.

- Card network fees (assessment fees) are paid to card networks like Visa, Mastercard, Interac, or US PIN Debit for using their network to process the transaction.

- The processor’s margin is charged by your payment processor to enable you to accept debit card payments.

Because true debit card processing fees fluctuate, many processors simplify things by applying a flat rate to all debit transactions, from 0.75% + 7¢ to 2.8% + 30¢. However, these rates are set high enough to ensure the processor remains profitable. This means you often overpay for most of the debit transactions.

A more cost-effective pricing model is interchange plus, which passes the actual cost of the debit card transaction to you, such as interchange fees + card network fees + 0.40% + 8¢. For example, Helcim’s interchange-plus pricing offers debit card fees as low as 0.40% + 8¢ in Canada and 0.40% + 98¢ in the US.

For a detailed interchange fee list, check out the US PIN Debit Interchange Fees here if you're a US merchant, or the Interac Network Interchange Fees here if you're a Canadian merchant.

Why do you have to pay debit card processing fees?

Even though debit card transactions are processed in the blink of an eye, there's a complex process behind the scenes that ensures everything runs smoothly from start to finish.

The debit card processing fees cover the costs of multiple institutions involved in making the transaction happen:

- Card-issuing banks: These are your customer’s banks that issue the debit card and hold the customer’s funds.

- Card brands or networks: Networks like Visa, Mastercard, Interac Debit (Canada), or PIN Debit (U.S.) facilitate communication between the payment processor and your customer’s bank.

- Payment processors: These companies provide payment solutions that allow you to accept debit card payments. They work with the card networks and issuing banks to authorize, authenticate, and settle the transaction.

- Acquiring banks (acquirer): These banks work with payment processors and card networks to authorize and complete transactions and deposit funds into your business account.

How does debit card processing work?

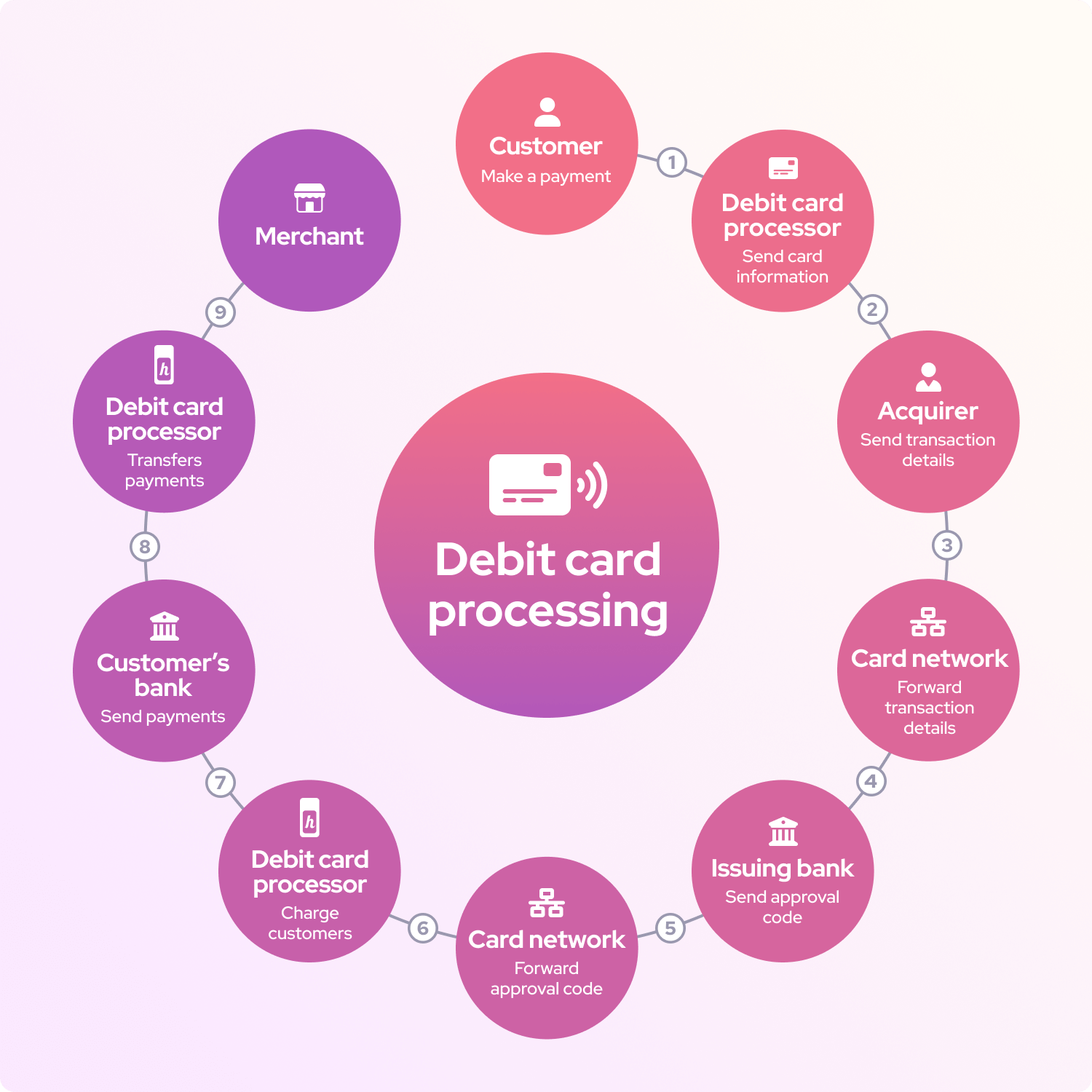

Debit card transactions follow a three-step process: authorization, authentication, and settlement.

1. Authorization

When a customer pays with their debit card, whether in-store or online, the debit transaction details (such as the card number and amount) are sent from your payment terminal to the payment processor. The processor then forwards the debit transaction through a card network, like Visa Debit, Mastercard Debit, or a direct debit network like Canada Interac or US PIN Debit.

2. Authentication

The card network communicates with the customer’s bank, which checks whether the card is valid and whether there are enough funds in the customer’s account. If the debit transaction is legitimate and the customer has enough money, the bank sends an approval message back through the network to your payment processor.

3. Settlement

Once the transaction is approved, the payment processor works with the card network to move the funds from the customer’s bank to your business account. This step ensures that the money reaches your account quickly and securely.

PIN Debit vs Signature Debit transaction: Which one is cheaper?

Debit card processing can be handled in two primary ways: PIN debit and signature debit transactions. Both methods allow customers to use their debit cards, but they work differently and affect how much you pay in fees.

1. What is the PIN Debit transaction?

With PIN debit transactions, your customers simply enter their personal identification number (PIN) at the point of sale after swiping, tapping, or inserting their debit card into the payment terminal.

These transactions are routed through a PIN debit network, like Interac in Canada or NYCE in the U.S. The security of entering a PIN makes these transactions safer and cheaper.

Because of the lower fees, PIN debit is a great option for businesses that want to keep their debit card merchant costs down.

2. What is the signature debit transaction?

Unlike PIN debit, signature debit transactions don’t require customers to enter a PIN. Instead, they simply sign a receipt in person or authorize the payment online. This makes the transaction to be processed like a credit card transaction.

Because these transactions go through the credit card network (like Visa or Mastercard), they come with higher processing fees because of risks like fraud or chargebacks. That’s why the cost of signature debit transactions can be pretty close to what you’d pay for credit cards.

Why are debit card fees lower than credit card fees?

At first glance, credit card and debit card transactions may seem similar—they both involve swiping, tapping, or entering card details to make a purchase. But they have different processing fees.

Credit card transaction fees are high because credit cards involve more risk for the banks. When a customer uses a credit card, they’re borrowing money from their bank. This means the bank takes on the risk that the customer may not repay that money.

Debit card transaction cost is lower than credit card transaction fees because the funds are directly withdrawn from the customer’s bank account for purchases. Since there’s no borrowing involved, there’s less risk for the bank.

Why are in-person debit card fees lower than online fees?

In-person debit card fees are lower than online fees because of the lower risk. When customers make in-person debit transactions, they physically present their card or enter a PIN at your store, making it easier for the payment processor to verify that the cardholder is legitimate. This lower risk of fraud allows banks and payment networks to charge lower fees.

In contrast, online debit card transactions are considered “card-not-present” transactions, where the cardholder isn’t physically present. Because it’s harder to confirm that the transaction is authorized by the actual cardholder, there’s a higher risk of fraud. As a result, banks and payment networks charge higher fees for online payments.

How can I lower my debit card processing fees?

You can lower your debit card processing fees by choosing a processor with an interchange plus pricing model that passes you the true cost of each transaction. Besides, you can encourage in-person transactions, as these typically have lower fees than online debit transactions.

You can also reduce debit processing fees by encouraging customers to use PIN debit transactions rather than signature debit transactions. PIN debit is processed outside the credit card network, which can lower debit card merchant fees. Additionally, choosing a payment processor that offers transparent pricing models can help lower overall fees for both debit and credit cards.

Can you pass debit card fees on to customers?

Surcharging is a method where merchants can pass the payment processing fees to customers who choose to pay with a more expensive payment method, such as credit card payments, instead of a preferred, cheaper option like cash or debit.

In the United States, merchants are not allowed to surcharge debit card or prepaid card purchases. This means you cannot pass debit card processing fees directly to your customers at checkout.

In Canada, merchants can add surcharges to debit card transactions in most provinces, but there are some important restrictions to keep in mind:

- You’ll need to check with your acquirer or payment processor first, as some networks don’t allow surcharging on debit payments.

- Surcharges are only allowed on Interac debit transactions. You can’t apply surcharges to Visa Debit, Mastercard Debit, or prepaid cards.

- The surcharge must be clearly displayed to the customer before they complete the debit card transaction, and they must have the option to cancel without any fees if they choose.

- In Quebec, consumer protection laws prohibit surcharges on debit transactions for consumers.

Save 25% in processing fees with Helcim

Switch to Helcim and start saving up to 25% on your processing fees, no monthly fees, no contracts, and no hidden costs—just transparent, affordable pricing.

Beyond the savings, Helcim gives you access to a full suite of tools to accept online and in-person payments for free. Getting started with Helcim now. No paperwork or signatures are required.

If you’re stuck in a contract with another provider, Helcim’s Merchant Buyout Program offers up to $500 in credits to help cover your cancellation or equipment costs.

FAQ

Do debit cards have processing fees?

Yes, debit cards do have processing fees, though they are typically lower fees than credit card payments. These fees are paid to the card issuing bank, payment network, and payment processor to cover the costs of authorizing and processing the debit card transaction.

What are the maximum debit card processing fees?

The maximum debit card processing fees without the processor’s margin can reach around 2.150% + 10¢ (for US Interlink Prepaid Commercial) and 5.5¢ (for Canada Interac Flash transactions). The maximum debit card fees are primarily determined by the network's interchange fees. Check out the US PIN Debit Interchange Fees here if you're a US merchant, or the Interac Network Interchange Fees here if you're a Canadian merchant.

Is debit card processing secure?

Yes, debit card processing is highly secure. Payment processors use advanced security measures like encryption, tokenization, and fraud prevention tools to protect cardholder information and safeguard your business from potential fraud.

Why are credit card processing fees higher than debit card fees?

Credit card processing fees are usually higher because credit card transactions involve more risk for the issuing bank and the credit card network. Debit cards cost merchants less because funds are directly pulled from the customer’s account.