-

Content

Choosing the best payment gateway in 2026 isn't just about transaction fees - it's about security, scalability, global reach, and long-term cost efficiency.

According to Statista's Digital Payments Forecast, global digital payment transaction value is projected to exceed $14 trillion in 2026. As online, contactless, and cross-border commerce continues to grow, businesses need payment infrastructure that is secure, transparent, and adaptable.

In this guide, we compare the top payment gateways in 2026, analyze pricing models, and answer the most searched questions to help you choose the right solution.

What Are the Best Payment Gateways in 2026?

Below is a side-by-side comparison of the leading gateways this year.

| Gateway | Pricing Model | Best For | Key Strengths |

|---|---|---|---|

| Helcim |

|

|

|

| Stripe |

|

|

|

| Square |

|

|

|

| PayPal |

|

|

|

| Adyen |

|

|

|

| Authorize.Net |

|

|

|

Helcim

Helcim's strengths are:

1. Transparent interchange-plus pricing: Helcim uses interchange-plus pricing, which separates the underlying card network fee from the processor markup. This transparency helps businesses clearly understand what they are paying and often results in lower costs compared to flat-rate models. As businesses grow, many realize flat-rate pricing can become expensive at higher volumes. Transparent pricing models such as interchange-plus allow merchants to better control payment costs as they scale.

Example: A growing healthcare clinic processing $30,000 per month may see meaningful savings with interchange-plus pricing compared to a flat-rate processor that charges the same percentage regardless of card type.

2. Automatic volume discounts: As processing volume increases, Helcim automatically lowers its markup. Businesses benefit from cost reductions without needing to renegotiate pricing tiers.

Example: A business that grows from $10,000 to $75,000 in monthly sales automatically benefits from lower transaction costs as their volume increases.

3. No long-term contracts: Helcim does not require long-term commitments or early termination fees, which gives businesses flexibility if their needs change.

Example: A seasonal retailer or startup can adopt Helcim without worrying about being locked into a multi-year agreement.

4. Clear fee breakdowns: Detailed statements allow merchants to see exactly what portion of each transaction goes to the card networks versus the processor.

Example: Finance teams can more accurately forecast payment costs and identify opportunities to reduce fees.

5. Strong customer support reputation: Reliable support can be critical when payment issues occur, especially for businesses that rely on payments for daily operations.

Example: If a merchant experiences a payment integration issue during a peak sales event, responsive support can help resolve it quickly and avoid lost revenue.

Overall Helcim is best for: Small and mid-sized businesses looking for transparent pricing and scalable payment infrastructure without hidden markups.

Stripe

Stripe's strengths are:

1. Deep API customization: Stripe offers one of the most robust developer platforms in payments, allowing businesses to build custom checkout experiences and payment flows.

Example: A SaaS company can design a completely customized subscription checkout with automated billing logic and usage-based pricing.

2. Subscription and marketplace infrastructure: Stripe includes tools for recurring billing, invoicing, and marketplace payouts, which simplifies complex payment flows.

Example: A marketplace platform can automatically split payments between vendors while handling subscription renewals for customers.

3. Multi-currency and international support: Stripe supports payments in many currencies and regions, helping businesses expand globally.

Example: A digital product company selling to customers in Europe, North America, and Asia can accept payments in local currencies.

Overall, Stripe is best for: Developer-led companies, SaaS platforms, and businesses that require highly customizable payment infrastructure.

Square

Square's strengths are:

1. Complete retail ecosystem: Square provides a full suite of tools including POS software, payment hardware, inventory management, and reporting.

Example: A coffee shop can manage in-store payments, track inventory, and generate daily sales reports from a single platform.

2. Hardware and POS integration: Square offers card readers, terminals, and registers designed to work seamlessly with its payment system.

Example: A retail store can accept tap, chip, and mobile wallet payments with minimal setup.

3. Fast onboarding: Businesses can start accepting payments quickly without lengthy underwriting processes.

Example: A pop-up shop or market vendor can begin accepting card payments within minutes of signing up.

Overall, Square is best for: Retailers and small businesses that need an easy-to-use payment system for both in-person and online sales.

PayPal

Paypal's strengths are:

1. Global brand recognition: PayPal is one of the most recognized payment brands worldwide, which can increase customer trust during checkout.

Example: An online store selling internationally may see higher checkout conversion when customers recognize a trusted payment option.

2. Digital wallet adoption: PayPal allows customers to pay using stored payment methods without re-entering card details.

Example: Returning customers can complete purchases quickly with one-click checkout.

3. Consumer trust and buyer protection: PayPal includes buyer protection features that can increase shopper confidence.

Example: Customers purchasing from a new ecommerce store may feel more comfortable completing the transaction using PayPal.

Overall, Stripe is best for: Ecommerce businesses selling internationally that want to offer a familiar checkout option for customers.

Adyen

Ayden's strengths are:

1. Unified global infrastructure: Adyen combines gateway, processing, and acquiring capabilities into one platform, reducing reliance on multiple payment providers.

Example: A multinational retailer can manage payments across multiple countries using one integrated system.

2. Local acquiring across many regions: Local acquiring can reduce cross-border transaction fees and improve authorization rates.

Example: A European ecommerce company selling in Asia may experience higher payment approval rates when transactions are processed locally.

3. Enterprise-grade fraud tools: Adyen offers advanced fraud detection and risk management tools designed for large-scale businesses.

Example: A global travel platform processing millions of transactions per month can monitor fraud patterns across regions.

Overall, Ayden is best for: Large enterprises or multinational businesses with complex global payment requirements.

Authorize.Net

Authorize.net's strengths are:

1. Established gateway technology: Authorize.Net has been a widely used gateway for many years and integrates with a broad range of ecommerce platforms.

Example: A business using an older ecommerce system may find built-in compatibility with Authorize.Net.

2. Works with many banks and merchant accounts: Authorize.Net can connect with multiple merchant account providers, giving businesses flexibility in how they process payments.

Example: A company that already has a merchant account through its bank can add Authorize.Net as the gateway layer.

3. Recurring billing tools: The platform includes built-in tools for subscription payments and automated billing.

Example: A membership site can automatically charge customers each month without requiring manual invoicing.

Overall, Authorize.net is best for: Businesses that already have a merchant account and want a reliable standalone payment gateway that integrates with many systems.

What Is a Payment Gateway?

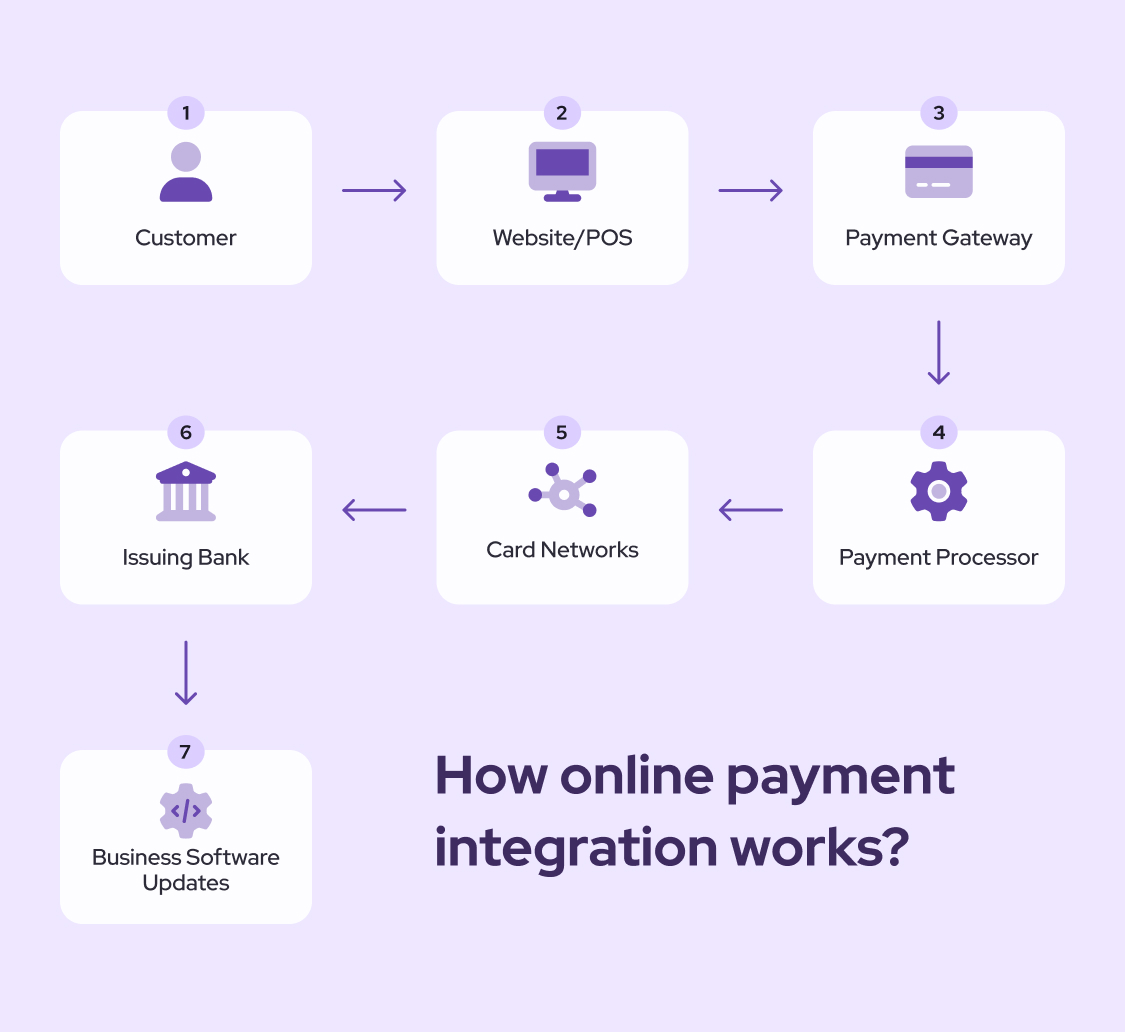

A payment gateway is technology that securely transmits payment information from your checkout to the acquiring bank for authorization.

It:

- Encrypts cardholder data

- Sends transaction details to card networks

- Receives approval or decline

- Returns the response within seconds

All legitimate payment gateways must comply with the PCI DSS security standards, which govern how cardholder data is handled and protected.

Payment Gateway vs Payment Processor: What's the Difference?

These terms are often used interchangeably, but they serve different roles:

- Payment Gateway: Securely transmits payment data

- Payment Processor: Moves funds between banks

- Merchant Account: Holds funds before settlement

Many modern providers bundle all three services into one integrated platform.

How much does a payment gateway cost in 2026?

In short, each transaction processed through a payment gateway costs your business from 2.3% to 3.5% depending on your payment processors and the pricing model.

| Fee Type | Typical Range |

|---|---|

| Flat-Rate | 2.6%–3.5% + $0.10–$0.30 |

| Interchange-Plus | Interchange + 0.2%–0.5% |

| Chargebacks | $15–$25 per dispute |

| Cross-Border | +0.5%–1.5% |

Other potential costs may include:

- Monthly gateway fees

- PCI compliance fees

- Currency conversion fees

- Chargeback handling costs

How to find cheap payment gateway?

To get find the cheap payment gateway, you should choose the payment provider that offers interchange-plus pricing model for payment processing fee.Payment processing fees can be confusing because the true cost of each transaction can fluctuate depending on the card type, issuing bank, and payment method used.

In general, most businesses encounter two common pricing structures: Interchange-plus and flat-rate pricing.

- Interchange-plus pricing: The processor charges you the actual card network cost and adds a small fixed markup. For example, 1.75% (interchange fee) + 0.40% (processor's markup) = 2.15%. This model is considered the most transparent because merchants can see exactly how much goes to the card networks and how much goes to the processor. Interchange-plus pricing is often preferred by businesses that process larger volumes because it can reduce overall costs as transaction amounts grow.

- Flat-rate pricing: The processor simplifies the fees by charging the same rate for every transaction regardless of card type. For example, 2.9% + $0.30 per transaction. Even though the underlying interchange fees vary, the merchant always pays the same amount. This model is easier to understand and can simplify accounting for small businesses, which is why many flat-rate providers focus on startups and low-volume merchants. However, because the provider must cover all possible card costs, the average rate can be higher compared to interchange-plus pricing.

The Federal Reserve Payments Study shows continued growth in card-based payments, which makes understanding fee structures increasingly important for profitability. Understanding these pricing structures can help businesses choose the model that best aligns with their transaction volume and growth plans.

For example, Helcim uses an interchange-plus model, where businesses pay the underlying card network cost plus a small transparent markup.

Understanding why these models exist requires a closer look at how payment processing fees actually work.

Why do true payment processing fees of payment gateway fluctuate?

Every time you process a card transaction with payment gateway, there are multiple parties participate in the whole process:

- The customer's issuing bank: The bank that provides the credit card to the customers

- The card network (Visa, Mastercard, etc.)

- The payment processor or gateway

- The merchant's acquiring bank

Each of these parties charges a small fee for their role in the transaction.

The largest component is the interchange fee, which is set by the card networks and paid to the customer's issuing bank. These fees vary depending on several factors, including:

- The type of card used (credit vs debit)

- Whether the card is rewards-based

- Whether the transaction is online or in-person

- The merchant's industry

- The country where the card was issued

Because of these variables, the cost of processing one transaction with payment gateway can be different from the next, even if the purchase amount is the same.

For example:

- A basic debit card might cost less than 1% in interchange.

- A premium rewards credit card might exceed 2%.

This variation is the reason different pricing models exist.

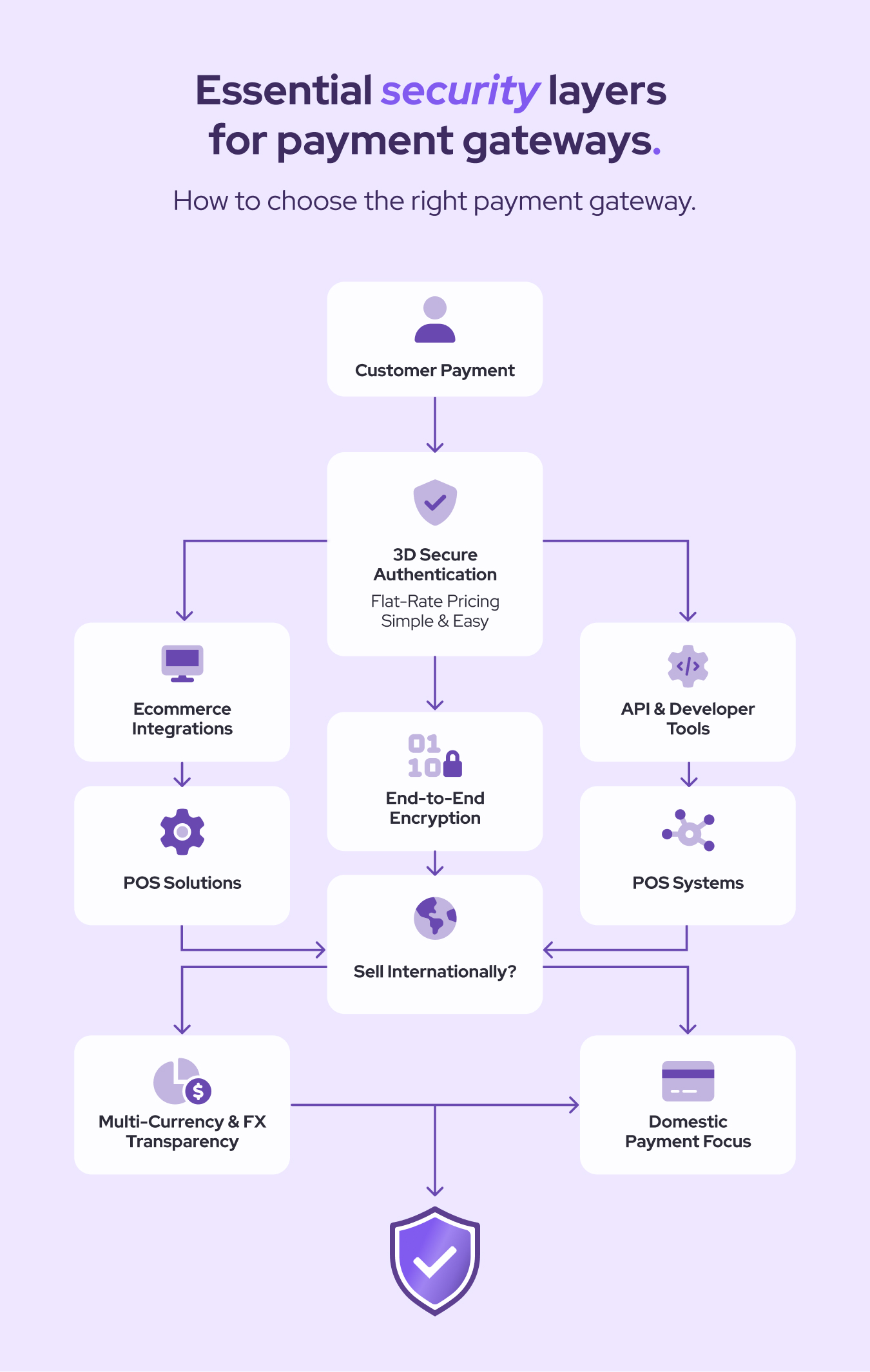

Which is the safest payment gateway?

The safest payment gateways are those that are PCI Level 1 compliant and offer card tokenization, end-to-end encryption, and fraud detection tools. Because these gateways handle highly sensitive financial data, any weakness in the infrastructure can expose businesses to fraud, chargebacks, and costly data breaches.

According to IBM's Cost of a Data Breach Report, the average global data breach cost reached $4.45 million.

To reduce these risks, businesses should look for payment gateways that include the following security features:

PCI DSS Level 1 Compliance

PCI DSS (Payment Card Industry Data Security Standard) Level 1 is the highest security certification for companies that handle cardholder data.

Why it matters: Payment gateways that meet PCI DSS Level 1 standards must follow strict requirements around encryption, secure network infrastructure, and ongoing security testing. This helps ensure that cardholder data is protected throughout the payment process.

Risk without it: Using a gateway that does not meet PCI DSS standards can increase the risk of data breaches and may expose businesses to regulatory penalties or liability if customer payment information is compromised

Tokenization

Tokenization replaces sensitive card data with a randomly generated token that has no exploitable value outside the payment system.

Why it matters: Even if a database is compromised, the stored tokens cannot be used to recreate the original card numbers. This significantly reduces the risk of stolen card data being used for fraud.

Risk without it: If a gateway stores raw card data instead of tokens, a breach could expose real card numbers, putting customers at risk and potentially leading to significant financial and reputational damage for the merchant.

End-to-End Encryption

End-to-end encryption ensures that payment data is encrypted from the moment it is entered by the customer until it reaches the payment processor.

Why it matters: Encryption prevents attackers from intercepting sensitive information during transmission between the customer, the gateway, and the payment processor.

Risk without it: Without encryption, payment data could be intercepted through network vulnerabilities or malicious software, increasing the risk of payment fraud and data theft.

3D Secure 2.0

3D Secure 2.0 is an authentication protocol designed to verify that the person making an online purchase is the legitimate cardholder.

Why it matters: This additional authentication layer helps reduce fraudulent transactions and can shift liability for certain fraud-related chargebacks from the merchant to the issuing bank. Learn more on how to spot and prevent card-not-present fraud.

Risk without it: Without strong authentication, merchants may face higher fraud rates and increased credit card chargeback, which can impact revenue and merchant account standing.

AI-Powered Fraud Detection

Modern payment gateways increasingly use machine learning and artificial intelligence to detect suspicious payment behavior in real time.

Why it matters: AI-based systems analyze transaction patterns, device information, and behavioral signals to identify fraud attempts before transactions are approved.

Risk without it: Payment gateways without advanced fraud detection tools may struggle to detect sophisticated fraud patterns, potentially leading to higher chargebacks and financial losses.

The safest gateway is one that combines compliance, encryption, and active fraud monitoring.

How should small businesses evaluate payment gateway?

When small businesses evaluate payment gateways, they should look for transparent pricing, no long-term contracts, reliable customer support, fast deposits, and easy integrations. Small businesses often face unique challenges when selecting a provider; while many advertise simple pricing or quick setups, hidden fees, restrictive contracts, or poor support can become costly over time.

Transparent pricing

Transparent pricing helps businesses understand exactly what they are paying for each transaction.

Some processors advertise simple rates but add credit card hidden fees, such as:

- PCI compliance fees

- Monthly minimums

- Statement fees

- Gateway access fees

- Inflated cross-border markups

Why it matters: Without clear pricing, it can be difficult for businesses to predict their true processing costs or compare providers fairly.

Example: A small ecommerce store might initially sign up for a provider offering a "simple" rate, only to discover additional monthly fees and higher effective transaction costs once sales increase.

No long-term contracts

Flexible agreements allow businesses to change providers if their needs evolve.

Some payment processors require multi-year contracts with early termination fees, which can cost hundreds of dollars if a merchant wants to switch providers.

Why it matters: Small businesses often experiment with different tools as they grow, and being locked into a long-term agreement can limit flexibility.

Example: A startup may discover that their original payment provider lacks features they need as they expand into subscriptions or international sales. Without contract flexibility, switching providers becomes expensive.

Reliable customer support

When payment issues occur, fast and knowledgeable support is essential.

Unlike large enterprises with dedicated technical teams, small businesses often rely on their payment provider for help with:

- chargebacks

- integration issues

- settlement delays

- fraud alerts

Some providers rely heavily on automated systems or ticket queues, which can slow down problem resolution.

Why it matters: Payment interruptions can directly impact revenue if transactions fail or accounts are temporarily restricted.

Example: If a merchant experiences payment failures during a major sales event, responsive support can quickly identify and resolve the issue before significant revenue is lost.

Fast deposits

Deposit speed determines how quickly businesses receive funds from completed transactions.

Some providers hold funds for several days or delay payouts due to internal risk policies.

Why it matters: Small businesses often depend on regular cash flow to cover operating expenses such as payroll, inventory, and marketing.

Example: A retailer that processes strong weekend sales may need those funds deposited early in the week to restock inventory.

Easy payment gateway integrations

Payment gateways should integrate smoothly with ecommerce platforms, accounting tools, and business software.

Some providers require complex technical setups or limited integrations with popular tools.

Why it matters: Small businesses typically operate with limited technical resources, so integrations that work out-of-the-box can save significant time and effort.

Example: An online store owner using WooCommerce payment integration or Freshline payment integration can connect payment gateway easily with their store and accounting software without needing custom development.

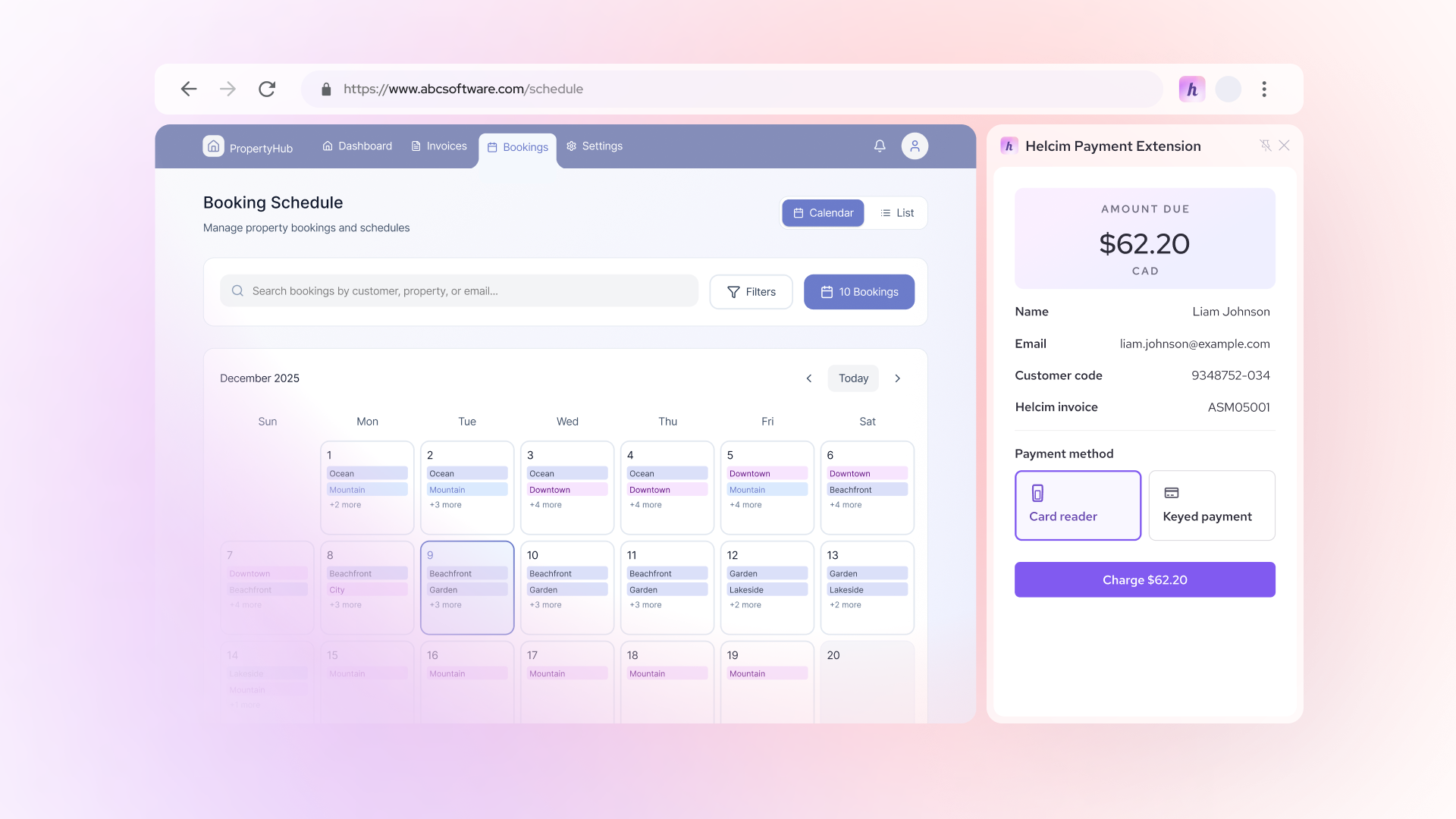

Some payment providers also offer tools that simplify payment acceptance even outside traditional integrations. For example, Helcim provides a browser-based payment integration that allows merchants to securely enter and process payments directly from their web browser. This can be especially useful when taking payments inside other web-based tools such as CRM systems, support platforms, or order management software-without requiring a full technical integration.

By reducing the need for complex development work, flexible integration options can help small businesses start accepting payments faster and operate more efficiently.

Credit card processing pricing models

As businesses grow, transaction volume increases and payment fees become a larger portion of operating costs. When this happens, you should choose the interchange-plus pricing model for credit card processing.

Flat-rate pricing can be convenient at low volumes, but interchange-plus pricing often becomes more cost-effective as businesses scale because merchants pay the underlying card network cost plus a smaller markup.

Understanding these pricing structures helps small businesses choose a payment gateway that remains affordable as their revenue grows.

What Is the Best Payment Gateway for International Payments?

The best payment gateway for international payments should support multiple currencies, offer competitive foreign exchange rates, maintain a strong network of acquiring banks, and comply with local regulations.

Cross-border ecommerce continues to grow globally, supported by initiatives from organizations such as the Bank for International Settlements and the World Bank's Payments Systems research aimed at improving international payment efficiency.

When evaluating a payment gateway for international transactions, several capabilities become especially important.

Multi-currency support

Multi-currency support allows businesses to accept payments in different currencies while displaying localized pricing to customers.

Most modern payment gateways support 100-135 currencies, allowing businesses to sell to customers worldwide without requiring them to convert prices manually.

Why it matters: Customers are more likely to complete purchases when prices are displayed in their local currency, which can improve conversion rates and reduce checkout friction.

Example: An ecommerce store selling digital products globally may allow customers in Europe to pay in euros while customers in Canada pay in Canadian dollars.

Transparent FX (foreign exchange) fees

Across the industry, the foreign exchange fees for payment gateway commonly range from 1% to 3% per transaction, depending on the provider and the currencies involved.

When payments are made in a different currency, the transaction must be converted to the merchant's settlement currency. Payment providers typically charge an additional foreign exchange (FX) fee for this conversion.

Why it matters: Hidden or unclear FX fees can significantly impact margins for businesses selling internationally. Transparent pricing allows merchants to accurately forecast their international sales costs.

Example: A Canadian ecommerce business selling to customers in the United States may pay a 1-2% FX fee when converting USD payments into CAD.

Local acquiring

Local acquiring refers to processing transactions through a payment processor located in the same country as the customer's issuing bank.

Why it matters: When payments are processed locally, transactions are often treated as domestic rather than cross-border, which can:

- Improve payment authorization rates

- Reduce cross-border interchange fees

- Lower the likelihood of fraud declines

Example: A European customer purchasing from a global ecommerce store may have their payment processed through a European acquiring bank rather than a North American one, increasing the chance the transaction is approved.

Regulatory compliance

Different countries have unique payment regulations that businesses must follow when accepting payments.

These may include:

- Data protection regulations (such as GDPR in Europe)

- Payment authentication rules like Strong Customer Authentication (SCA)

- Local card network requirements

Why it matters: Payment gateways that support regional compliance help businesses avoid failed transactions and regulatory issues when selling internationally.

Example: A gateway operating in Europe must support 3D Secure authentication to comply with SCA requirements under PSD2 regulations.

Enterprise platforms often excel here, but many modern SMB-focused providers now offer strong international capabilities.

How to Choose the Best Payment Gateway for Your Business

Ask yourself:

- What is my monthly processing volume?

- Do I need in-person payments?

- Am I selling internationally?

- Do I need recurring billing?

- Do I value pricing transparency

The "best" gateway depends on your business model, not just popularity.

FAQ

Is PayPal a payment gateway?

Yes, PayPal functions as both a payment gateway and a payment processor. It securely transmits payment data (gateway function) and processes transactions between banks (processor function). However, PayPal operates primarily as a payment aggregator, meaning merchants share a master merchant account rather than having a dedicated one. This allows for fast setup but may involve higher flat-rate fees and potential account reviews. Many businesses use PayPal alongside another gateway to offer customers a trusted wallet checkout option.

Do I need a merchant account to use a payment gateway?

It depends on the provider you choose. Traditional payment gateways require a separate merchant account to hold and settle funds. However, many modern platforms bundle the gateway, processor, and merchant account into one integrated solution.

A dedicated merchant account often provides more stability and may lower costs through interchange-plus pricing. Aggregated models offer faster onboarding and simpler setup but may include higher flat-rate fees. The right choice depends on your processing volume, risk profile, and long-term growth plans.

Which payment gateway is best for small businesses?

The best payment gateway for small businesses depends on transaction volume, pricing structure, and business model. Businesses processing lower monthly volume may prefer flat-rate pricing for simplicity, while growing businesses often benefit from interchange-plus pricing, which can reduce costs over time.

Small businesses should prioritize:

- Transparent pricing

- No long-term contracts

- Reliable customer support

- Easy integrations

- Fast deposits

Retail businesses may need POS integration, while ecommerce brands may prioritize subscription tools or international support. The "best" option is the one that aligns with your growth stage and cost structure.

Can you build your own payment gateway?

Yes, businesses can technically build their own payment gateway, but it requires significant infrastructure and regulatory compliance. A custom gateway must meet PCI Level 1 security standards, integrate with card networks and banks, and maintain fraud detection systems and secure infrastructure. Building and maintaining this system can be expensive and complex, which is why most businesses partner with established payment providers instead. For most companies, using an existing gateway is faster, more secure, and more cost-effective.

Related Articles

-

Payment gateway integration guide for small businesses

Booky | August 21, 2025

-

Refining payment gateway testing for secure transactions

Robert Luong | January 31, 2025

-

Payment Gateway vs. Merchant Account: What's the Difference?

Kiara Taylor | September 5, 2023

-

What is a payment gateway and how can it help your business?

Miranda Russell | September 17, 2022

-

How a hosted payment gateway can help you get paid online

Miranda Russell | November 17, 2020