You know the type—those cozy little cash-only spots. Maybe it’s a diner where the pancakes are the size of your plate, or a mom-and-pop corner store that hasn’t changed in decades. They’ve been sticking to cash since day one and haven’t noticed an impact on their businesses cash flow – until now.

With the shift to contactless payments and the rise of credit card acceptance, lots of small businesses are considering a transition away from cash only. At first, this change may seem daunting, but understanding the payment industry and researching credit card processing companies can help set your business up for a seamless transition.

Looking to make the switch from a cash only business and accept credit cards? Explore this article to help determine if adding credit cards as an accepted payment method is right for you.

What is a cash-only business?

A cash only business is exactly what it sounds like: a business that only accepts cash payments. No credit cards, no debit cards, no mobile payments—just good old-fashioned bills and coins.

These businesses are often small and local, like food trucks, barbershops, or corner stores. For some, it’s about keeping things simple. Cash is straightforward—no need to deal with payment processors, payment processing fee, or waiting for money to clear.

Others stick to cash transactions because it’s how they’ve always done things. It feels familiar and reliable. Plus, some believe it helps them avoid the risk of chargeback frauds or disputes that can come with card payments.

But there’s a flip side. With fewer people carrying cash these days, cash only businesses can lose sales if customers don’t have the right payment option on hand. And that’s where the debate begins: should they stay cash only or adapt to meet changing customer expectations?

Cash or credit? What today's customers prefer

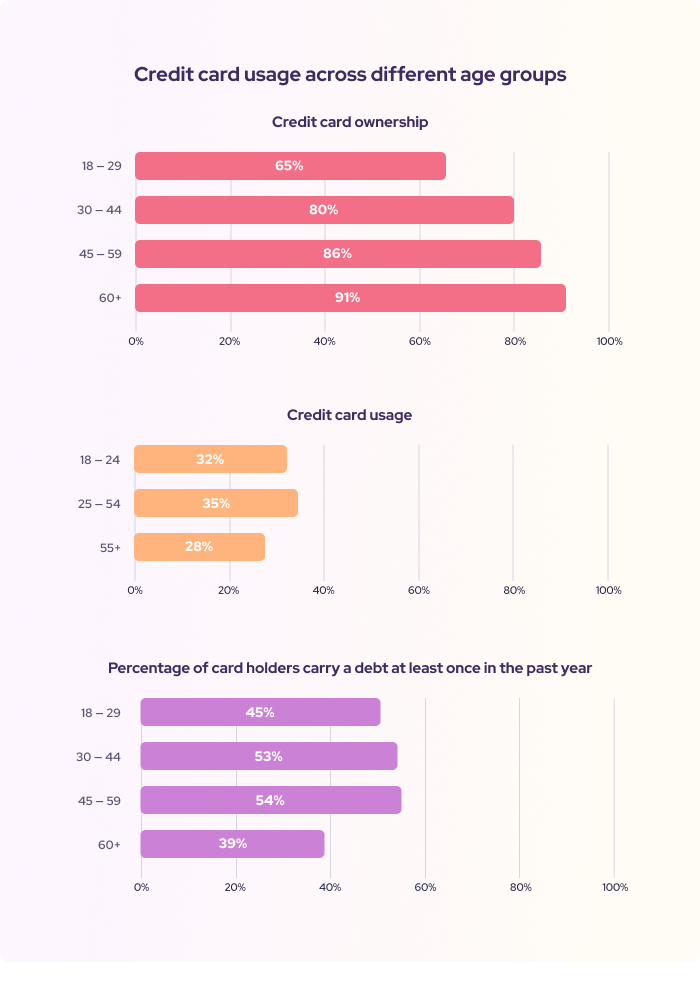

Consumer payment preferences have been evolving quickly, particularly in recent years. While cash still plays a role, the use of credit, debit cards, and contactless payment continues to grow, reflecting changing habits and technology.

A Federal Reserve study in 2024 highlighted that, for the first time, small-value payments (purchases under $25) were dominated by credit and debit cards rather than cash. This marks a shift from cash's traditional role in these transactions.

Demographics also play a part in payment method preference. Younger generations, particularly those under 55, are far more likely to use credit or debit cards, with cash accounting for just 12% of their transaction types. Not far behind in adoption, older consumers (55 and up) use cash for 22% of their purchases. Household income influences these trends too—higher-income households favor credit cards, while lower-income groups rely more on cash, often for budgeting purposes or due to limited access to banking services.

As a business owner, understanding these trends is crucial. With more customers expecting credit card payment options, it’s worth considering whether sticking to a cash only business might mean losing out on sales. In the next section, we'll dive deeper into the pros and cons of accepting credit cards for your business.

The pros and cons of accepting credit cards?

Deciding to process credit cards is a big step for owners that operate cash only businesses. It opens the door to new opportunities and customers but also brings its own challenges. Let’s break it down.

The pros of accepting credit cards

- More customers, more sales: People love convenience, and many prefer to pay with credit cards. Studies show that cash use continues to decline, especially among younger consumers. Accepting cards means you won’t lose customers who don’t carry only cash.

- Higher spending: Credit card users often spend more per transaction than cash users. With cards, people aren’t limited by what’s in their wallet, which can boost your average sale size.

- Improved business reputation: Offering multiple payment options signals professionalism and modernity. Customers expect businesses to accept cards, and meeting that expectation can enhance your credibility.

- Reduced security risks: Keeping large amounts of cash on hand can make your business a target for theft. Accepting cards means less cash in the register, reducing your risk.

- Easier tracking: Digital payment records make it simpler to track sales, manage inventory, and prepare for taxes. It’s a win for organization and bookkeeping.

The cons of accepting credit cards

- Transaction fees: Credit card processors charge fees for each transaction, which can eat into your profits. These typically range from 1.5% to 3.5% per sale, depending on your provider.

- Equipment and setup costs: Getting started with card payments usually involves upfront costs for equipment like card readers and ongoing monthly fees for processing services.

- Fraud and chargebacks: Credit card fraud is a real risk, especially for businesses that process transactions without strong verification measures. Chargebacks (when customers dispute a charge) can also lead to lost revenue.

- Technology dependence: Card payment systems rely on internet or mobile connections. If those go down, you might not be able to process transactions, creating potential hiccups.

- Learning curve: Adopting a card system means learning how to use new tools, handle disputes, and manage processing fees. For some, this might feel overwhelming at first.

- Slower cash flow: Credit card processors typically take 2–3 business days to deposit the money into your bank account after a transaction. In contrast, cash payments provide instant access to funds, allowing you to cover expenses and reinvest in your business without delay.

Is accepting credit cards worth it?

Accepting credit cards isn’t just about keeping up with the times—it’s about meeting your customers where they are. While there are costs involved, the potential to grow your customer base and increase sales often outweighs the downsides. Not to mention that there is also a cost to accepting cash for businesses which we’ll explore in our next section.

The cost of accepting cash

While cash might seem straightforward, it comes with hidden costs that can add up quickly. Here’s a breakdown of the most significant expenses:

- Bank fees: Depositing cash isn’t always free. Some banks charge fees for large cash deposits, and regular trips to the bank can cost businesses around $25 or more per visit when accounting for time, fuel, and other expenses.

- Theft and security risks: Cash is a prime target for theft, both internally and externally. Business insurance premiums may be higher for cash-heavy operations due to these risks, and security measures like cameras or safes can add hundreds of dollars annually to your costs.

- Labor costs: Handling cash is time-consuming. Employees spend time counting, reconciling, and transporting it, with labor costs adding up to as much as 5-15% of cash transactions due to errors, lost time, and inefficiencies.

- Operational inefficiencies: Running out of change or needing frequent trips to the bank can disrupt operations, leading to downtime and potential missed sales.

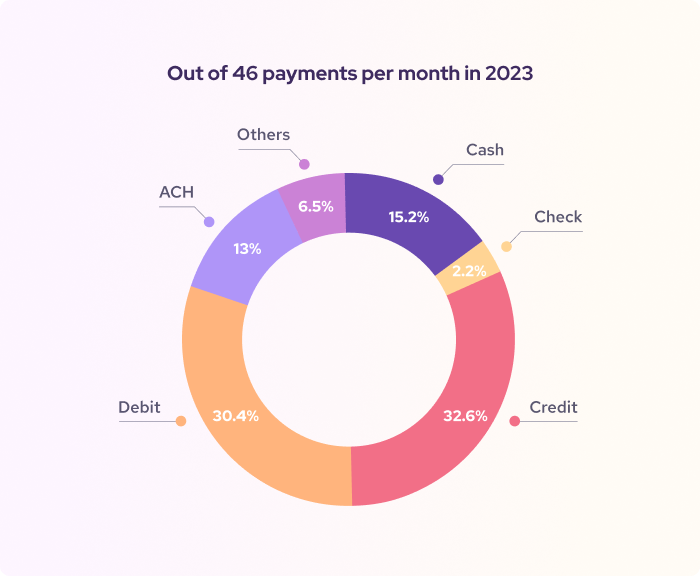

- The loss of sales: As credit cards accounted for 28% of all transactions in 2023, businesses that don’t accept card payments may struggle to serve customers who prefer paying with cards—or those who no longer carry cash at all. As a result, you risk losing sales.

These indirect costs make cash less economical than it first appears. When compared to the relatively low processing fees of 1-3% for credit cards, cash might not be as cheap as you think.

The cost of accepting credit cards: Transaction fees and more.

When deciding to accept credit cards, many business owners worry about costs. But here’s the good news: the expense of credit card processing is often outweighed by the benefits it brings. Plus, working with the right payment processor can keep fees low and manageable.

Here are some common costs to look out for when deciding if the expense to accept credit cards is worth it for your business.

1. Transaction fees

Yes, every card transaction comes with a fee, typically ranging from 1.5% to 3.5% of the total sale. But consider this: these fees buy you access to customers who might otherwise walk away if you were cash-only. A $20 sale with a 2% fee costs just $0.40—a small price to pay for growing your business.

Top processors with the lowest credit card processing fees for Canadian businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.39% (avg) + $0.25 | 1.76% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% + $0.30 to 3.3% + $0.15 | 2.5% |

| Stripe (flat-rate) | 2.90% + $0.30 + 0.5% for manually entered cards + 0.8% for international cards* + 2% if currency conversion is required | 2.7% + $0.05 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Top processors with the lowest credit card processing fees for U.S. businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.49% (avg) + $0.25 | 1.93% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% to 3.30% + $0.30 | 2.60% + $0.15 |

| Stripe (flat-rate) | From 2.90% + $0.30 + 0.5% for manually entered cards + 1.5% for international cards + 1% if currency conversion is required | 2.70% + $0.50 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Some providers, like Helcim, make fees transparent and affordable. Helcim offers interchange-plus pricing, which means you only pay the card networks' base cost plus a small markup. This model ensures you never overpay, unlike flat-rate providers that charge the same fee for every transaction and likely pocket extra margins.

2. Monthly or annual fees

Some payment processors charge businesses ongoing fees to maintain their merchant accounts. These can range from $10 to $50 per month for access to their platform, customer support, and other services. Some providers also tack on annual fees for premium features.

Be sure to look into these additional costs on top of transaction fees before signing up to accept credit card payments.

Hint: Helcim has no monthly, or annual fees.

3. Equipment costs

To accept credit cards, you’ll need equipment like a card reader or point-of-sale (POS) system. POS equipment costs can vary depending on your needs, but checking out cloud based POS systems that require minimal equipment or providers that offer tap to pay on iPhone can be a great way for your business to start accepting credit cards for little to no hardware cost.

4. Chargebacks and fraud

Chargebacks occur when customers dispute a charge they see on their credit card. If the dispute isn’t resolved in your favor, you not only lose the sale but may also face a chargeback fee—typically $15 to $25 per dispute depending on your processor.

Credit card fraud is another risk, with potential financial losses if fraud protection measures aren’t in place so be sure to set up a merchant account with a credible payments company so you can reduce the risk of fraud.

What do cash-only businesses need to get started and accept credit cards?

If you’ve made it this far, it means your cash only business is seriously considering accepting credit cards. Let’s break down the steps you need to take to make it happen.

1. Choose a payment processor

The first step is to partner with a reliable payment processor. Look for one with transparent pricing, excellent support, and tools tailored to your business size and industry.

2. Set up a merchant account

A merchant account is where credit card payments are temporarily held before being deposited into your bank account. Many processors now bundle this service, so you don’t need to apply for one separately but will rather be assigned one once your sign up process is complete and your business is approved by a processor’s acquiring bank or risk teams.

3. Select the right equipment

If you want to accept credit cards in person, you’ll need to consider what type of credit card terminal your business will need. There are many variations of POS systems that can help streamline credit card transactions. What your business needs will be dependent on whether you are an online business, brick and mortar shop or both. Online businesses will likely look to more ecommerce tools and embedded payment pages and wont need hardware per se, but if you have a physical location and expect to accept credit cards in person a cloud based POS or Tap to Pay on iPhone provider can be a low cost way to start out.

4. Ensure secure internet connection

Card payments require a stable internet connection. If your business operates in an area with spotty service, consider a mobile credit card reader or offline-capable POS system.

5. Train your staff

Once your system is in place, train employees on how to process payments, handle disputes, and use fraud prevention tools. A little preparation goes a long way in ensuring smooth transactions.

6. Update your business policies

Let customers know you now accept credit cards by displaying signs, updating your website, or promoting the change on social media. You may also want to review your pricing or return policies, as customers paying by card might have different expectations.

Best credit card processor for cash-only businesses

Deciding to accept credit cards is a big step. If you're ready to take the leap into accepting credit cards, Helcim is the ideal partner for cash only businesses. With transparent pricing, free POS software, and low-cost hardware, Helcim makes it affordable and easy to get started. Their exceptional customer support and fraud protection give you peace of mind, while their scalable solutions grow with your business. Making the switch has never been simpler—or smarter. Sign up for free today.

FAQ.

Is it expensive to accept credit card fees?

Accepting credit card fees isn’t as expensive as it might seem. Most fees range from 1.5% to 3.5% per transaction, depending on the card type and processor. While that might sound like a lot, the cost often offsets itself through increased sales and customer convenience.

Do businesses pay to accept credit cards?

Yes, businesses pay fees to accept credit cards. These typically include transaction fees (a percentage of each sale), monthly fees, and sometimes equipment costs. However, some processors eliminate hidden fees and offer free tools like POS software, making it more affordable for small businesses to start accepting cards.

Does accepting credit cards increase sales?

Yes, accepting credit cards can significantly increase sales because you can now accept payments from someone who is less likely to carry cash. Studies show that customers tend to spend more when paying with a card versus cash. Credit cards also open your business to more customers who prefer cashless payments. For example, the Federal Reserve reported that credit cards accounted for 28% of all transactions in 2023, showing how widespread their use is among consumers.

How can businesses avoid credit card fees?

While you can’t eliminate credit card fees entirely, there are ways to reduce them:

- Choose a transparent payment processor like Helcim, which offers fair, interchange-plus pricing.

- Encourage ACH transactions, as ACH fees are often lower than credit card fees.

- Set minimum purchase amounts for credit card payments, if allowed.

- Shop around for the best rates and negotiate with processors.

- Pass on fees to your customer using surcharging tools like Helcim Fee Saver