For small and medium-sized businesses, credit card payment processing fees can take a significant bite out of your profits. The good news? There are ways to minimize those costs and optimize how you accept payments. With a little strategy and the right payment provider, you can reduce the fees you’re paying and put more money back into your business. Here are four powerful tactics you can start using today.

Tactic 1: Understand your credit card processing fees and optimize how you process payments

To reduce your credit card processing fee, you first need to understand what you’re paying for. Each transaction carries multiple layers of fees, like assessment fees, interchange fees, and more which can vary based on several factors. Let’s break them down:

The pricing structure of your payment processor

Not all processors charge the same way. Different pricing models, such as flat rate and subscription models, impact the overall cost structure, with some eliminating monthly fees while others require them, which can significantly affect a business's expenses depending on their sales volume.

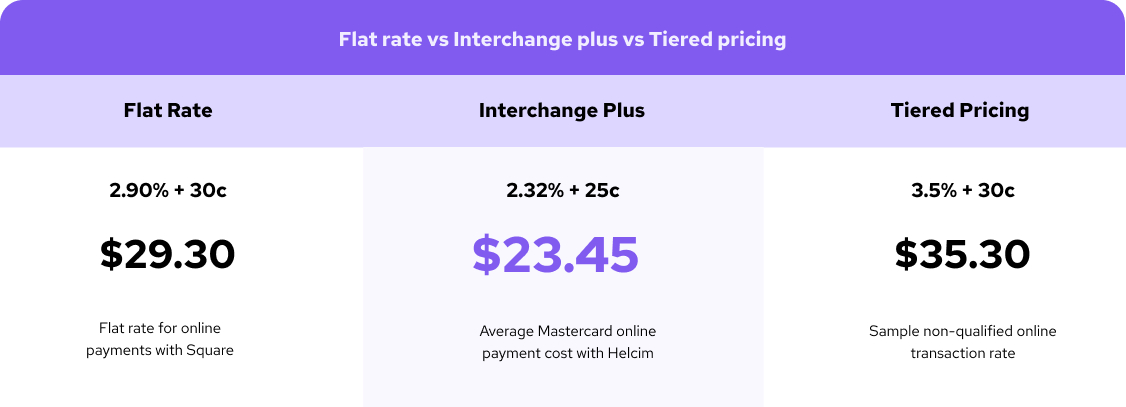

Some use flat-rate pricing, which offers simplicity but may not always be the cheapest option for every business.

Others offer tiered pricing, where fees vary based qualified and non-qualified transactions which can lead to higher costs if you’re not careful.

The most transparent (and often the most cost-effective) is interchange-plus pricing, where you pay the true cost of each transaction plus a small markup. Credit card networks like Visa and Mastercard charge varying rates and fees. Interchange fees are determined by various factors such as transaction amounts and card types. Understanding which pricing structure your payment processor uses—and which works best for your business—can significantly affect your costs.

The types of cards you accept

High-reward credit cards are great for your customers—they earn points, cashback, and perks. But for businesses, these cards come with higher processing fees because banks charge more for the perks. If a significant portion of your customer base uses these types of cards, it’s important to factor in those higher fees.

On the flip side, accepting debit cards or basic credit cards often leads to lower processing fees. Accepting both credit and debit cards is essential for enhancing sales opportunities while managing costs.

The way you accept payments

Whether it’s in-person or online—plays a big role in how much you pay in processing fees. Each method comes with different costs, and understanding these can help you make better decisions to reduce fees.

In-person transactions (swipe, insert, or tap) usually come with lower fees because they are considered less risky. When the cardholder and the card are physically present, there’s a lower chance of fraud, which means banks charge you less. Card-not-present transactions (like online payments, phone orders, or recurring payments) typically carry higher fees due to the increased risk of fraud. If your business operates mostly online, it’s important to evaluate how much these transactions are costing you and consider processors that offer competitive rates for online payments. ACH payments: If you’re looking to drive processing costs down even further, ACH bank transfers (Automated Clearing House) are an excellent option. ACH transactions generally charge much lower fees than credit cards—for instance, Helcim's ACH payments are only 0.5% + $0.25 per transaction. This can make a significant difference, especially for businesses that process high-dollar transactions or recurring payments.

Optimizing your payment process starts with choosing the right payment methods and processor. Whenever possible, accepting in-person payments that leverage an interchange plus pricing model or explore ACH payments to reduce costs.

Tactic 2: Leverage Level 2 and Level 3 data to cut costs

For businesses that regularly deal with B2B (business-to-business) or B2G (business-to-government) transactions, leveraging Level 2 and Level 3 data is one of the most effective ways to reduce processing fees.

But what is it? Simply put, Level 2 and Level 3 data refers to extra information businesses can provide to their payment processors during a transaction that can help lower credit card processing fees. This additional data makes the transaction more secure in the eyes of banks, which means they charge you less.

Level 2 processing

This applies primarily to B2B payment processing and allows for lower interchange rates when you provide additional data, such as sales tax, invoice numbers, or customer codes. This additional information gives the card networks and banks more security, which reduces the risk of fraud and leads to lower fees for your business.

Level 3 processing

This is even more detailed and is often used in B2B and government transactions. By providing data like line-item details of purchases, shipping information, and item quantities, businesses can qualify for the lowest interchange rates available. Level 3 processing requires more information, but the savings can be significant—especially for companies dealing with large or recurring corporate transactions.

Not every business needs Level 2 or 3 processing, but if you’re handling large or frequent B2B transactions, the savings can quickly add up. Some payment processors, like Helcim, make it easy to automatically apply Level 2 and 3 data, helping you get the reduced rates if the data is qualified.

If your transaction data is qualified, you can see the immediate savings for Mastercard transactions. However, for Visa transactions, savings may not appear right away because of stricter rules under Visa’s Commercial Enhanced Data Program (CEDP). We need to ensure that all extra data is as high-quality as possible. Therefore, you can see the savings as a retroactive adjustment up to 45 days after the original transactions if your data is qualified. This means savings would be credited to you on the following month's statement.

Tactic 3: Maximize volume discounts

The more transactions you process, the more you should be able to save. Many payment processors offer volume discounts for businesses that handle large amounts of credit card transactions. Here’s where it gets interesting: some payment processors (again, like Helcim) provide automatic volume discounts—no forms, no negotiations, just automatic savings as your business grows. This means if you’re scaling up and processing more transactions, you don’t have to worry about manually requesting a discount. It’s already built into the system. If you’re processing high volumes of transactions but aren’t seeing those discounts automatically applied, it’s time to start looking for a processor that rewards your business’s growth without extra paperwork.

Tactic 4: Pass on processing fees with surcharging and convenience fees

One of the most straightforward ways to reduce the impact of credit card payments processing fees on your business is to pass them on to your customers. While this may not be suitable for every business or customer base, it’s an increasingly popular strategy and one that is worth considering. Here are a few ways to pass on those fees:

Surcharging

This is the most direct way to cover your processing fees. A surcharge is a small fee added to credit or debit card transactions that helps offset the cost of processing. It’s important to check local regulations, as not all states or countries allow surcharging, but where permitted, it’s a great way to pass those costs to customers who choose to pay with a credit card.

Convenience fees

These are slightly different from surcharges in that they apply when a customer uses a non-standard payment method. For example, if your business typically accepts in-person payments but offers an online option, you could charge a convenience fee for using that online method.

Helcim's Fee Saver offers a built-in way for businesses to implement surcharging or convenience fees making it easier to pass on processing costs without disrupting your customer experience. Done right, passing on fees can be a smart way to reduce the impact on your profits.

Final thoughts: Start saving on your processing fees

Reducing your credit card processing fees doesn’t have to be a complicated process. By understanding what drives your costs, leveraging tools like Level 2 and 3 data, maximizing discounts, and exploring options to pass fees on to customers, you can take control of your fees and start saving. The key is to stay proactive and choose the right strategies that work best for your business. And, of course, it doesn’t hurt to work with a payment processor that makes saving easy by offering transparent pricing, automatic discounts, and flexible fee-passing options.

Ready to start saving on your credit card processing fees?

Sign up with Helcim today and see how much you can save! With transparent pricing, lower rates for in-person and online transactions, and support for cost-saving options like ACH payments, Helcim makes it easy to keep more of your hard-earned money.

FAQs

1. What’s the difference between in-person and online transaction fees?

In-person transactions generally come with lower fees because they’re less risky—both the cardholder and the card are physically present, reducing the chances of fraud. Online (card-not-present) transactions carry higher fees because the risk of fraud is higher.

2. How does Level 2 and Level 3 data reduce processing fees?

By providing extra information to your payment provider (like sales tax or line-item details) during transactions, you make the transaction more secure for banks, which lowers your fees. Level 2 is typically for B2B payments, while Level 3 applies to larger B2B or government transactions.

3. What are ACH payments, and how do they save me money?

ACH payments are a way to transfer funds directly between bank accounts. They charge much lower fees (around 0.5% + $0.25 per transaction) compared to credit card processing, which ranges from 1.4% to 4%. This makes ACH a great option for businesses processing high-dollar transactions or recurring payments.

4. What are surcharges and convenience fees, and can I apply them?

Surcharges are additional fees added to credit card transactions to help offset processing costs. They’re typically used when customers choose to pay with a credit card. Convenience fees, on the other hand, are charged when customers use a non-standard payment method, like paying online when the business primarily accepts in-person payments. Helcim allows you to easily set up surcharging and convenience fees, helping you pass on some of the processing costs to your customers.