Do you got this, or shall I?

Imagine asking your customers this next time they pull out their credit card for a $2.00 transaction. But in all seriousness, business owners are starting to wonder if maybe it’s time to let their customers foot the bill on payment processing costs- they are getting the benefits of high-rewards consumer card and cash-back options after all, right?

Many businesses are still hesitant to impose credit card processing fees, holding onto a notion of customer service by claiming that it is merely a necessary cost of conducting business.

As a business owner, all this controversy may make you wonder:

What goes into payment processing fees anyway?

- Who is benefitting?

- Why are processing fees so expensive?

- Why do some payment providers charge more than others?

- Why do some providers offer various pricing models depending on where you go?

- What’s the actual cost of payment processing?

- And finally, who should pay the tab when it comes to accepting payments?

In this article, we will answer all these questions. We will explain what processing fees are, what they entail, what factors go into their cost, who pays them, and how you can optimize your payment processing to pay lower fees on your transactions. Finally, we will tell you how you can take advantage of free credit card processing by passing these fees on to your customers.

Understanding Credit Card Processing Fees

If you’re new to payment processing, you’re probably wondering what all this fuss about credit card processing fees is.

Here are the basics: Processing fees are a cost businesses incur for accepting card payments. While processing fees may appear as a burden, they play an integral role in the stability and growth of the credit card payment system. They contribute to the development and maintenance of robust networks, advanced fraud prevention measures, and ongoing technological innovations that make electronic payments a secure and convenient option for businesses and customers alike.

The merchant pays these fees to a payment processor who divides up respective payments to the card brand networks and banks and puts a little aside to cover their own costs.

The portion that is paid to the card brand networks and banks is called the interchange fee. Every payment provider has to pay these interchange fees, almost like paying the tax at a toll bridge, in order to use the card brand networks and do business with key players. They are a necessary contribution towards maintaining the infrastructure that supports the reliability and security of card payments.

Behind the Scenes: Getting to know the main characters

You can think of payment providers as guardians overseeing the integrity of transactions and ensuring a secure and efficient payment system. The guardian is working diligently behind the scenes to guide you through your payments journey and collaborates with a diverse cast of characters within the credit card payment industry. Then, you have the card networks, such as Visa and Mastercard, which facilitate the smooth flow of electronic transactions.

Accompanying them are the acquiring banks and issuing banks, working diligently behind the scenes to facilitate the movement of funds between your customers’ cards and your business account. Your payment processor facilitates this journey, ensuring seamless transactions and protecting your data from fraud and security breaches.

Of course, there are other factors which might influence your processing fees , such as the risk factor of the transaction. For example, in-person transactions are far less likely to be fraudulent than online purchases. Furthermore, certain merchants might be deemed higher risk, or the type of card or transaction they are accepting may cost all the players a little more skin than other types of transactions. And finally, you may come to learn that, unfortunately, not all payment providers are transparent guardians and try to take more margin and fees then they need.

Have you ever felt like there’s a sneaky creature lurking in the shadows, ready to snatch away a chunk of your hard-earned money every time you make a credit card transaction?

Enter the fee goblins.

These payment processors take more than their share to cover their costs and revel in the fog of interchange fees, feeding on the confusion and overcharging you on your rates and smuggling extra charges on your merchant statement.

For all these reasons, it is all the more important to know how to choose your payment processor wisely, which will help to make your rates as affordable as possible.

Who Pays Credit Card Processing Fees?##

The short answer is that merchants are responsible for covering credit card processing fees.

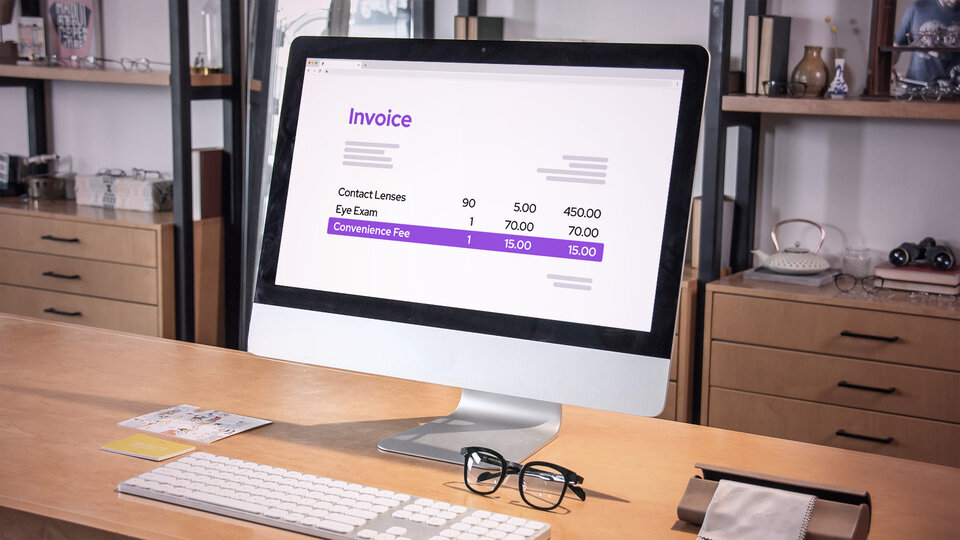

However, this does not mean that they can’t pass on the cost to their customers. And depending on the pricing model you use with your payment processor, you may not even see the actual processing fees on your statement. For example, if your provider charges you a subscription fee, you may be charged by the amount of transactions or by pricing tier. While you could infer that this fee covers the processing costs of your transactions, you might not know if you are overpaying for what you are using.

With Interchange Plus pricing, however, Helcim passes on the true cost (the interchange fee we discussed earlier) to you with a small, single markup, so you pocket the savings instead of overpaying on transaction fees.

Optimizing Your Credit Card Processing Strategy

Stop overpaying on fees and processing costs

As the Fee Goblin’s grip tightens, merchants wonder if there’s a way to reduce their processing costs. Whether you’re overpaying with your current provider or looking for ways to pass on your fees, one of the most important aspects to consider is your provider and pricing strategy.

You’ll want to understand the pricing models payment processors utilize, including flat rate pricing, Interchange Plus pricing, and tiered pricing, and determine which aligns best with your business needs. Not only can you save money on your transactions, but you may also notice a boost in customer service and other perks, such as access to free software tools. Plus, you can nix some extra or hidden fees, such as monthly equipment and administrative fees. Be aware of common additional costs that payment processors may charge, such as account change fees, early termination fees, and PCI non-compliance fees, and learn how to trim extra fees from your payment processing.

Finally, with subscription pricing, for example, passing on processing fees becomes more complicated. You’re still paying for these costs in your payment provider service, but it becomes harder to pinpoint the costs of each and how to pass them on to your customers.

The Surcharging Dilemma

Even for those using Interchange Plus pricing, paying processing fees can still bite. While we have covered some ways to lower your processing costs and shrug that fee goblin off your back, let’s discuss another solution: shifting the processing costs to the customers themselves. Enter the controversial technique of surcharging.

Some merchants already use this method, effectively passing on their credit card processing fees directly to their customers just by adding a small percentage or flat fee to each transaction. But is it a fair solution, or does it risk driving customers away? And this brings us back to our age-old question: Who should pay processing fees?

The answer? It’s up to businesses to make the right call for their customers and interests. However, there are some strategic considerations and best practices for passing on your processing fees, such as competitive positioning, customer experience, and industry norms.

Winning the Battle

While the Fee Goblin may seem unbeatable, there are strategies to approach surcharging or lowering your credit card processing fees. With some guiding principles to help you find and switch to a true-blue fee guardian, we hope this guide has helped arm you with tactics to minimize the goblin’s toll on your profits.

Find a provider who works with you to pass on your processing costs

When it comes to passing on processing fees, ask your provider about leveraging software integrations such as the Helcim Fee Saver. A seamless software integration with your payment processor can lend you the ability to streamline operations and communicate these changes to your customers seamlessly. Overall, these subtle touches go a long way to boosting your professionalism and preserving customer goodwill to help you reduce costs and support your small business.