What is a POS transaction?

A POS transaction happens whenever a customer buys products or services from your business. Imagine a customer picking up an item in your store and paying with cash, swiping their credit card, or tapping their smartphone. A POS transaction also occurs online, through invoices, via SMS or email, or through virtual terminals.

No matter how or where these transactions take place, they all get processed and recorded through your POS system.

What are the different types of POS transactions?

POS transactions are most commonly categorized into cash, debit card, credit card, and ACH transactions. Depending on the industry you're in, your customers or clients may trend towards certain payment methods over others.

When it comes to credit card, debit card, and ACH transactions, here's how some common industries tend to accept payments with Helcim:

| Industry | Credit card payments | Debit card payments | ACH payments |

|---|---|---|---|

| Healthcare | 91% | 8% | 1% |

| Retail Goods | 84% | 16% | 0% |

| Professional Services | 89% | 6% | 5% |

| Automotive | 89% | 9% | 1% |

| Health Beauty and Wellness | 80% | 19% | 1% |

| Wholesale | 88% | 11% | 2% |

| Enterprise Utilities | 97% | 2% | 1% |

| Recreation | 67% | 32% | 1% |

| Education | 87% | 9% | 4% |

| Contractors Home Services | 86% | 8% | 7% |

Enterprise Utilities skews heavily towards credit card payments with 97% of their customers using credit cards to pay. The recreation industry has the highest trend towards debit card payments with 32% of their customers choosing it over ACH and credit card. Contractors and Home Services have the highest portion of clients choosing ACH, with 7% of them preferring ACH to debit and credit card.

1. Cash

When the customer is physically at the store to make a payment, they can use cash to pay for their purchase. The customer hands over cash to the cashier, who enters the amount into the cash register. The POS system calculates the total and provides the change if any.

According to the Federal Reserve Bank, the cash usage of consumers with a bank account decreased from 25% to 17% in 2022. This indicates a decline in cash usage compared to other forms of payments, such as credit and debit cards. If your business only take cash payments, it's time to consider accept credit card payments instead of cash-only.

2. Debit card transactions

A debit transaction happens when your customer uses their debit card to pay for something. The POS system sends the transaction details through a card processor to their bank, which checks the card and account balance before approving the payment. Once approved, the money moves from their bank account to your account.

Another type of debit card transaction is a POS withdrawal, where the customer can withdraw cash while making a purchase. For example, if they’re buying $50 worth of groceries, they might ask for a $20 cash withdrawal. The customer will then pay a total of $70 with their debit card, and you hand them $20 in cash along with their groceries and receipt.

3. Credit card transactions

When customers use their credit cards for purchase, the customer's bank pays the merchant. The customer then repays the bank, either in full or through monthly payments with interest.

According to the Board of Governors of the Federal Reserve System, 82% of adults in the US had at least one credit card in 2022. This statistic highlights the widespread popularity of credit card usage for both in-person and online transactions.

Another form of credit card transaction is a hold transaction. For example, if a customer checks into a hotel and uses a credit card to pay a $200 security deposit, the hotel places a hold of $200 on their card to cover any potential charges, like room service or damages. The customer may see a pending transaction of $200 in their bank app, even though they haven't spent that money yet.

When the customer checks out, if there are no additional charges, the hotel releases the $200 hold, and the pending credit transaction disappears. However, if there are charges for room service or damages, the hotel will charge the card accordingly, and any remaining amount from the hold will be released.

4. ACH transactions

ACH bank transfers are electronic bank-to-bank transfers that enable customers to transfer money directly from their bank accounts. The ACH transfer network is managed by NACHA, the National Automated Clearing House Association, a not-for-profit organization that connects around 11,000 financial institutions across the United States.

What are examples of a POS transaction?

In-Person POS transaction example

A customer is shopping at a local clothing boutique.

Step 1: The customer browses the store and picks out a few items they want to buy. They bring their selections to the checkout counter.

Step 2: The cashier scans each item's barcode using a barcode scanner that's connected to the POS system. If an item doesn’t have a barcode, the cashier can manually enter the item code or select it from the register screen.

Step 3: The POS system automatically calculates the total cost of $90, including any sales tax and discounts.

Step 4:

- If the customer pays with cash, they hand over $100 to the cashier. The cashier enters the cash amount into the POS system, which then calculates the change due back to the customer.

- If the customer decides to pay with a credit card, they insert or tap their card on the card reader.

- The customer can also use Apple Pay or Google Pay by tapping their phone. They select the saved debit or credit card in their mobile wallet to complete the payment.

Step 5: After the payment is processed, the receipt printer prints the receipt, and the POS system updates the inventory to reflect the sale of the purchased items.

Online POS transaction example

-

Digital invoicing: Imagine a consultant sending an online invoice to a client via email. The client clicks on the payment link, chooses a credit card, and easily enters their name, card number, expiration date, and CVV on the online form. Just like that, the transaction is complete!

-

Subscription transactions: A customer signs up for a gym membership using ACH payment. During their visit, a sales associate helps them set up the start date and payment intervals, entering the bank details like transit number, bank ID, and account number. On every billing date, the POS system automatically transfers the money from the subscriber’s bank to the merchant’s bank, making the process smooth and effortless.

-

Virtual terminal: A customer calls a motorcycle dealership and shows an interest in buying a new bike. They need to pay a deposit before picking it up. Over the call, they provide their credit card details to the sales associate, who enters the info into the virtual terminal to process the deposit. Once approved, the associate emails the receipt and schedules the pick-up date. Easy and convenient!

-

Online checkout page: A customer adds items to their cart and heads to the checkout page. They enter their shipping info, choose to pay with a credit card, input their payment details, review the order summary, and click "Place Order." The customer gets a confirmation email with the receipt and tracking info.

How much does a POS transaction cost?

Credit card transaction fees

The processing fee for credit card POS transactions is from 1.5% - 3.5%.

Here are the top processors with the lowest processing fees for Canadian businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.39% (avg) + $0.25 | 1.76% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% + $0.30 to 3.3% + $0.15 | 2.5% |

| Stripe (flat-rate) | 2.90% + $0.30 + 0.5% for manually entered cards + 0.8% for international cards + 2% if currency conversion is required | 2.7% + $0.05 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Here are the top processors with the lowest processing fees for U.S. businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.49% (avg) + $0.25 | 1.93% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% to 3.30% + $0.30 | 2.60% + $0.15 |

| Stripe (flat-rate) | From 2.90% + $0.30 + 0.5% for manually entered cards + 1.5% for international cards + 1% if currency conversion is required | 2.70% + $0.50 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

The processing fees are made of two primary components:

- Interchange fees: These are fees paid to the customer's bank for processing transactions. These fees vary based on the card brands, whether the transaction occurs in-person or online, and the pricing model employed by the payment processor.

- Processor margin: This is the fee charged by the payment processor for accepting and handling the transactions.

How to prevent fraudulent POS transactions?

Fraudulent transactions are unauthorized purchases made with stolen credit card information. Since the real cardholders are unaware of these purchases, they will dispute the transactions, which can cause you to lose sales, especially if you've already shipped the product.

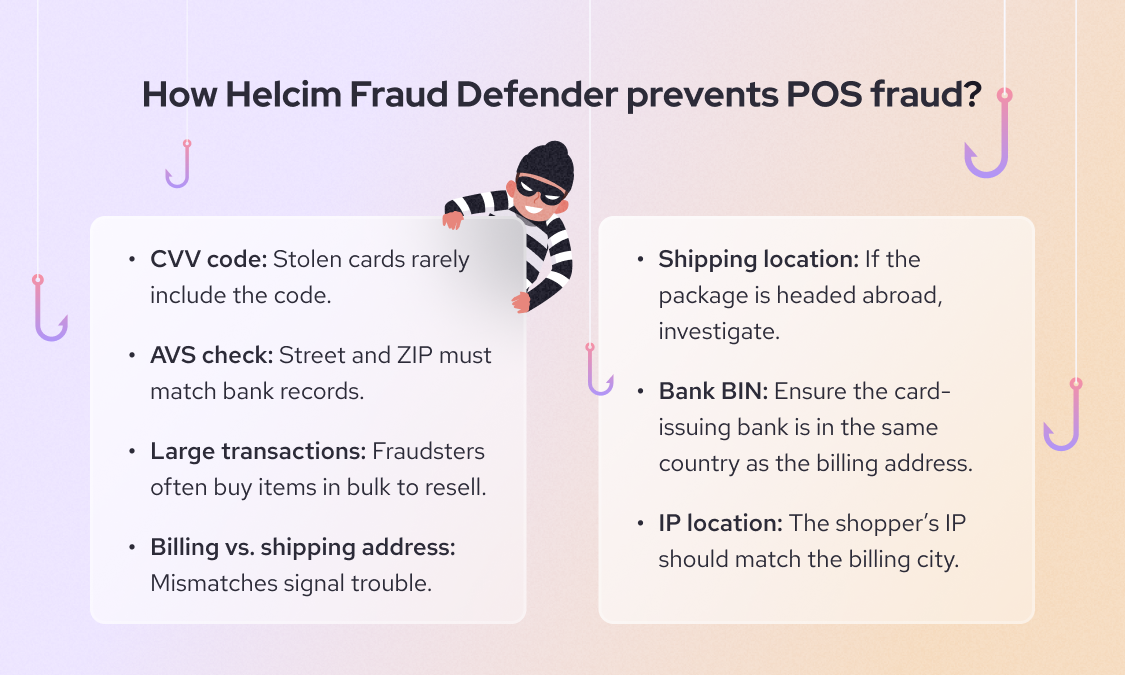

To help prevent fraudulent POS transactions, payment processors offer tools to reduce the risk of fraud. If you’re with Helcim, our Fraud Defender tool evaluates the risk of each transaction based on several key factors:

- CVV Security Code: Fraudsters using stolen card numbers typically won’t have the CVV code. Requiring the CVV helps ensure the card is physically present.

- Address Verification Service (AVS): AVS checks if the provided street address and postal/zip code match what the cardholder's bank has on file.

- Transaction Size: Fraudsters often buy items they can resell, like a large quantity of the same product.

- Billing & Shipping Address: Fraudsters might use the real billing address of the stolen card but a different shipping address.

- Shipping Location: It’s a red flag if the shipping destination is in a different country than the billing address.

- Bank BIN: This verifies if the cardholder's bank is in the same country as the billing address.

- IP Address Location: It confirms whether the customer's IP address matches the billing address's city, state, and country.

Helcim’s Fraud Defender gives each transaction a risk score, helping you decide whether to proceed with shipping the product. If a transaction has a high-risk score, you might choose to refund the payment and avoid shipping the product, reducing the chance of chargebacks and merchandise loss.

If you’ve already shipped your products but later receive a chargeback, you can gather supporting information and dispute the chargeback to recover the lost revenue and associated fees.

Process POS transactions securely with Helcim

Helcim offers a flexible solution for accepting both in-person and online transactions without any monthly fees, contracts, or hidden costs.

Helcim provides free Point-of-sale software and apps that you can easily download to your laptop, tablet, or phone. Just connect a card reader to your device and start processing payments immediately.

For businesses that are always on the move or at job sites, like food trucks, plumbers, or contractors, the Helcim Smart Terminal is an ideal solution. It comes with a built-in POS app, card reader, and receipt printer, allowing you to collect payments and run your business anywhere. Additionally, with Tap to Pay enabled on the Helcim Point-of-Sale app, you can accept contactless payments using just your iPhone.

With just one Helcim account, you get access to a suite of free tools for online payments:

- Online invoicing software

- Online POS (Virtual Terminal)

- Online Store Builder

- Recurring Payments

- Hosted Payment Pages

These tools are great for businesses that operate online and don’t need hardware to collect payments, such as freelancers, accountants, consultants, lawyers, and marketing agencies.

Interested in exploring Helcim? Sign up for free here or contact our sales team for more information.

FAQ

What is POS data?

POS data is the information collected during customer transactions at the point of sale:

- Sales Data: Amount spent, quantity purchased, payment methods used, etc.

- Inventory Data: Stock levels, product details, etc.

- Transaction Data: Date, time, transaction status, and payment methods, etc.

- Customer Data: Name, email, address, saved credit card information, etc.

By leveraging POS data, you can gain valuable insights to enhance customer experiences, and drive sales.

What is a credit POS transaction?

A credit POS transaction refers to the use of a credit card to purchase goods or services. They either swipe their card, insert it into the chip reader, or enter their card details online. The payment provider then verifies if the card is valid and if there’s enough credit available. Once the transaction is approved, a small processing fee is deducted from the total sale amount.

What is a debit POS transaction?

A debit POS transaction is when a customer uses their debit card to purchase goods or services. The payment provider will check if there are sufficient funds available in the customer's bank account. Once the transaction is approved, the amount is directly debited from the customer's account.

What is a POS withdrawal transaction?

POS withdrawal, also known as cash back or cash withdrawal at the point of sale, allows customers to withdraw cash from their bank account while making a purchase using their debit card. This service is commonly available at grocery stores, supermarkets, and other retail locations.

What is a Credit Card Hold transaction?

A credit card hold transaction is when a merchant temporarily reserves a certain amount of money on your credit card to make sure you have enough funds for a purchase. This hold reduces your available credit by that amount but doesn't finalize the transaction yet. The hold usually lasts until the merchant charges your card. If there is no charge, the hold is lifted after a few days, and your available credit returns to normal.