The Department of Finance Canada has made an announcement this May 2023 that is sure to ignite excitement among small business owners across the country.

As part of its commitment outlined in the 2023 Federal Budget, the Government of Canada has successfully negotiated new agreements with industry giants Visa and Mastercard to lower credit card transaction fees, or processing fees, for small businesses. This initiative aims to level the playing field by reducing interchange fees and empowering merchants to maximize their savings potential. And merchants who process with an Interchange Plus pricing model may see substantial savings in processing fees.

The backbone of Canada's economy, small businesses have long grappled with the processing fees associated with credit card transactions. A large portion of these fees, known as interchange fees, is paid to the issuing banks and card brand networks.

What's changing in 2024?

However, the changes may provide respite to an impressive "90 percent of credit card-accepting businesses in Canada qualify for lower rates."

Businesses that process with Interchange Plus pricing are expected to pay 27 % less on average. "These reductions are expected to save eligible Canadian small businesses about $1 billion over five years," states the Department of Finance Canada.

To ensure a fair and balanced approach to credit card processing, Visa and Mastercard have agreed to implement fundamental changes to contribute to these savings. This includes reducing domestic consumer credit interchange fees for in-store transactions to an annual weighted average interchange rate of 0.95 percent.

Additionally, interchange fees for online transactions will witness a decrease of up to 7 percent, thanks to a ten basis point reduction. As a valuable bonus, small businesses meeting the criteria will receive complimentary access to essential online fraud prevention and cybersecurity resources, safeguarding their growth potential.

Visa, Mastercard, and Nonprofit interchange rate eligibility

Credit card networks are implementing separate qualification criteria for lower interchange fees. Under the new regulations, businesses with annual Visa sales volume below $300,000 and those with annual Mastercard sales volume below $175,000 will be eligible for reduced rates from their respective networks. Additionally, nonprofit organizations with transaction volumes falling below these thresholds will also enjoy the advantages of reduced rates.

Impact on small businesses and nonprofits

This move aims to alleviate financial burdens on small businesses and nonprofits, allowing them to retain more of their revenue and invest it back into their operations. By lowering the interchange fees, credit card networks are supporting these vital sectors of the economy.

For small businesses, the reduced interchange fees can lead to substantial cost savings, contributing to their overall profitability. This financial relief can be particularly significant for smaller enterprises, which often operate on narrower margins. During times of economic uncertainty, while many businesses are navigating a recession, this may be a welcomed opportunity for small businesses to redirect the saved funds towards expansion, improving their products or services, or even enhancing their employees' benefits.

Nonprofit organizations, too, stand to benefit greatly from the reduced interchange fees. As these organizations often rely heavily on donations and contributions, any reduction in costs can significantly impact their ability to pursue their missions and provide essential services to their communities. With lower rates, nonprofits can allocate more resources to programs, outreach initiatives, and addressing the needs of those they serve.

In addition to empowering small businesses with lower fees, the government has secured the protection of Canadians' valuable reward points through its agreements with Visa and Mastercard, in collaboration with major banks across the country, preserving the benefits of using and accepting credit card payments for both consumers and businesses respectively. It further anticipates that other credit card companies will take similar steps to lower fees for small businesses, with payment processors passing on the resulting reductions to small-scale enterprises.

How to make the most of the 2024 Interchange Rates

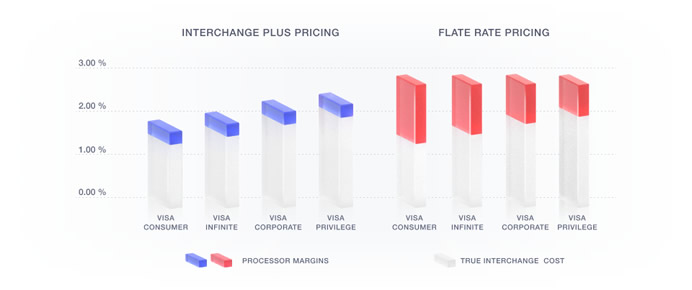

Interchange vs. Flat Rate savings

For businesses looking to capitalize on these savings opportunities, they should be looking to their payment processor and pricing model to determine whether they might see a change in their statement. For example, when considering Interchange Plus pricing vs. flat rate pricing, many flat rate payment processors will not change their fees, despite having lower interchange rates. Other payment processors, such as Helcim, will continue to pass on the wholesale rate of the transaction, including savings, with a small flat margin on top.

As the fall of 2024 approaches, anticipation builds among small business owners who eagerly await the implementation of these transformative changes. With lower credit card transaction fees on the horizon, the stage is set for merchants to capitalize on the savings, embrace growth opportunities, and solidify their positions as pillars of the Canadian business landscape.